Upstox Originals

Has the market given up on blue chips too soon?

6 min read | Updated on July 02, 2026, 16:11 IST

SUMMARY

For two years, India's biggest companies have been the market's most ignored. HDFC Bank is down ~26% in 2026. Infosys has fallen ~37% from its peak. ITC trades at nearly half its 10-year average valuation. But history, and the numbers, suggest the most boring trade on Dalal Street right now might quietly be its most compelling one.x

Stock list

For the past two years, India’s largest companies have given below market returns. | Image: Shutterstock

For years, the investing playbook seemed straightforward: buy large-cap blue chips and let time do the work. But lately, that script has changed.

Over the past year, while the Nifty 50 declined 4.9%, the Nifty Midcap 100 gained 7.5% and the Nifty Smallcap 100 rose 1.4%.

Even as the broader market corrected, investors continued to favour mid- and small-cap stocks over large-cap blue chips. PSU stocks became celebrities. Defence, railways, and power themes closed NFOs within days.

And through all of it, six of India's biggest, most fundamentally sound companies went nowhere.

Together, they form what Dalal Street has started calling the HRITHIK basket, HDFC Bank, Reliance Industries, Infosys, TCS, ITC, and Kotak Mahindra Bank. Six businesses that collectively represent India's banking system, its technology export engine, its largest conglomerate, and its most dominant consumer franchise. And for the better part of two years, all six have rewarded their shareholders with a mix of sideways movement, sharp corrections, and investor frustration.

Which raises a bigger question: has the market become so focused on what's exciting that it has started overlooking what's enduring?

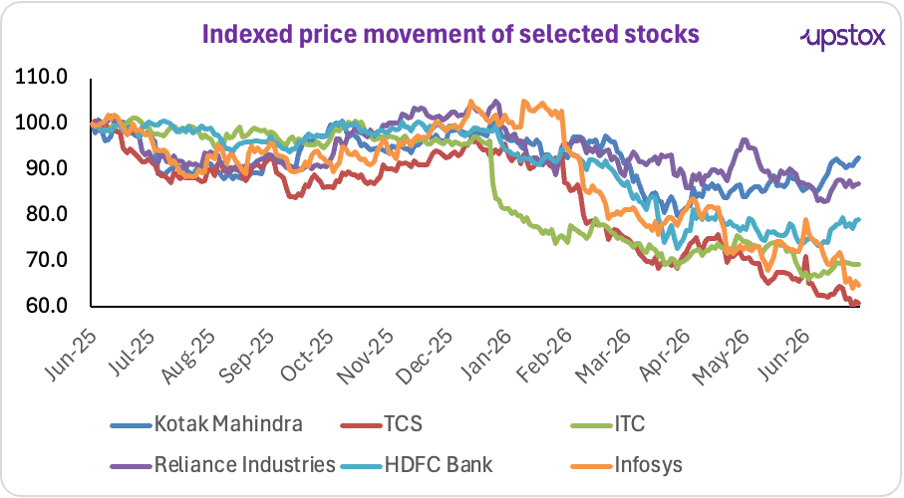

The chart below indexes each company's share price to 100 at the start of the period, allowing for a direct comparison of their relative market performance.

Source: NSE Share prices indexed to 100, as of Jun 27, 2026

Why have these heavyweights underperformed?

FIIs left, and they left in a hurry. Between January and April 2026 alone, Foreign Portfolio Investors pulled ₹1.98 lakh crore out of Indian equities, more than the ₹1.29 lakh crore that exited in all of CY2024. By May 2026, total CY2026 FII outflows had touched ~₹2.76 lakh crore.

| Period | FII Net Outflow |

|---|---|

| CY2024 | ~₹1,29,000 cr |

| CY2025 | ~₹2,40,000 cr |

| Jan–Apr 2026 | ~₹1,98,000 cr |

| CY2026 YTD* | ~₹2,76,388 cr |

Source: NSDL;*up to 29 Jun 2026

Liquidity challenges

Here is the part most investors missed. FIIs cannot exit mid-cap or small-cap positions quickly, the impact cost (the price slippage caused by a large sell order) would be devastating in illiquid names. So the selling always concentrates on the most liquid names on the exchange: HDFC Bank, Reliance, Infosys, TCS. India's strongest businesses took the hardest price hit, not because their fundamentals weakened, but because they were the only exit door wide enough for ₹2 lakh crore worth of institutional traffic.

