Synthetic Options Spread

Written by Upstox Desk

Published on July 31, 2025 | 5 min read

Options are popular instruments to trade in the market. And in many cases, whether one wants to speculate or hedge pre-existing positions or portfolio – options are the most cost-effective financial instrument that allows traders and investors alike to benefit from non-linear payoffs.

But such versatility often comes at the expense of opportunity cost. The Synthetic options spreads are a step-in direction to mitigate against adverse opportunity costs incurred by traders while trading all kinds of derivatives, including options.

What are Synthetic options spread

A synthetic options spread is a combination of various options positions (long or short, call or put) combined with either underlying security, usually referred to as “cash position” in market jargon or with futures position or both. A main objective of synthetic option spread is to emulate the payoff of another instrument using a combination of cash positions, options and futures. Meaning the payoff emerging from combination of options and underlying security could be identical as an individual position of futures contract.

In most cases when synthetic option spreads are created, the counter positions are usually in cash or futures and often of the same value or size. A synthetic structure can be implemented to emulate unlimited profit potential and limited loss, just like the regular call or put option but without the restriction of choosing the optimal strike. Apart from this, the synthetic spreads can also restrict unlimited risk emanating out of futures positions, especially when traded without proper hedge.

Arbitrage in Synthetic options

Put call parity theory is the prominent reason behind the existence of synthetic spreads. The theory states that holding a long call and a short put option, shall deliver a return profile similar to that of holding a long future. This is represented with a help of an equation;

Long Call option + Short Put option + Short futures = Zero

The put-call parity equation states that if one of the asset prices deviates from the relationship, an arbitrage opportunity will arise. This allows traders to exploit the opportunity by buying the underpriced asset and selling the overpriced asset.

There are 4 different type of synthetic option spreads;

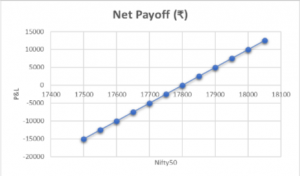

Synthetic Long Future

The futures contract payoff can be emulated by option spread. Suppose Nifty50 is currently at 17,796 and futures is trading at 17,810. Every 1-point variation in spot price will match 1 point change in futures. Now, instead of going long in the future and paying an upfront and maintenance margin. We can long a call option at strike 17,800 for ₹290 and short a put option at the same strike of 17,800 for ₹265. This would result in net premium outflow of ₹25.

Payoff for long synthetic option spread is remarkably identical to long Nifty50 futures payoff.

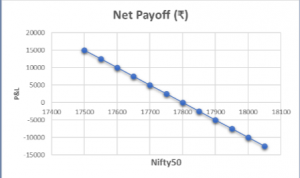

Synthetic Short Future

So, when an investor has a bearish outlook, it pays to construct synthetic short, instead of going short in the future. Continuing with the above example, if we short a call at strike of 17,800, we earn an upfront premium of ₹290 and buying a put option at strike of 17,800 would cost us ₹265. The resultant net inflow of ₹1250 (net premium received 25 * lot size 50) works massively in favor of spread holders, especially those looking to hedge their portfolios or pre-existing positions without paying anything upfront. Illustration for synthetic short future:

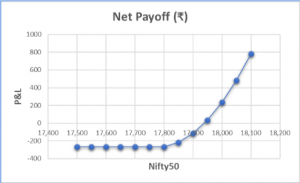

Synthetic Long Call

The payoff here resembles a long call option but is actually created by going long in Nifty50 futures contract at 17,810 and simultaneously buying a put option at strike 17,800 for premium of ₹265. The loss is limited and slightly higher than the premium paid. On the upside, the increase in Nifty 50 fetches gains but that is adjusted against premium paid. So Max profit = (Futures buy price - futures sell price – premium paid for long put) Max loss = (Futures buy price – Strike price + premium paid) = (17,810 -17,800 + 265) = ₹275

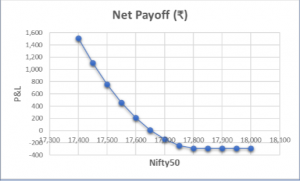

Synthetic Long Put

The payoff here can be equated to holding a long-put option. But the structure is created by shorting the Nifty50 futures at 17,810 and buying call options at strike 17,800 for ₹290. Again, here the losses are limited and slightly higher than premium paid for long call position, The Max profit is potentially unlimited but is adjusted against the net outflow of premium for long put option. Max Profit = (Futures sell price - Futures buy price – premium paid for long call) Max Loss = (Futures sell price – strike price + premium paid) = (17,810 - 17,800 + 290) = ₹300

Similarly, the synthetic spread can be structured to create Synthetic short call option spread and Synthetic short put option spread where the strategy would emulate the conventional short call and short put payoffs.

Conclusion:

- Synthetic long call option strategy is best deployed when markets are expected to rally upwards. The strategy minimizes losses when prices decline but ensures unlimited profit potential when the market rises. This is a sound strategy for investors looking to buy or accumulate additional stocks.

- Synthetic long put option strategy is used as an insurance against price correction and is best deployed when the outlook is bearish for underlying security. Sometimes it is also used as a hedge for a pre-existing short futures position. The losses again are limited in case of unexpected up move and potential profit remains unlimited when markets fall.

- Synthetic option spread can be used to limit downside and preserve capital.

The synthetic spread can be created using a pre-existing position in cash, futures and option contracts. This gives investors a lot of flexibility. As synthetic long or short spread is combined using multiple options, in case of a strong trending market, the loss making leg of strategy can be squared-off and the profiting options can be kept open.

About Author

Upstox Desk

Upstox Desk

Team of expert writers dedicated to providing insightful and comprehensive coverage on stock markets, economic trends, commodities, business developments, and personal finance. With a passion for delivering valuable information, the team strives to keep readers informed about the latest trends and developments in the financial world.

Read more from Upstox

Upstox is a leading Indian financial services company that offers online trading and investment services in stocks, commodities, currencies, mutual funds, and more. Founded in 2009 and headquartered in Mumbai, Upstox is backed by prominent investors including Ratan Tata, Tiger Global, and Kalaari Capital. It operates under RKSV Securities and is registered with SEBI, NSE, BSE, and other regulatory bodies, ensuring secure and compliant trading experiences.

Related articles

Futures and Options

What is the Expiration Time in Options Trading?4 min read | Written by Mariyam Sara

Futures and Options

How to Trade in Options with Small Capital: Strategies for Success6 min read | Written by Upstox Desk

Futures and Options

Top 5 Futures Trading Strategies You Should Know in 20262 min read | Written by Mariyam Sara

Futures and Options

Best Ways To Calculate Commodity Price Risks: Understanding The Main Risks Involved5 min read | Written by Upstox Desk