Upstox Originals

What Korea's explosive market rally teaches Indian investors

6 min read | Updated on June 03, 2026, 14:14 IST

SUMMARY

South Korea’s stock market has staged one of the most explosive comebacks, surging over 200%. Beneath the headline rally lies a far more interesting story: a two-stock market driven by AI chip giants and a decades-old governance problem finally being tackled. Discover why a growing economy isn't always enough to lift an index and what India must watch out for to ensure its own bull run doesn't run into a wall.

The South Korean equity markets have skyrocketed since mid 2025. | Image: Shutterstock

Ever heard of the Korea Discount?

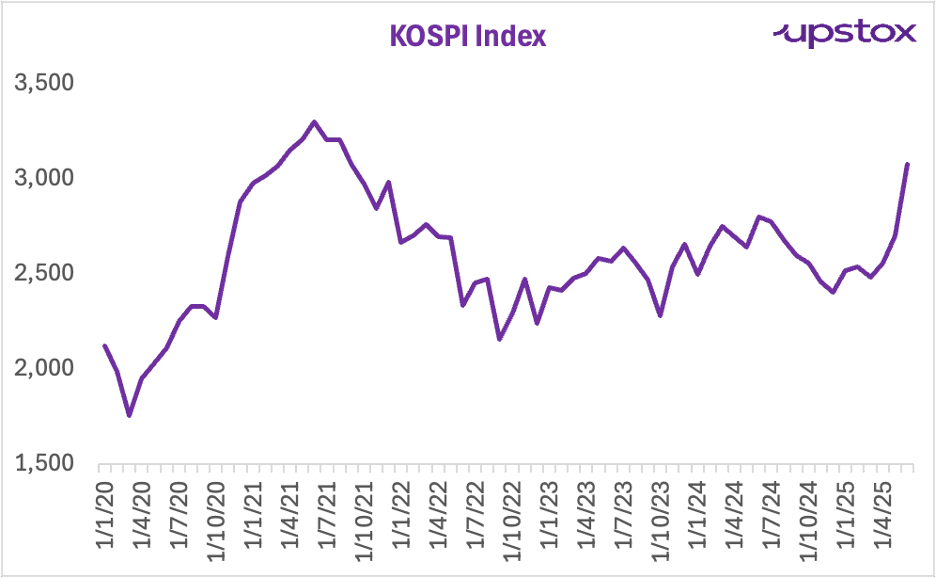

Not long ago, South Korea's stock market was something of a punchline. Despite being home to global giants like Samsung and Hyundai, despite being the world's sixth-largest exporter, the KOSPI — South Korea's benchmark index — went nowhere for years. This was referred to as the Korea Discount.

KOSPI Index (2021 - mid 2025)

Source: investing.com

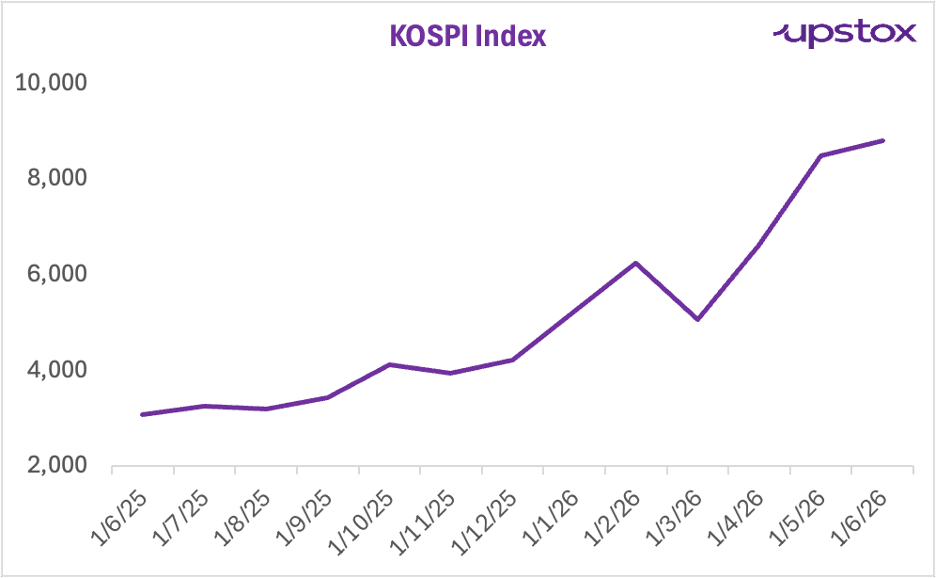

Then, almost without warning, everything changed.

KOSPI Index (June 2025 to June 2026)

Source: Investing.com

As seen below, the KOSPI has been one of the best-performing markets recently.