Company-specific headwinds

HDFC Bank absorbed a ₹6.5 lakh crore mortgage book from the HDFC merger, compressing margins. Infosys issued weak FY27 revenue guidance of 1.5–3.5%. ITC faced higher cigarette taxes. Kotak went through a leadership transition following the RBI's directive on MD tenure. Each headwind was real. None was structural. But the market priced all of them as if they were.

Is the valuation case actually as strong as it looks?

According to a report by DSP Mutual Fund's NETRA, despite ~₹1.08 lakh crore in FII selling in March 2026, India's top 10 Nifty stocks showed no disruption in trading activity or impact costs. The P/E of the Nifty Top 10 Equal Weight Index had fallen to the 17th percentile since 2006, a level last observed only in 2016 and 2020, both of which were followed by significant large-cap re-ratings.

The Nifty's trailing P/E, which peaked near 24–25x in late 2024, has since compressed to 20.8x, close to its historical average. Meanwhile, several HRITHIK stocks trade at meaningful discounts to their own long-term valuation multiples, with non-banking companies trading below their historical P/E levels and banks below their historical P/B multiples.

| Company | Current P/E | 10-Year Avg P/E |

|---|---|---|

| Reliance Industries | 22.9x | 22.17x |

| Infosys | 14.0x | 22.39x |

| TCS | 14.5x | 26.11x |

| ITC | 17.4x | 21.6x |

| Banks | Current P/B | 10-Year Avg P/B |

| HDFC Bank | 2.11x | 3.58x |

| Kotak Mahindra Bank | 2.25x | ~4.1–4.4x |

Source: Screener, Yahoo Finance, Trendlyne, Tickertape, as of Jun 25, 2026

Put simply: you can buy India's mid-cap indices at a 29–60% premium to their own history, or you can buy India's blue-chip leaders at a 27–45% discount to their own history. Markets do not allow that gap to persist indefinitely.

What is actually happening inside these businesses?

Here is where the market narrative begins to diverge from business performance. While share prices remained under pressure, the underlying businesses continued to deliver resilient earnings and healthy operational performance across FY26. The stocks? Not so much.

| Company | FY26 PAT | YoY Growth |

|---|---|---|

| HDFC Bank | ~₹76,030 cr | 10.9% |

| Reliance Industries | ~₹95,610 cr | 17.8% |

| Infosys | ~₹29,474 cr | 10.2% |

| TCS | ~₹49,454 cr | 1.4% |

| ITC | ~21,018 cr | 4.9% |

| Kotak Mahindra Bank | ~₹14,008 cr | 2.0% |

Sources: Company Fillings

Has the market rotated like this before?

Look at the precedent set during previous Indian market cycles:

The 2017–2018 Pivot: In 2017, the Nifty Smallcap index rallied over 50%, pushing valuations into unchartered territory. In calendar year 2018, the small-cap index crashed by nearly 30%, while a handful of large-cap heavyweights (such as TCS, HDFC Bank, and Reliance) carried the Nifty 50 to positive territory.

The 2020 Recovery: Post-COVID, liquidity flooded small-caps. But as soon as inflation flared up globally, money safely nested back into mega-cap defensives. Why could the "old favourites" return?

The case for large caps goes beyond valuation.

Foreign investors typically prefer highly liquid large-cap stocks. With India's forex reserves at record highs and global conditions stabilising, any meaningful return of FII money is likely to favour Nifty 50 heavyweights.

Corporate capex among India's top 500 non financial companies has nearly doubled to around ₹10 lakh crore from pre-pandemic levels. Large cap leaders are both the biggest beneficiaries and the primary executors of this investment cycle.

More importantly, the HRITHIK stocks remain some of India's strongest businesses. What has changed is not their fundamentals, but their valuations. While the timing of a re-rating is uncertain, valuation gaps of this scale have rarely persisted indefinitely.

About The Author

Next Story