Option Strategies

Introduction to the Long Straddle

Introduction to the Long Straddle

You must have come across the Hindi saying – ‘Chit bi meri pat bhi meri.’ Loosely translated it means ‘heads or tails I win.’ The Long Straddle Option Strategy works somewhat like that. Read on to see what it is and why use this strategy.

How do you construct a long straddle?

A Long Straddle consists of purchasing both a call and a put for the same strike price and expiration date.

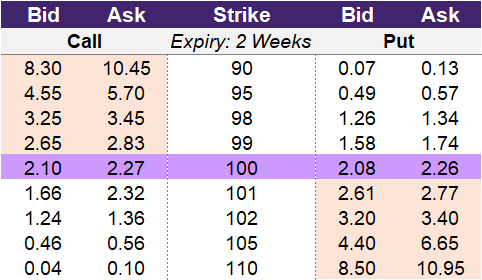

For example, if the underlying is trading at 100 and you believe that this security will move significantly from 100 in the near future you could enter into a straddle. You could select any strike, but as an example, you could purchase a call on the 100-strike, which would cost you the asking price of 2.27. You would also purchase a corresponding put on the 100-strike, which would cost you the asking price of 2.26. Therefore, the straddle would cost 4.53.

Illustration 1

Source: Upstox

Source: UpstoxWhy would a trader use a long straddle?

A trader will enter into a Straddle if they believe that the underlying will be volatile during the period prior to expiration. This trade works best when the underlying is less volatile before entering the trade and then becomes more volatile during the life of the options. The trader doesn’t have a specific forecast of bullish or bearish here but will be successful if any movement occurs in the security.

What is the max profit of a long straddle?

Key Formula:

- Long Straddle Max Profit (if the stock rises) = Unlimited – Total Premium Paid

- Long Straddle Max Profit (if the stock falls) = Strike Price – Total Premium Paid

The maximum gain and profit depend on the direction that the underlying moves. But do note that at any given time, either the call or the put will end up in the money, never both.

If the underlying security moves upwards, then the payoff will be similar to a call option. If the underlying price closes up significantly at expiration, the call will be valuable but the put will be worthless. Conversely, if the underlying security moves downwards, then the payoff will mimic that of a put option.

While it may seem that you are getting the benefit of both a call and a put, the drawback is that you are paying for both upfront. If the underlying price doesn’t move enough to offset the initial cost of buying both options, your trade will end in a loss.

How much can you lose trading a long straddle?

Key Formula:

- Long Straddle Maximum Loss = Total Premium Paid

The maximum loss is capped at the price you paid to enter the strategy. Using the table above, if the trader entered into a straddle with a 100-strike price, the trader will pay 2.27 for the call option and 2.26 for the put option. This total cost of 4.53 is the maximum loss for this strategy.

What is the breakeven point when entering a long straddle?

Key Formula:

- Long Straddle Upper Breakeven Point = Strike Price + Total Premium Paid

- Long Straddle Lower Breakeven Point = Strike Price – Total Premium Paid

The breakeven point when going long a straddle is the price at which the trader can make a profit. Because a straddle requires the purchase of two options, there are two breakeven points. To make a profit, the price of the underlying asset needs to move beyond the breakeven point in either direction. The upper breakeven point is the strike price plus the total premium paid to enter into the straddle. The lower breakeven point is the strike price minus the total premium paid to enter into the straddle.

A reminder about breakeven points is that these are for expiration. An option has both time value and intrinsic value prior to expiration. On expiration, an option only has intrinsic value. Because an option has time value remaining prior to expiry, the breakeven point of an option strategy will be less than on expiration. This is because a trader can exit the individual option contracts for a higher premium prior to expiry.

What is the profit formula for a long straddle?

Key Formula:

- Long Straddle Payoff = Max(0 Underlying Price – Strike Price) + Max(0 Strike Price – Underlying Price)

- Long Straddle Profit = Max(0 Underlying Price – Strike Price) + Max(0 Strike Price – Underlying Price) – Total Premium Paid

The profit formula for a long straddle combines the profit formulas for a long call and a long put. The profit formula for a long call is the maximum of 0 or the underlying price on expiration less the strike price. The profit formula for a long put is the maximum of 0 or the strike price less the underlying price on expiration. To determine the profit on expiry of a long straddle, the payoff of the two options (long call, long put) is reduced by the total premium paid to enter into the straddle.