Global equity market performance comparison (select markets)

| Market / Index | 1-year returns | 2026 YTD Return* |

|---|---|---|

| South Korea (KOSPI) | 225.62% | 103.92% |

| USA (S&P 500) | 27.70% | 10.52% |

| Germany (DAX) | 5.26% | 2.65% |

| France (CAC 40) | 5.95% | 0.03% |

| India (NIFTY 50) | -5.40% | -10.57% |

Source: Google; *Returns as of June 1, 2026

So what happened? While European markets were flat or falling and India was navigating its own headwinds, Korea was rewriting record books. The contrast is stark.

What drove the rally — and is it real?

Two forces came together at the same time: 1) AI-driven earnings supercycle and 2) Governance changes

An earnings supercycle

South Korea is one of the countries at the centre of the AI revolution. Samsung Electronics and SK Hynix are the world's two dominant producers of High Bandwidth Memory (HBM), the specialised chips that are crucial to Nvidia's AI accelerators. The earnings numbers are staggering. In Q1 2026, SK Hynix reported an operating margin of 72% — higher than Nvidia (65%), TSMC (58%), Apple (35%), and Google (31%), according to the Seoul Economic Daily.

Governance revolution

The second ingredient is structural reform. For decades, Korean companies, particularly the family-controlled conglomerates called chaebols, had little incentive to reward ordinary shareholders. Inheritance laws made it advantageous for controlling families to keep stock prices low. Dividends were minimal.

South Korea's government set about changing this through its 'Value Up' programme. In July 2025, a landmark amendment to the Commercial Act required directors to act in the interest of all shareholders, not just the company.

Dividend taxes were reduced. Overseas activist funds — like AVI, Oasis, Palliser, Dalton — began setting up offices in Seoul.

But is it a broad rally?

Despite such a meteoric rise, of the 2,764 listed stocks, only 378 gained ground. The index is flying because only two companies — Samsung and SK Hynix — together powered the returns.

Samsung and SK Hynix market weight and performance

| Company | KOSPI Weight | 1-year share price returns |

|---|---|---|

| SK Hynix | ~21% | 1,038.8% |

| Samsung Electronics | ~21% | 514.4% |

Sources: Seoul Economic Daily, KED Global, TradingKey.

Sounds familiar? It should.

The United States has experienced a near-identical dynamic. The 'Magnificent Seven' — Apple, Microsoft, Nvidia, Alphabet, Amazon, Meta and Tesla — represent ~35-40% of the S&P 500's market capitalisation.

In 2023 and 2024, these seven companies contributed 84% and 73% of the NASDAQ and S&P 500's total returns, respectively. In Korea, there are just two stocks driving the index. In the US, there are seven. The pattern is the same: a narrow group of earnings giants lifting an entire index, while the broader market struggles to keep up.

What can Indian investors learn?

Here is where the Korea story stops being about Korea.

The lesson on governance

India has made real progress on corporate governance. But promoter concentration remains high, related-party transactions continue to be a concern in certain pockets, and the dividend culture is still developing in many sectors.

The lesson on concentration

India's NIFTY 50 is itself a concentrated index, with a handful of financial and IT names carrying significant weight. If the earnings growth of those companies stalls — as Korea's broader market found when chip stocks briefly corrected — the index can look deceptively weak even when pockets of the economy are doing well.

The lesson on patience

The Korea story also validates something that long-term investors know but struggle to internalise: markets can take a long time to reflect underlying value. Korean stocks were cheap for years. Cheap is not enough. Cheap plus catalyst is the combination that moves markets.

Can domestic Indian investors participate in the rally?

Very limited options. Indian investors can access the iShares MSCI South Korea ETF (please note: not a reccomendation), listed on the US stock exchange, by opening an international trading account through Indian brokers that offer US market access. This ETF tracks South Korean equities broadly, including the Samsung and SK Hynix positions, driving the rally. While you have access to Korean markets, Whether the risk-reward is appropriate for your portfolio is a question only you — and your financial advisor — can answer.

The bottom line

South Korea's market has seen one of the most remarkable comebacks in modern financial history. It was not luck. It was the product of genuine structural reform, an extraordinary earnings cycle driven by AI chip demand and a political moment that aligned underlying factors.

But the most important lesson is not about Korea. It is about what happens when a market lacks these ingredients. A country can grow. Companies can earn profits. And the stock market can still go nowhere for years — if governance is poor, if shareholders are not respected, and if earnings growth is concentrated in too narrow a slice of the economy.

India's long-term story remains compelling. But the Korean episode is a reminder of what it takes to make that story show up in investor returns.

About The Author

Next Story