What is Credit Spread Strategies

Written by Upstox Desk

Published on October 24, 2025 | 6 min read

The credit spread strategy is an option strategy that involves buying and selling of options having the same underlying security and expiration but different strike. The spread is deployed in such a manner that there is a net inflow of option premium, thus leading to naming such strategies as “Credit Spreads”. Such strategies are simple to execute and tend to be highly popular with traders and investors, alike.

The net inflow of premium or “credit” happens at the initiation of the option strategy. This is done by selling At-the-money option strike, which possesses the highest time value and is expensive and buying Out-of-The-Money option strike which is cheaper. The credit spreads are further bifurcated into Credit Call spread and Credit Put spread.

Here the Call or Put refer to the instrument type being used to create spread. Generally, the value of call option increases with the increase in market levels and value of put increases with decline in market levels. However, with vertical spreads it is possible to generate profit with either call or put options in both rising and declining markets.

Illustration:

Credit Call Spread

Nifty 50 Index is currently trading at 17,580. A credit call spread is initiated by selling At-the-Money call option at strike 17,600 for ₹ 106 and buying Out-of-the-Money call option at strike of 17,800 for ₹ 40 of Nifty50 Index of the same expiry.

| Strategy | Index | Action | Strike | Premium |

| Credit call Spread | Nifty50 | Sell Call | 17,600 (strike 1) | 106 |

| Buy Call | 17,800 (strike 2) | -40 | ||

| Net Premium | 66 |

This results in net inflow of premium amounting to ₹66. The short At-the-Money call is more expensive than the long Out-of-the-Money call.

Breakeven Spread = Strike 1 + net premium

= 17,600 + 66 = 17,666

Max Loss = (strike 2 – strike 1 – net premium) * lot size

= (17,800 – 17,600 – 66) * 50 = 134 * 50 = ₹6,700

Max Profit = Net premium received * lot size

= 66 * 50 = ₹3,300

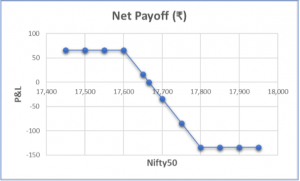

Payoff schedule

| Nifty50 @ Expiry | Net Payoff (₹) |

| 17,450 | 66 |

| 17,500 | 66 |

| 17,550 | 66 |

| 17,600 | 66 |

| 17,650 | 16 |

| 17,666 | 0 |

| 17,700 | -34 |

| 17,750 | -84 |

| 17,800 | -134 |

| 17,850 | -134 |

| 17,900 | -134 |

| 17,950 | -134 |

Payoff chart

Scenario 1 – Nifty50 expires at 17,400

The long call at 17,800 expires worthless leading to forfeiture of premium paid. The short call too expires worthless and without any intrinsic value but due to short trade the option is able to preserve its time value and we end up with retaining the credit equivalent to the premium received of ₹3,300.

Scenario 2 – Nifty50 expires at 17,650

The short call of 17,600 strike price retains 50 rupees as the intrinsic value while the long call options of 17,800 strike price expires worthless. As 17,650 is below the breakeven point of 17,666, the spread is able to retain a marginal portion of premium received i.e. ₹800 (17,666 – 17,650 = 16)

Scenario 3 – Nifty50 expires at 17,800

The short call position at 17,600 starts to bleed the spread, but the long call position at 17,800 provides cover against the potential unlimited loss. The loss is limited to the extent of difference between the two strikes minus net premium multiplied by the lot size which is ₹6,700 ((17,800 – 17,600 – 66 = 134) * 50).

Credit Put Spread

Nifty50 is currently trading at 17,775. The credit put spread can be initiated by selling At-the-Money put option of strike 17,800 at ₹ 110 and buying Out-of-the-Money strike of 17,600 at ₹ 40

| Strategy | Index | Action | Strike | Premium |

| Credit Put Spread | Nifty50 | Buy Put | 17,600 (strike 1) | -40 |

| Sell Put | 17,800 (strike 2) | 110 | ||

| Net Premium | 70 |

Here the spread generates a credit of ₹ 70.

