What is Zero-Cost Collar Strategy

Written by Upstox Desk

Published on July 31, 2025 | 4 min read

A zero-cost collar strategy, as the name indicates, is a cost effective and risk defined strategy which is deployed to protect portfolio or underlying security against potential down move. A hedge essentially carries a cost. This options strategy is aimed at minimizing the impact of hedging cost while providing protection in case the prices decline over a long term.

The zero-cost collar is usually deployed using LEAPS options, which have a tenure for expiration of more than 12 months. In India only Nifty 50 Index have option contracts that carry option expiry up to 12 months. The stocks are limited to having monthly expiries upto three months.

The zero-cost collar is used by traders or investors when they are mildly bullish towards market sentiments but want to add protection to the long underlying security without incurring hedging cost. Theoretically, the zero-cost collar is a combination of protective put and covered call. The strategy is deployed by selling Out-of-the-Money (OTM) call option to earn premium and buying an At-the-Money put option. Usually, the spread is deployed with a long position in the underlying which provides protection against potentially unlimited loss emanating out of the short call position.

Illustration:

Since on NSE, the long dated expiry is only available on Nifty50 and even those are illiquid, the strategy can be reconfigured to deploy on near and far dated option series. The spread is created by buying an At-the-money Put option and shorting an Out-of-the-money Call option at higher strike.

Strategy | Index | Action | Strike | Price (₹) |

Zero Cost Collar | Nifty50 | Buy Future (Oct 22) | - | 17,100 |

| Buy Put (Oct 22) | 17,100 (strike 1) | -200 | ||

Sell Call (Oct 22) | 17,250 (strike 2) | 200 | ||

Net Premium | 0 |

The trade results in nullification of premium as outflow matches the inflow. Therefore, the strategy is called zero-cost collar. Practically speaking, there will always be a difference in the two premiums as At-the-Money option premium shall always be more expensive than the Out-of-the-Money options.

The breakeven point = strike 1 – net premium = 17,100 – 0 = 17,100

Max potential profit = (Strike 1 – price of underlying – net premium) * lot size

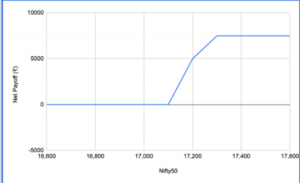

Payoff Chart

Scenario 1 – Nifty expires at 16,900

The short call option is able to preserve the premium earned and the long-put position that was added to provide cover also generates profit as the intrinsic value grows. The fall in the price of underlying may provide gains on the collar but there would be an actual cash erosion in the value of the underlying asset. Therefore, the profits earned would be used to subsidize the losses emanating out of the reduction in value of the underlying asset. Therefore, at this level there is no profit or loss.

Scenario 2 – Nifty expires at 17,300

The long-put option position expires worthless and the short call option position would eventually face the risk of being exercised. The losses are however balanced against the rise in value of the underlying asset or portfolio in the cash segment. The strategy makes a capped profit of ₹7,500.

Conclusion:

- Zero-cost collars can be deployed by novice and retail traders. The execution of strategy is easy but the position needs to be constantly monitored with a well laid out risk management plan.

- The long-dated length of time for option expiry provides more breathing space for holders of the zero-cost collar options. The holder need not square off the positions immediately as the price begins to fall, if the holder is of opinion that the fall in prices is temporary and limited to near term – and the price of underlying security shall recover and rise slightly after the fall.

- The above situation offers a relative amount of comfort and some respite to novice traders and investors from being anxious and stressed from short term moves.

About Author

Upstox Desk

Upstox Desk

Team of expert writers dedicated to providing insightful and comprehensive coverage on stock markets, economic trends, commodities, business developments, and personal finance. With a passion for delivering valuable information, the team strives to keep readers informed about the latest trends and developments in the financial world.

Read more from Upstox

Upstox is a leading Indian financial services company that offers online trading and investment services in stocks, commodities, currencies, mutual funds, and more. Founded in 2009 and headquartered in Mumbai, Upstox is backed by prominent investors including Ratan Tata, Tiger Global, and Kalaari Capital. It operates under RKSV Securities and is registered with SEBI, NSE, BSE, and other regulatory bodies, ensuring secure and compliant trading experiences.

Related articles

Futures and Options

What is the Expiration Time in Options Trading?4 min read | Written by Mariyam Sara

Futures and Options

How to Trade in Options with Small Capital: Strategies for Success6 min read | Written by Upstox Desk

Futures and Options

Top 5 Futures Trading Strategies You Should Know in 20262 min read | Written by Mariyam Sara

Futures and Options

Best Ways To Calculate Commodity Price Risks: Understanding The Main Risks Involved5 min read | Written by Upstox Desk