Market News

Auto sector preview Q2FY25: What to expect across two-wheelers, passenger vehicles and commercial vehicles

.png)

3 min read | Updated on October 15, 2024, 17:41 IST

SUMMARY

The Indian auto sector's Q2FY25 outlook shows strong growth in two-wheelers, challenges in passenger vehicles, a seasonal dip in commercial vehicles, and stability in tractors, driven by rural demand and festivals.

Stock list

Auto sector preview Q2FY25: What to expect across two-wheelers, passenger vehicles and commercial vehicles

The Indian auto sector is gearing up for the Q2FY25 earnings announcement, with varied performances across segments like two-wheelers, passenger vehicles, commercial vehicles, and tractors, driven by multiple factors.

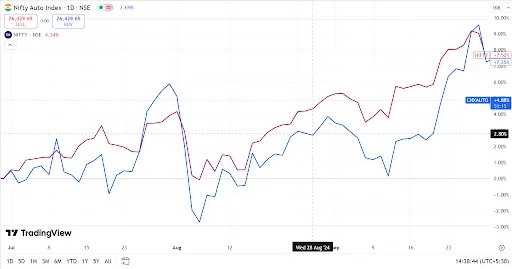

The Nifty Auto index jumped 7.25% in the July to September quarter. However, it underperformed the benchmark Nifty 50 (+7.50%). As of today, October 11, 2024, the return stands at 4.88% (July till date).

(source: tradingview)

Top 10 Automobile companies by market capitalisation

| Name | CMP (Rs) | Mcap (Rs crore) | P/E |

|---|---|---|---|

| Maruti Suzuki | 12,796 | 4,02,300 | 27.37 |

| M & M | 3,126 | 3,88,690 | 35.23 |

| Tata Motors | 931 | 3,42,543 | 10.12 |

| Bajaj Auto | 11,850 | 3,30,920 | 41.4 |

| TVS Motor | 2,790 | 1,32,551 | 77.39 |

| Eicher Motors | 4,717 | 1,29,272 | 30.91 |

| Hero Motocorp | 5,469 | 1,09,377 | 26.95 |

| Ashok Leyland | 228 | 66,833 | 26.74 |

| Escorts Kubota | 3,914 | 43,254 | 41.09 |

(source: screener, 11/10/2024)

2W Segment - Two Wheelers

The two-wheeler segment is set to deliver strong growth in Q2FY25, expected to be around the mid-teens. This growth is driven by increasing rural demand and the build-up to the festive season. A good monsoon will also boost this growth, with the momentum expected to continue due to more weddings in the upcoming months.

Is EV Driving Growth in the Two-Wheeler Segment?

Growth in this segment is driven by a balanced mix of traditional models and the increasing penetration of EVs. Stable commodity prices have helped improve margins slightly.

PVs - Passenger Vehicles

The passenger vehicle segment faced challenges this quarter and might see a marginal dip in volumes. This is due to a high base effect from the previous year and reduced footfalls caused by monsoon conditions.

What is Driving Revenue Stability in PVs?

The utility vehicle (UV) segment has remained steady, with Mahindra & Mahindra and Maruti Suzuki as the primary beneficiaries. However, Tata Motors volumes were impacted by increased competition and slower traction in the EV business.

CVs - Commercial Vehicles

The commercial vehicle segment experienced a seasonal slowdown, with Tata Motors and Ashok Leyland (AL) seeing volume dips ranging from the high single digits to the low teens. Although revenues are expected to be lower, better pricing strategies and stable commodity costs should lead to modest margin improvements.

Tractor Segment

The tractor segment benefitted from a healthy monsoon and a favourable base effect. Mahindra & Mahindra recorded a low single-digit increase in volumes. Consistent rural demand is expected to keep things stable in the near term.

Key Headwinds and Tailwinds to Watch

Tailwinds: The festive season, rural recovery, improvements in product mix, and infrastructure development.

Headwinds: Input costs, discounts to stimulate demand and policy changes, high inventory levels at dealers end.

Review of Q1FY25

In Q1FY25, the two-wheeler segment experienced strong growth due to rural recovery and increased sales of premium models. Passenger vehicle growth was muted, with low single-digit volume increases, while rising inventories and discounts raised concerns. Commercial vehicles underperformed, though a stronger second half was expected, with the festive season in focus.

About The Author

Next Story