How to Use LEAPS for Covered Call writing

Written by Upstox Desk

Published on September 21, 2022 | 5 min read

What are LEAPS?

LEAPS are Long-Term Equity Anticipation Securities. These are publicly traded options contracts with the duration to expiry of more than 1 year and upto 3 years.

What is a covered call writing strategy?

A covered call write refers to selling a call option of a security that the writer already has a long position on, in the cash market or in futures.

LEAPS in a covered call write

When LEAPS are used in a covered call writing strategy the premium received is higher than that in the weekly or monthly options as the time to expiry is more. Covered call writing in India cannot be done using LEAPS, as LEAPS options are traded on Indian exchanges. However, the covered call strategy can still be used in the market to hedge your positions.

“Buy write” vs “Covered call”

Covered call strategy can be executed in two ways; “buy write” and “overwrite”. The term “buy write” describes the action of buying stock (or futures) and selling calls at the same time while “overwrite” means selling call options against stock (or futures) already purchased.

Covered call writing example

Let us understand the covered call strategy with the help of an example.

Mr. Ishan purchased stock XYZ when it was trading at ₹45. It is now trading considerably higher at ₹75. His analysis suggests that the stock has strong potential upside in the long term, however, in the short-term, say this month, the stock might see selling pressure. He has 2 options:

- Option 1: Sell the shares in the cash market outright and earn the profit. And buy the shares when the prices dip.

- Option 2: Deploy a covered call writing strategy.

In a covered call strategy, Mr. Ishan will hold the shares and sell a call option to earn the premium.

Here we assume that Mr. Ishan has 100 shares of XYZ and the lot size of the XYZ options contract is also 100. It is important to have the same number of shares as the options contract lot size of the stock to get an adequate hedge.

Mr. Ishan picks an out-of-the-money (OTM) strike price.

Mr. Ishan sells a call option of stock XYZ with the strike price of 80 at a premium of ₹3. Here the total premium received = lot size x premium = 100 x ₹3 = ₹300.

There are three possible scenarios for this strategy:

Scenario 1: At expiry, Stock XYZ is trading at ₹87.

In this case, Mr. Ishan incurred a loss on his call option position as the spot price moved ₹7 higher than the strike price.

Loss in option = (Spot price - Strike price - Premium paid) * Lot size

= (87 - 80 - ₹3)* 100

= ₹400

Mr. Ishan incurred a loss of ₹400 on his call option. However, he earns a notional profit on his holdings as he hasn't liquidated his position yet. The loss on his call option position can be set off against this profit on the underlying XYZ stock.

Scenario 2: At expiry, Stock XYZ is trading at ₹83.

₹83 mark is the break-even point in this scenario, which is calculated by adding the strike price and premium. This point is the same for the seller and buyer of the call option contract.

Break even point = Strike price + Premium = 80 + ₹3= ₹83

So, Mr. Ishan’s profit is zero on his call option. However, he earns a notional profit on his holdings as he hasn't liquidated his position yet.

Scenario 3: At expiry, Stock XYZ is trading at ₹75

In this case, Mr. Ishan's view turned out to be correct and the spot price moved ₹5 lower than the strike price.

Profit = total premium received = lot size x premium = 100 x ₹3 = ₹300.

Mr. Ishan incurred a profit of ₹300 on his call option. However, he earns a notional loss on his holdings as he hasn't liquidated his position yet. This profit earned by selling call option partly offsets the notional loss in holdings. This effectively reduces the cost of buying for the equity holdings.

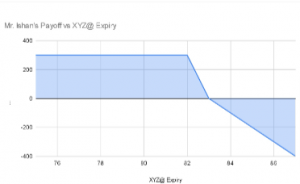

Payoff:

Mr. Ishan's payoff on the call option:

Payoff Schedule for call option writing

| XYZ@ Expiry | (Seller) Mr. Ishan's Payoff |

75 | 300 |

| 76 | 300 |

| 77 | 300 |

78 | 300 |

| 79 | 300 |

80 | 300 |

| 81 | 200 |

82 | 100 |

| 83 | 0 |

84 | -100 |

| 85 | -200 |

86 | -300 |

| 87 | -400 |

Payoff Chart

As Mr. Ishan still continues to hold the shares, he earns a notional profit or loss as the price fluctuates. But the covered call strategy helps him ride this volatility and benefit from a fall or stagnation in the price of the stock.

About Author

Upstox Desk

Upstox Desk

Team of expert writers dedicated to providing insightful and comprehensive coverage on stock markets, economic trends, commodities, business developments, and personal finance. With a passion for delivering valuable information, the team strives to keep readers informed about the latest trends and developments in the financial world.

Read more from Upstox

Upstox is a leading Indian financial services company that offers online trading and investment services in stocks, commodities, currencies, mutual funds, and more. Founded in 2009 and headquartered in Mumbai, Upstox is backed by prominent investors including Ratan Tata, Tiger Global, and Kalaari Capital. It operates under RKSV Securities and is registered with SEBI, NSE, BSE, and other regulatory bodies, ensuring secure and compliant trading experiences.

Related articles

Futures and Options

What are Option Greeks? Delta, Gamma, Theta, Vega, and Rho Explained7 min read | Written by Subhasish Mandal