Upstox Originals

Trading the rain: What the latest weather derivative means for Indian markets

7 min read | Updated on July 01, 2026, 13:29 IST

SUMMARY

For centuries, the Indian monsoon has shaped profits, harvests and livelihoods, yet nobody could hedge its risks. That just changed. With the launch of India's first weather derivative, businesses and traders can now take positions on rainfall itself. But is this a revolutionary tool for managing climate uncertainty, or merely a sophisticated wager on the weather?

RAINMUMBAI is a futures contract listed on NCDEX that lets you take a position on Mumbai's monsoon. | Image: Shutterstock

Picture two business owners, both watching the same monsoon sky. One runs a chain of ice-cream carts and prays the rain holds off. The other sells raincoats and prays that it pours. Same clouds, opposite fortunes. For as long as anyone can remember, both have simply had to take whatever the season handed them.

But now, they no longer have to. On May 29, 2026, India’s leading commodity exchange NCDEX launched a contract that lets a business, or a trader, bet directly on the monsoon. It is called a weather derivative, and while the concept is brand new to India, the idea finds its roots in the 1990s in the US.

So, what is a weather derivative?

A weather derivative is a contract that pays out based on a measured weather figure rather than on any damage suffered. That figure might be a season’s rainfall, a month’s average temperature, or a fortnight’s wind speed. Two parties agree on a level — say, the total rain in a season — and whoever is on the right side of it when the season ends collects from the other.

The first customers were power and gas utilities. Since then, the players have widened to farmers facing drought, construction firms losing days to rain. The fastest-growing users today are renewable-energy firms: a wind farm’s output depends on the wind and a solar park’s on the sun, and both can now pass that uncertainty to someone willing to carry it.

India’s missing weather market

In India, rain is more than weather — it's market sentiment. For the first time, that sentiment has a price a business can actually lock in.

India has never lacked weather risk — the monsoon still sets the rhythm of the rural economy. What it lacked was a market for that risk. Until now, the burden was carried almost entirely by the state, through vast crop-insurance schemes that enrolled a record 4.19 crore farmers in 2024-25 and cost the exchequer trillions of rupees.

Those schemes are insurance policies: subsidised, administered from the top, and long criticised as slow to pay.

But NCDEX’s RAINMUMBAI is a completely different product.

What is RAINMUMBAI?

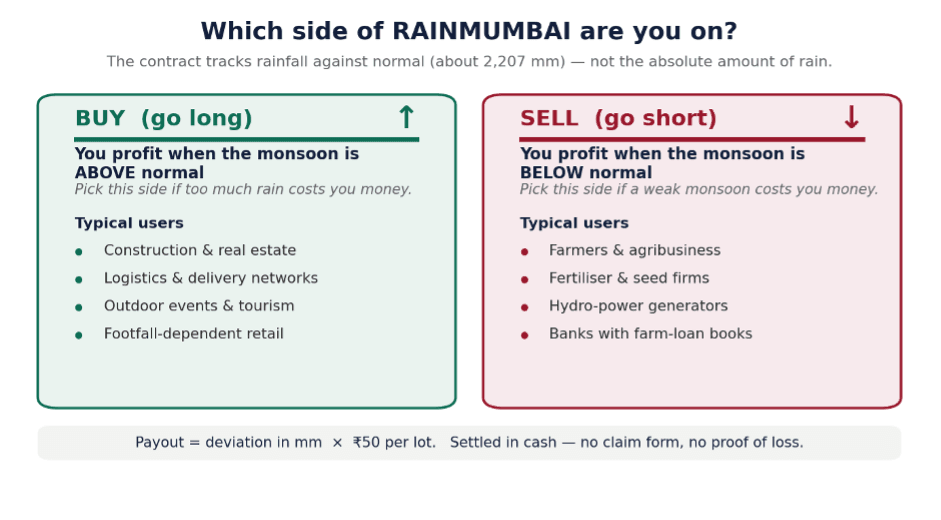

RAINMUMBAI is a futures contract listed on NCDEX that lets you take a position on Mumbai's monsoon. It launched on May 29, 2026 and trades through the season, roughly June to September.

