Upstox Originals

The $1.75 trillion question: what are investors really buying in SpaceX?

11 min read | Updated on May 29, 2026, 13:57 IST

SUMMARY

SpaceX’s IPO is built around three very different businesses: profitable Starlink, capital-heavy rockets, and a loss-making AI bet. At a possible $1.75 trillion valuation, the big question is simple, whether this IPO is a once-in-a-generation opportunity or an extremely expensive bet.

SpaceX wants to raise $75–80 billion at a valuation of $1.75 trillion. | Image: Shutterstock

Every few years, a company comes along that makes investors question everything they know about valuation. Amazon in 1997. Google in 2004. When those companies listed, the question was never whether they were real businesses. It was always: at this price, how much of the future are you paying for today?

SpaceX’s IPO, filed on 20 May 2026, is that moment for this decade, except the numbers are larger than anything seen before. The company wants to raise $75–80 billion at a valuation of $1.75 trillion. The fundraise alone would be nearly 3x Saudi Aramco’s 2019 IPO, the previous world record. If it lists at target, SpaceX enters the world’s top ten most valuable companies on day one, ahead of Tesla.

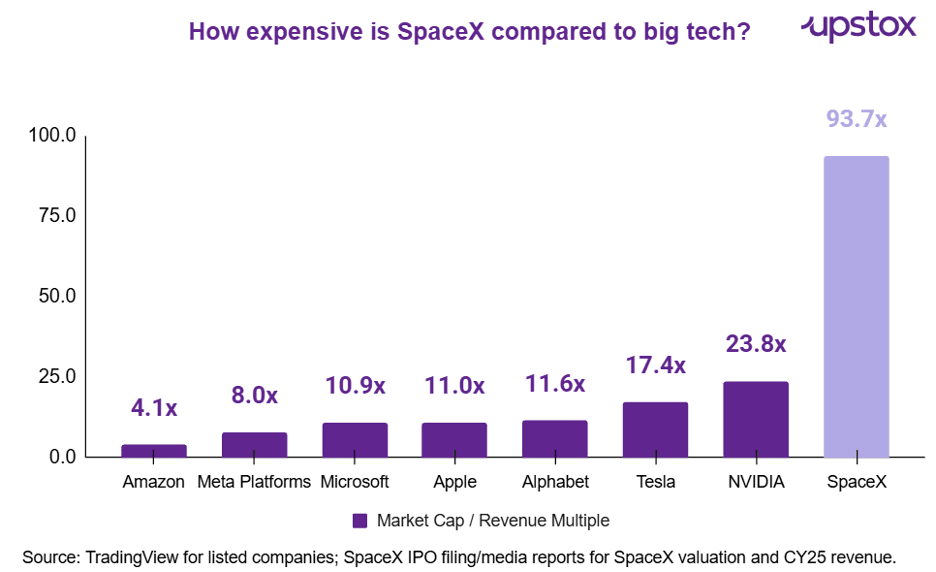

At $1.75 trillion, SpaceX would trade at nearly 93.7x revenue, far above NVIDIA at 23.8x, Tesla at 17.4x, and other big tech companies.

Three businesses, one price tag

SpaceX is best understood as three businesses packaged into one company.

| Business | What the business does | Current position |

|---|---|---|

| Space | Rockets, spacecraft, Starship, government, and commercial missions | Strategically important, but currently loss-making due to heavy investments |

| Connectivity / Starlink | Satellite internet and satellite-to-mobile connectivity | The strongest financial engine, with large revenue and operating profit |

| AI / xAI | Grok, X, and AI compute infrastructure | Biggest long-term opportunity, but currently the largest loss-maker |

Source: Company

SpaceX is best understood as three businesses packaged into one company: Space, Starlink, and AI. Each business plays a different role in the IPO story.

The Space business is the foundation. Falcon 9 is SpaceX’s proven reusable rocket, used for commercial launches, government missions, and Starlink satellite deployments. Starship is the next-generation rocket SpaceX is still developing. In simple terms, Falcon 9 supports today’s business, while Starship is the long-term bet.

SpaceX is spending heavily on Starship because it believes the rocket can carry larger payloads, reduce launch costs, and support the next phase of Starlink, AI infrastructure, and Mars-related ambitions. This spending is visible in the numbers. Space revenue fell 28.4% in Q1 2026, while operating losses widened from $70 million to $662 million in a year.

The Connectivity business, mainly Starlink, is the easiest part for investors to understand. As of March 31, 2026, SpaceX had around 9,600 Starlink broadband and mobile satellites in low-Earth orbit and served around 10.3 million subscribers across 164 countries, territories, and markets.

Starlink is also the company’s strongest financial engine. It generated $4.4 billion in operating profit in 2025 and $1.19 billion in Q1 2026 alone. But that strength is being used to support heavier spending in Space and AI.

The AI business is the newest and most debated part of the IPO. SpaceX acquired xAI in February 2026, bringing Grok, X, and AI compute infrastructure into the company. This has expanded SpaceX’s long-term market opportunity, but it has also increased losses and capex.

