What is a call ratio backspread option strategy

Written by Upstox Desk

Published on February 10, 2026 | 5 min read

Call ratio backspread option strategy is a bullish option trading strategy that entails purchasing and selling call options. The strategy is intended to benefit from a significant increase in the price of the underlying stock in the near term.

The ratio in the call ratio backspread refers to the fact that a 2:1 ratio of long call options position against short call option position and “backspread” refers to long term or next month dated options that are commonly used thus affording more time for position to work in favor of traders or investors.

Bullish investors use the strategy to limit losses while expecting the underlying security to rise significantly. This strategy combines buying a large number of call options while selling a smaller number of calls at different strikes but with the same expiration date. While the downside is protected, gains can be substantial if the underlying security rises significantly due to the embedded ratio.

In this strategy volatility also plays a very important role. Usually, volatility is understood as a component that leads to premium erosion and reduction in value of option premium. But volatility can be of significant help to traders when timed appropriately.

Illustration:

The Call ratio backspread option strategy contains three legs as referenced in the above ratio of 2:1. The strategy involves buying two Out-of-the-Money call options and selling one In-the-Money call option. Both call options must have the same underlying security and the same expiration month. This strategy is generally deployed by traders or investors when they are moderately bullish on the price of underlying security and also expect volatility to increase.

The break even point calculation are as follows;

2 * (long call strike) – short call strike +/- net premium

In case of net premium resulting in an inflow, one more breakeven point gets added. Calculation for which are as follows;

(Short call strike + net premium received)

In theory maximum profit potential profit is unlimited, which occurs due to rise of price in underlying security, the two long call option position makes this strategy a net long call position. However, if the traders are able to establish this call ratio backspread for a net credit i.e premium received from short call is higher than premium paid for two long call positions, then there is potential of profiting from this strategy even if the price of underlying security falls instead of rising.

The maximum potential loss is limited to the difference in strike price of long and short call and net premium paid for long call option positions.

Call ratio backspread example

This is a three-legged option strategy with same underlying and same expiration month

Strategy | Index | Action | Strike | Premium |

Call Ratio Backspread | Nifty50 | Sell Call | 17,400 (strike 1) | 475 |

Buy Call | 17,800 (strike 2) | 225 | ||

Buy Call | 17,800 (strike 2) | 225 | ||

| Net Premium | 25 |

The spread between the two strikes is 400.

Max loss = (Spread – Net premium received) * lot size

= (400 – 25)

= (375) * 50

= -₹18,750

Lower breakeven point = (Strike 1 + premium received)

= 17,400 + 25

= 17,425

Upper breakeven point = (Strike 2 + max loss)

= 17,800 + 375

= 18,175

The strategy will be profitable if Nifty50 trades below 17,425 or above 18,125

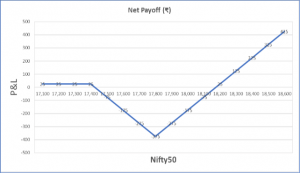

| Nifty50 @ Expiry | Net Payoff (₹) |

17,100 | 25 |

17,200 | 25 |

17,300 | 25 |

| 17,400 | 25 |

17,500 | -75 |

| 17,600 | -175 |

| 17,700 | -275 |

17,800 | -375 |

| 17,900 | -275 |

18,000 | -175 |

18,100 | -75 |

18,200 | 25 |

18,300 | 125 |

| 18,400 | 225 |

| 18,500 | 325 |

| 18,600 | 425 |

Conclusion:

Call ratio backspread option strategy will only result in profit if there is rapid change in price due to expansion of implied volatility. Generally, strikes with higher volatility are considered to be good entry points for setting up this spread. Another way to filter out potential counters for this strategy is to systematically look for stocks with higher-than-average volatility.

To improve odds in trading and increase profitability, traders deploy this strategy with certain variations, the most common being changing the ratio from commonly used norm of 2:1 to more complex and high leverage 3:2 and 3:1 combination. The addition of one more long call option positions leads to amplified gains in case of strong up move in price of underlying security.

Similar to call ratio backspread option strategy, which is deployed when traders are bullish on underlying security and expect increased in volatility, the put ratio backspread is deployed when traders are bearish and expect substantial down move in price of underlying security, along with increase in volatility. The ratio and nature of deployment would remain the same, traders shall buy 2 put options that are In-the-Money and short a put option that is slightly Out-of-the-Money.

Having said this, three legged option strategies with non-linear payoffs are often complex in nature and require active monitoring and therefore is recommended for retail investors with substantial knowledge of options trading.

About Author

Upstox Desk

Upstox Desk

Team of expert writers dedicated to providing insightful and comprehensive coverage on stock markets, economic trends, commodities, business developments, and personal finance. With a passion for delivering valuable information, the team strives to keep readers informed about the latest trends and developments in the financial world.

Read more from Upstox

Upstox is a leading Indian financial services company that offers online trading and investment services in stocks, commodities, currencies, mutual funds, and more. Founded in 2009 and headquartered in Mumbai, Upstox is backed by prominent investors including Ratan Tata, Tiger Global, and Kalaari Capital. It operates under RKSV Securities and is registered with SEBI, NSE, BSE, and other regulatory bodies, ensuring secure and compliant trading experiences.

Related articles

Futures and Options

What is the Expiration Time in Options Trading?4 min read | Written by Mariyam Sara

Futures and Options

How to Trade in Options with Small Capital: Strategies for Success6 min read | Written by Upstox Desk

Futures and Options

Top 5 Futures Trading Strategies You Should Know in 20262 min read | Written by Mariyam Sara

Futures and Options

Best Ways To Calculate Commodity Price Risks: Understanding The Main Risks Involved5 min read | Written by Upstox Desk