Breakeven point = strike 2 – net premium received = 17,800 – 70 = 17,730

Max profit = Net premium received * lot size = 70 * 50 = ₹ 3,500

Max Loss = (strike 2 – strike 1 – 70) * lot size = (17,800 – 17,600 – 70) * 50 = 130 * 50 = ₹ 6,500

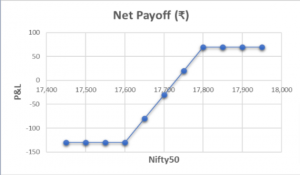

Payoff schedule

| Nifty50 @ Expiry | Net Payoff (₹) |

| 17,450 | -130 |

| 17,500 | -130 |

| 17,550 | -130 |

| 17,600 | -130 |

| 17,650 | -80 |

| 17,700 | -30 |

| 17,750 | 20 |

| 17,800 | 70 |

| 17,850 | 70 |

| 17,900 | 70 |

| 17,950 | 70 |

Payoff chart

Scenario 1 – Nifty50 expires at 17,450

The short put option position at 17,800 begins an incremental loss, leading to loss of upfront premium collected. The long-put option position at 17,600 helps in covering the incremental losses arising from short position. Since this is a risk defined strategy. The losses are limited to the difference between the two strikes minus net premium multiplied by the lot size Loss = (strike 2 – strike 1 – Net premium) * lot size = (17,800 – 17,600 – 70) * 50 = ₹6,500.

Therefore, when Nifty 50 expires at 17,450, a loss of ₹6,500 will be incurred.

Scenario 2 – Nifty50 expires at 17,750

The short put option of strike price 17,800 will retain ₹50 as intrinsic value while the long put option of strike price 17,600 will expire worthless. As 17,750 is slightly above the breakeven point of 17,730, the spread is able to retain a marginal portion of premium received i.e. ₹1,000 ((17,750 – 17,730 = 20)*50)

Profit = (Nifty50 at expiry - Break even point)* lot size = (17,750 – 17,730)*50 = ₹1,000

Therefore, when Nifty50 expires at 17,750, a profit of ₹1,000 will be incurred.

Scenario 3 – Nifty50 expires at 17,950

Both the options expire worthless and the trade is able to profit from this strategy. The profit is equivalent to net premium received and the same is the maximum potential profit of ₹ 3,500.

Profit = Net premium received * lot size = 70 * 50 = ₹ 3,500

Therefore, when Nifty50 expires at 17,950, a profit of ₹3,500 will be incurred.

Conclusion:

- Since the strategy is hedged, the quantum of profit and losses are pre-defined and limited.

- The strategy revolves around collecting or retaining the net credit or premium received, which leads to a positive impact of time decay on the strategy.

- The credit call spread is deployed when the outlook is bearish and traders expect significant decrease in volatility. The credit put spread on the other hand is deployed when the outlook is bullish and accompanied with contraction in volatility.

About Author

Upstox Desk

Upstox Desk

Team of expert writers dedicated to providing insightful and comprehensive coverage on stock markets, economic trends, commodities, business developments, and personal finance. With a passion for delivering valuable information, the team strives to keep readers informed about the latest trends and developments in the financial world.

Read more from Upstox

Upstox is a leading Indian financial services company that offers online trading and investment services in stocks, commodities, currencies, mutual funds, and more. Founded in 2009 and headquartered in Mumbai, Upstox is backed by prominent investors including Ratan Tata, Tiger Global, and Kalaari Capital. It operates under RKSV Securities and is registered with SEBI, NSE, BSE, and other regulatory bodies, ensuring secure and compliant trading experiences.

Related articles

Futures and Options

What is the Expiration Time in Options Trading?4 min read | Written by Mariyam Sara

Futures and Options

How to Trade in Options with Small Capital: Strategies for Success6 min read | Written by Upstox Desk

Futures and Options

Top 5 Futures Trading Strategies You Should Know in 20262 min read | Written by Mariyam Sara

Futures and Options

Best Ways To Calculate Commodity Price Risks: Understanding The Main Risks Involved5 min read | Written by Upstox Desk