What is a Protective Put?

Written by Upstox Desk

Published on September 30, 2022 | 6 min read

The protective put strategy is a hedging strategy used to protect an existing long position in the market. In a protective put the holder of a security (equity or futures) buys a put option to protect himself against a drop in price.

When is a protective put used?

A protective put strategy is used when the investor is still bullish on his holdings but according to their analysis it may fall in the near term. It is also used as a means to protect unrealized gains on shares from a previous purchase.

Protective put example

Let's understand this with the help of an example. Mr. Patel already owns 300 shares of Infosys which is currently trading at ₹1,500. He feels that the share price will go higher in the long term, but could fall in the near term. So here he has 2 options:

Option 1: Sell the shares in the cash market and buy the shares when the prices dip.

Option 2: Use a protective put strategy.

Here, Mr. Patel will hold the shares and buy an out-of-the-money (OTM) put option of strike price 1,400 for a premium of ₹50. The lot size of Infosys options contracts is 300.

Therefore, total premium paid = lot size x premium = 300 x ₹50 = ₹15,000.

Note: For the purpose of profit-loss calculations, we will consider ₹1,500 as the purchase price of the underlying Infosys holding as it is the price at which the protective put strategy is deployed.

Therefore,

Infosys purchasing price = ₹1,500.

Premium paid = ₹50

Put strike = ₹1,400.

Cash position break even point= ₹1,500

Long put position break even point= Strike price - Premium paid= ₹1,400 - ₹50= ₹1,350

Protective put strategy break even point = Cash price + premium paid = ₹1500 + ₹50 = ₹1,550.

Scenario 1: Infosys is trading at ₹1,200 at expiry.

In this scenario, Mr. Patel will make a loss on this trade as Infosys spot price is less than the Infosys protective put strategy break even point.

Loss = (Premium paid + Purchasing price - put strike) * lot size= (50 + 1,500 - 1,400)*300 = ₹45,000.

Mr.Patel will incur a loss of ₹45,000 on this trade. His loss on the cash position is ₹90,000. However, the long put position makes a profit of ₹45,000 at this point. Thus, substantially reducing the overall loss incurred due to the fall in the share price.

Scenario 2: Infosys is trading at ₹1,500 at expiry.

Infosys traded sideways in the near term and is at ₹1,500 on expiry. In this scenario, Mr. Patel will make a loss on this trade as ₹1,500 mark is the Infosys cash position break even point but the loss is incurred only on the premium paid for the put option.

Loss = (Purchasing price - Put strike + Premium paid) * lot size= (1,500 - 1,400 + 50) * 300 = ₹15,000.

Mr.Patel will incur a loss of ₹15,000 on this trade, which is equal to the premium paid for buying the put option.

Scenario 3 : Infosys is trading at ₹1,550 at expiry.

In this scenario, Mr. Patel will neither make a profit nor a loss on this trade as ₹1,550 mark is the Infosys protective put strategy break even point.

Protective put formula for Break even point = Infosys purchasing price + premium paid = 1500 + 50 = ₹1,550.

Scenario 4: Infosys is trading at ₹1,800 at expiry.

In this scenario, Mr. Patel will make a profit as Infosys spot price is more than the protective put strategy break even point..

Protective put formula for Profit = [Infosys spot - Infosys purchasing price - premium paid ] x lot size = [1800 - 1500 - 50] x 300 = ₹75,000.

Mr.Patel will incur a profit of ₹75,000 on this trade. His profit on the cash position is ₹90,000. However, the long put position makes a loss of ₹15,000 at this point. Thus, reducing his overall profit.

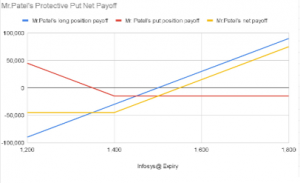

Payoff schedule

Price on Expiry | Cash position payoff | Long put payoff | Net payoff |

| 1,200 | -90,000 | 45,000 | -45,000 |

1,250 | -75,000 | 30,000 | -45,000 |

| 1,300 | -60,000 | 15,000 | -45,000 |

1,350 | -45,000 | 0 | -45,000 |

| 1,400 | -30,000 | -15,000 | -45,000 |

1,450 | -15,000 | -15,000 | -30,000 |

| 1,500 | 0 | -15,000 | -15,000 |

1,550 | 15,000 | -15,000 | 0 |

| 1,600 | 30,000 | -15,000 | 15,000 |

1,650 | 45,000 | -15,000 | 30,000 |

| 1,700 | 60,000 | -15,000 | 45,000 |

1,750 | 75,000 | -15,000 | 60,000 |

| 1,800 | 90,000 | -15,000 | 75,000 |

Payoff Chart

Summary:

- Protective put is a hedging strategy used to protect the investor from the downside in the cash or futures market.

- It is used when the investor is still bullish on his holdings but fears that it may fall in the near term.

- Break even point formula for protective put strategy = purchasing price of the security + premium paid.

- The loss potential is limited when a protective put strategy is deployed. When the price trades below the put option break even point, the losses in the holding will be recovered by the put option.

- Profit potential is high as once the premium paid to buy the put option is recovered, the long position will yield profits as the price goes up.

About Author

Upstox Desk

Upstox Desk

Team of expert writers dedicated to providing insightful and comprehensive coverage on stock markets, economic trends, commodities, business developments, and personal finance. With a passion for delivering valuable information, the team strives to keep readers informed about the latest trends and developments in the financial world.

Read more from Upstox

Upstox is a leading Indian financial services company that offers online trading and investment services in stocks, commodities, currencies, mutual funds, and more. Founded in 2009 and headquartered in Mumbai, Upstox is backed by prominent investors including Ratan Tata, Tiger Global, and Kalaari Capital. It operates under RKSV Securities and is registered with SEBI, NSE, BSE, and other regulatory bodies, ensuring secure and compliant trading experiences.

Related articles

Futures and Options

What are Option Greeks? Delta, Gamma, Theta, Vega, and Rho Explained7 min read | Written by Subhasish Mandal