The key thing to grasp: it does not track how much it rains in absolute terms. It tracks how far Mumbai's rain runs above or below normal.

"Normal" is a fixed benchmark called the Long Period Average (LPA —2,206.7 mm of rain across the four monsoon months, worked out from 30 years of IMD records (1991–2020) at two Mumbai stations, Colaba and Santacruz.

That gap between actual rain and normal is the whole game. It's measured by an index called Cumulative Deviation Rainfall (CDR):

- If it rains more than normal, the CDR is positive (a surplus).

- If it rains less than normal, the CDR is negative (a deficit).

And every 1 mm of that gap is worth ₹50 per lot. That single sentence is the heart of the contract.

How the index builds up, day by day

The index is "cumulative", which means it adds up as the season goes on. Each morning by 9:15, NCDEX takes yesterday's actual rainfall, compares it to what's normal for that date, and adds the difference to the running total. A tangible example from the methodology:

- June 1: normal for the day is 8.7 mm, but it doesn't rain. The season is now 8.7 mm behind normal.

- June 2: normal is 3.7 mm, again no rain. Now 12.4 mm behind.

Do that every day for four months and, by September 30, you have one number: how far the whole season landed above or below normal. That final number decides who pays whom.

Worked examples—how it actually pays out

The direction you take depends on which way rain hurts you. Remember, "up" means above the 2,207 mm normal, not just "a lot of rain."

A construction firm that loses money when it rains too much. Heavy rain means idle labour, stalled deliveries, and flooded sites. This firm buys RAINMUMBAI, so it profits if rain runs above normal.

Say, it buys 10 lots and the season ends 80 m above normal (CDR +80). Payout: 80 mm × ₹50 × 10 lots = ₹40,000, which helps cover the delay costs. If instead the monsoon is mild, the contract loses money—but the firm's sites ran on schedule, so it saved on the very costs it was hedging. That's the hedge working as intended: one side offsets the other.

Let’s look at another example.

A fertiliser dealer who loses money when the monsoon is weak. A poor monsoon means farmers buy less, so sales fall. This business does the opposite—it sells RAINMUMBAI, so it profits if rain falls below normal. If the season ends 30 mm short (CDR −30) on 10 lots, the payout is 30 × ₹50 × 10 = ₹15,000, cushioning the drop in sales.

A trader with no rain exposure at all. Someone who simply thinks this year's monsoon will beat forecasts can buy the contract purely as a bet, and sell it if they're right. No barn, no building site—just a view on the rain. This is the speculation side of the market, and it's what provides liquidity for the hedgers.

In every case, there's no claim form, no surveyor and no proof of loss—the weather station reads the sky and the money moves automatically.

What are the risks?

It's a Mumbai-only product, and has only two rain gauges. The contract settles on IMD’s reading from the Colaba and Santacruz stations. A builder in Navi Mumbai could be knee-deep in local flooding while the official index barely moves—so the hedge misses the very rain that hurt him. This is "basis risk," and it's the biggest practical limitation right now.

It's brand new, so trading is thin. Few participants means prices can jump around on small volumes and the gap between buy and sell prices can be wide.

The monsoon is genuinely hard to forecast. Even the IMD works with a margin of error, so getting the direction right is far from guaranteed.

It's not insurance. It pays on the rainfall number, not on damage to your crop, shop or building. It smoothens revenue, not physical loss.

Will it work?

The jury is still out.

On the face of it, a weather derivative is a useful product. A builder dreading a washout, a fertiliser firm fearing a weak season, or a trader with a view on the clouds can all take a position—no claim form, no loss adjuster.

It is a modest tool that does an unglamorous job for energy and farming that has boomed and busted before, and is reviving on the back of a warming planet.

For India, it is something more intriguing: the first attempt to attach a market price to the country’s single most important economic variable. Its success will depend on one thing above all: whether real hedgers—the farmers and utilities with genuine weather risk—actually turn up.

A weather market made only of speculators is just a casino with better data. But for a country that has lived at the mercy of the monsoon for centuries, simply having a way to trade it is a genuinely new chapter. That alone makes it worth watching the skies.

About The Author

Next Story