In Q1 2026, the AI segment reported an operating loss of $2.5 billion on revenue of around $820 million.

Below is the consolidated financial overview of the key business segments

Space segment - Key financials

| Metric | Q1 CY2025 | Q1 CY2026 |

|---|---|---|

| Launches | 38 | 40 |

| Segment income/loss | $(70) million | $(662) million |

| Segment Adjusted EBITDA | $224 million | $(351) million |

Source: SpaceX S-1 Filing

Connectivity / Starlink segment - Key financials

| Metric | Q1 CY2025 | Q1 CY2026 |

|---|---|---|

| Subscribers | 5.0 million | 10.3 million |

| ARPU | $86/month | $66/month |

| Segment income / loss | $1,033 million | $1,188 million |

| Segment Adjusted EBITDA | $1,618 million | $2,087 million |

Source: SpaceX S-1 Filing

AI / xAI - Key financials

| Metric | Q1 CY2025 | Q1 CY2026 |

|---|---|---|

| Nameplate compute draw | 0.3 GW | 1 GW |

| Segment income / loss | $(936) million | $(2,469) million |

| Segment Adjusted EBITDA | $(112) million | $(609) million |

Source: SpaceX S-1 Filing

Understanding why SpaceX is willing to absorb that requires looking at the market it believes it is chasing.

The $28.5tn bet behind the IPO

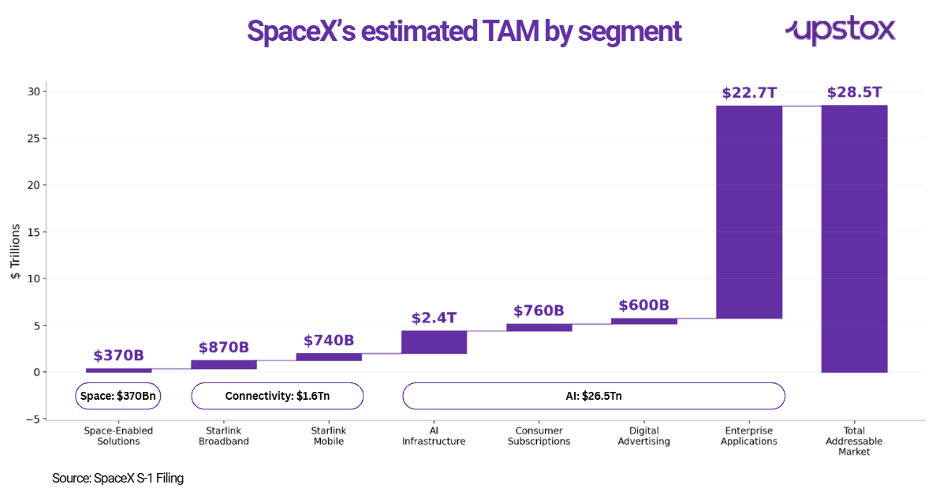

SpaceX’s IPO story is looking at a much larger opportunity. SpaceX estimates its total addressable market at $28.5 trillion across Space, Connectivity, and AI. But the key point is the split. Space and Connectivity together account for less than $2 trillion of this opportunity, while AI alone accounts for $26.5 trillion, mainly driven by enterprise applications.

This explains why AI has become so important to the SpaceX story. Without AI, SpaceX is a large space and satellite connectivity company. With AI, management is asking investors to value it as a much bigger technology infrastructure platform.

But this should be read carefully. TAM is not revenue or profit. It is the size of the market SpaceX believes it can chase. The real challenge is whether the company can convert this opportunity into actual earnings over time.

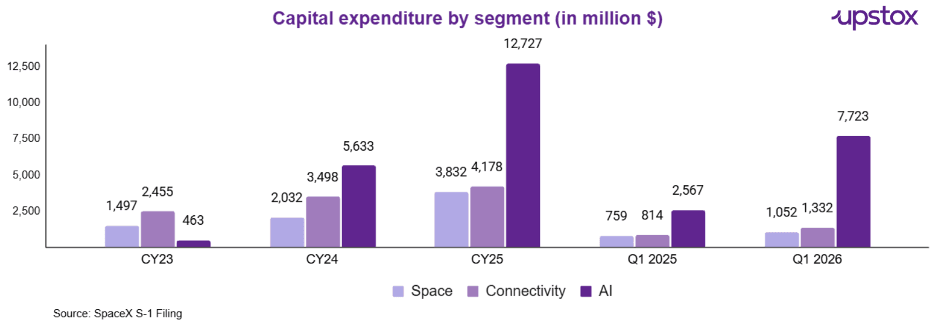

That ambition is also visible in how the company is spending. Total capex grew from $4.4 billion in 2023 to $20.7 billion in 2025. The AI segment alone accounted for $12.7 billion of that in 2025, rising from just $463 million in 2023. In Q1 2026, AI capex reached $7.7 billion out of a total $10.1 billion, more than Starlink and Space combined.

