What is a Short Put Butterfly option strategy

Written by Upstox Desk

Published on February 10, 2026 | 5 min read

A butterfly option strategy is a multi-leg, market neutral options strategy with limited profit and loss potential. The level of profit or loss is known at the time of taking position and thereby making it a reliable and risk defined strategy. Usually, a butterfly option strategy combines two spreads, i.e. it consists of two put options (one with a long position and the other with a short position) and two call options (one with a long position and the other with a short position). Therefore, a butterfly option strategy is a four-legged strategy, but uses only three options strikes.

A short put butterfly option strategy is formed by selling an out-of-the-money put option, buying two at-the-money put options and again selling in-the-money put options. In other words, the butterfly put option strategy is a combination of long put option spread and short put option spread.

Action | Qty | Option Type | Moneyness |

Sell | 1 | Put | OTM |

| Buy | 2 | Put | ATM |

Sell | 1 | Put | ITM |

The strategy is garnered to be neutral on market direction but plays on the possibility of rise in volatility. Along with being market neutral the risk and reward in the short put butterfly position options are limited and predetermined. This is a net credit strategy and since the short put butterfly spread is directional neutral, it has two breakeven points; Lower breakeven point = lower strike + net premium received Upper breakeven point = upper strike – net premium received

Two breakeven points would mean, there are two ways to profit from this strategy. The maximum profit potentials are achieved when the price of underlying security crosses either of the breakeven points, which can only happen when volatility rises and price changes rapidly. But since the strategy is defined as a limited risk-reward outcome the gains are limited to the quantum of option premium received. Profit = net premium received

On the flip side, when volatility shrinks and prices remain unchanged or within the two breakeven points. The maximum potential loss though limited, requires a bit of calculation; Loss = (Lower strike – middle strike + net premium received)

While deploying this strategy, it is important to remember that the strikes prices are set at equidistant from each other i.e difference between lower and middle strike is same as middle and higher strike price.

Illustration:

The Nifty50 index is currently trading at 17,530. A short put butterfly spread is initiated by buying 2 put options of Nifty50 at strike price of 17,550 at ₹165, which results in outflow and selling one out-of-the-money put option at strike 17,450 for ₹120 and one in-the-money put option at strike price of 17,650 for ₹225. We are able to secure a net inflow of ₹15.

| Strategy | Index | Action | Strike | Premium |

| Short Put Butterfly | Nifty50 | Sell Put | 17450 (strike 1) | 20 |

| Buy Put | 17550 (strike 2) | -65 | ||

Buy Put | 17550 (strike 3) | -65 | ||

| Sell Put | 17650 (strike 4) | 125 | ||

Net Premium | 15 |

*Strikes are arranged in ascending order and numbered accordingly.

The above neutral strategy provides two breakeven points to benefit from up move or down move of the underlying security.

Lower breakeven point = (strike 1 + net premium received) = 17,450 + 15 = 17,465 Upper breakeven point = (strike 4 – net premium received) 17,650 – 15 = 17,635

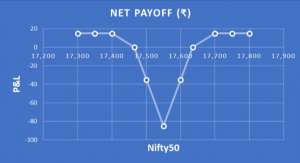

Payoff Schedule

Nifty50 @ Expiry | Net Payoff (₹) |

17,300 | 15 |

| 17,350 | 15 |

17,400 | 15 |

| 17,465 | 0 |

17,500 | -35 |

| 17,550 | -85 |

17,600 | -35 |

17,635 | 0 |

| 17,700 | 15 |

17,750 | 15 |

| 17,800 | 15 |

When Nifty50 expired anywhere above 17,700. The two long puts at 17,550 expire worthless and we lose the premium paid. We are able to retail the premium received from short put strikes at 17,450 and 17,650 respectively. Thus, the net premium received is the gain. Profit = Net premium received = ₹15

On the flipside, when Nifty50 expires within the breakeven points we are faced with a certain but limited loss. When Nifty50 expires at 17,500 we experience the maximum potential erosion of wealth. Loss = (strike 1 – strike 2 + net premium received) = (17,450 – 17,550 + 15) = - ₹85

Conclusion:

-

This is a net credit strategy, so there is no cash outflow at the time of initiation of the strategy.

-

It benefits from both time decay and increase in volatility. But one needs to figure the most optimal time of deploying the strategy. Deploying it very close to expiry, in order to take advantage of rapid time decay, would mean there is little for implied volatility to take effect.

-

The risk-to-reward ratio is generally unattractive for investors and therefore could discourage them.

-

The payoff of this spread is same as Long Iron Butterfly option strategy and Long Call Butterfly option strategy

About Author

Upstox Desk

Upstox Desk

Team of expert writers dedicated to providing insightful and comprehensive coverage on stock markets, economic trends, commodities, business developments, and personal finance. With a passion for delivering valuable information, the team strives to keep readers informed about the latest trends and developments in the financial world.

Read more from Upstox

Upstox is a leading Indian financial services company that offers online trading and investment services in stocks, commodities, currencies, mutual funds, and more. Founded in 2009 and headquartered in Mumbai, Upstox is backed by prominent investors including Ratan Tata, Tiger Global, and Kalaari Capital. It operates under RKSV Securities and is registered with SEBI, NSE, BSE, and other regulatory bodies, ensuring secure and compliant trading experiences.

Related articles

Futures and Options

What is the Expiration Time in Options Trading?4 min read | Written by Mariyam Sara

Futures and Options

How to Trade in Options with Small Capital: Strategies for Success6 min read | Written by Upstox Desk

Futures and Options

Top 5 Futures Trading Strategies You Should Know in 20262 min read | Written by Mariyam Sara

Futures and Options

Best Ways To Calculate Commodity Price Risks: Understanding The Main Risks Involved5 min read | Written by Upstox Desk