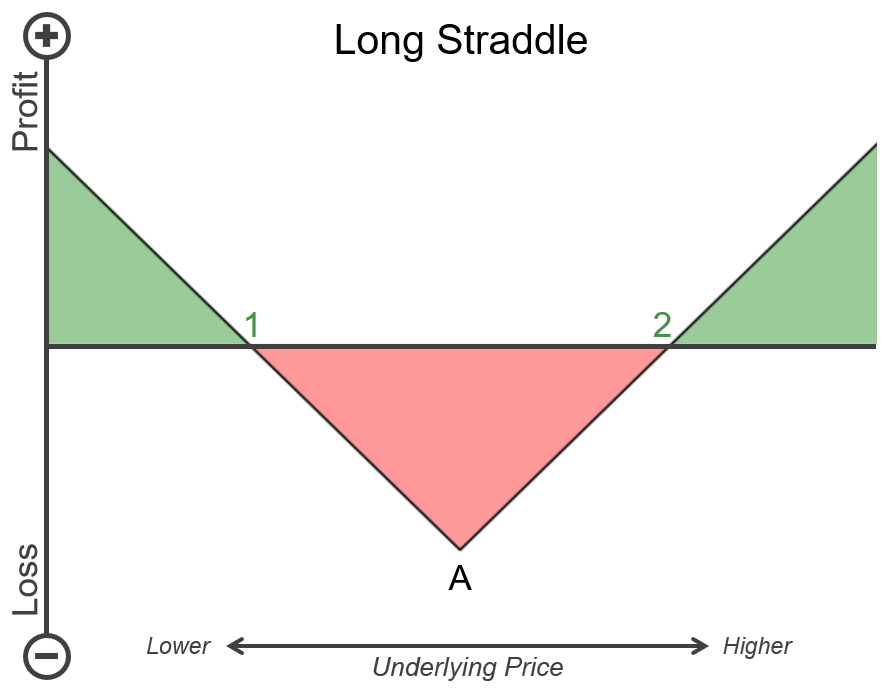

What is the payoff diagram for a long straddle?

Below is an example P&L diagram for a long straddle. Point A on the chart is the strike price selected for the long straddle. Point 1 is the lower breakeven point and is associated with the long put option. Point 2 is the upper breakeven point and is associated with the long call option. The vertical axis is the profit and loss, where the higher up represents more profit and further down is a higher loss. The horizontal is the underlying price. Further to the right is a higher underlying price, and further to the left is a lower underlying price. Areas that are shaded green are when the long straddle will have a positive payoff, and areas shaded red are when the long straddle will have a negative payoff.

Illustration 2

Source: Upstox

Source: UpstoxWhat is the point of max profit for a long straddle?

Key Formula:

- Price of Underlying = 0

or - Price of Underlying = ∞

The straddle doesn’t have a specific point of maximum profitability because the max profit isn’t capped. If the underlying keeps going up, the trader will earn more and more due to a rising value of the call option. If the underlying keeps going down, the trader will earn more and more due to a rising value of the put option. Technically, the max profit of a straddle occurs if the underlying rises to infinity or falls to zero.

What is the point of max loss for a long straddle?

Key Formula:

- Price of Underlying = Strike Price

The point of maximum loss for a long straddle occurs if the underlying doesn’t move at all. If the underlying moves a little from the strike price, then there will be a positive payoff for one of the options. If the underlying doesn’t reach one of the two breakeven points, the trader will suffer a loss. However, the max loss is if the underlying expires at the straddle’s strike price. In this case, the trader would lose the maximum amount, which is the total premium paid to enter into the long straddle.

Summary

- Use a long straddle option strategy if you believe the underlying could be volatile before expiry.

- This works best if volatility increases during the life of the options.

- Trader does not have a bullish or bearish outlook but benefits if any movement occurs in the security.

- To construct a long straddle, purchase both call and put options with the same strike price and expiry.

- Maximum gain and profit depend on the direction that the underlying moves.

- Either the call or the put will end up in the money, never both.

- If the underlying security moves upwards, then the payoff will be similar to a call option.

- If the underlying security moves downwards, then the payoff will be similar to a put option.

- Your trade is profitable only if the underlying moves enough to offset the cost of purchasing both call and put options.

- The maximum loss is capped at the price you paid to enter the strategy.

- A long straddle has two breakeven points.

Is this chapter helpful?

- Home/

- Introduction to the Long Straddle