Capital expenditure

Orbital AI compute: SpaceX’s boldest AI bet

The most unusual part of SpaceX’s AI strategy is its plan to take computing into orbit. SpaceX describes orbital AI compute as satellite-based data centers that could use solar power and the space environment for cooling. The company says it expects to begin deploying these AI compute satellites as early as 2028.

This is where SpaceX’s three businesses connect. Rockets help launch the satellites, Starlink brings network experience, and the AI segment creates demand for large-scale compute. If this works, SpaceX will not just compete in AI models; it could compete in the infrastructure that powers AI.

But this is still an early and unproven idea. It will need large capex, regulatory approvals, technical execution, and real customer demand.

Peers across segments

SpaceX has no clean public-market peer because it operates across three very different businesses: rockets, satellite connectivity, and AI infrastructure.

In Connectivity, Starlink does not have a perfect comparable. Traditional telecom and satellite internet companies can be used as reference points, but Starlink is different because it combines satellite broadband with SpaceX’s own launch capability.

In the Space business, comparison is also difficult because many players are either private, government-owned, or part of larger groups. SpaceX stands apart because of its launch volume, reusable rocket model, and payload capacity.

In AI, SpaceX is again different. It is not only building AI models through xAI; it is also investing in compute infrastructure, data centers, and eventually orbital AI compute. The key point is simple: each SpaceX segment has peers, but no single company combines Starlink, reusable rockets, and AI infrastructure in one structure.

| Segment | Relevant Comparables |

|---|---|

| Connectivity | Viasat, HughesNet/EchoStar, Eutelsat OneWeb, Verizon, AT&T |

| Space | Rocket Lab, ULA, Arianespace, ISRO, Blue Origin |

| AI | Nvidia, Microsoft, Google, Amazon, CoreWeave, Cerebras, Groq |

Source: News reports

The key point is simple: each SpaceX segment has peers, but no single company matches the full combination of Starlink, reusable rockets, and AI infrastructure.

Why investors may consider SpaceX

SpaceX is not a clean, profitable company today. The investment case is that it owns assets that are very difficult to replicate: reusable rockets, a global satellite internet network, strong government and commercial relationships, and now a large AI infrastructure ambition.

Starlink is the strongest part of the story because it is already profitable at the segment level. The upside beyond Starlink comes from optionality. If Starship works at scale and AI compute becomes a real business, SpaceX could become much larger than a satellite internet company.

But both Starship and AI remain execution-heavy bets. That is why the IPO is not just a valuation of today’s SpaceX. It is a bet on what the company may become over the next decade.

Shareholding and governance

SpaceX is a founder-controlled company. The IPO shares are Class A shares with one vote per share, while Class B shares carry 10 votes per share. As of May 1, 2026, Elon Musk held 85.1% combined voting power before the offering, which means public investors will get economic exposure but limited control.

This structure allows SpaceX to pursue long-term bets like Starship and AI infrastructure without short-term market pressure. But it also creates governance risk, as major decisions will remain closely linked to Musk.

At the same time, SpaceX is not a one-person operation. Musk serves as CEO, CTO and Chairman, while leaders like Gwynne Shotwell, President and COO, and Bret Johnsen, CFO, are important to execution. For investors, the bet is not just on Musk’s vision, but on the team’s ability to deliver across rockets, Starlink, AI compute and orbital infrastructure.

What the $75–80bn will fund

The IPO proceeds are expected to support SpaceX’s growth strategy across three major areas: Starship development, AI compute infrastructure, and Starlink expansion. The filing also gives management flexibility to use proceeds for general corporate purposes.

Starship needs capital because it is central to SpaceX’s long-term space ambitions. Starlink needs capital because satellite deployment, international expansion and network capacity require continuous investment. AI needs capital because compute infrastructure is expensive and is now the largest driver of capex.

The filing does not give a fixed allocation for each use. So, investors are also trusting management’s capital allocation across several expensive projects.

Valuation: Defensible thesis or expensive leap of faith?

SpaceX’s EV-to-Adjusted EBITDA multiple at $1.75 trillion is roughly 260x, far above Tesla at ~145x and Nvidia at ~45x. There is no established public-market benchmark for a company like this. The standard valuation tools simply do not fit.

Different institutions have reached very different conclusions about what the company is worth:

| Institution | Implied Valuation | Reasoning |

|---|---|---|

| ARK Invest | $1.75T+; $2.5T by 2030 | Starlink + Starship + orbital AI |

| Scottish Mortgage Investment Trust | $1.25 trillion | Based only on verifiable transactions |

| Rainmaker Securities | $5T–10T long-term | Musk’s track record of execution |

| eToro analyst | $1.75T priced for perfection | Multi-segment execution risk |

Source: Media Articles

Scottish Mortgage, one of SpaceX’s longest-standing institutional backers, values the company at $1.25 trillion, a full $500 billion below the IPO ask, citing its policy of using only verifiable transactions to mark private holdings. ARK Invest sees $2.5 trillion by 2030. The gap between these two credible views is $1.25 trillion. That gap is a measure of the genuine uncertainty built into this price.

One structural dynamic that has received almost no coverage: once SPCX begins trading, Nasdaq’s fast-entry rule means it automatically qualifies for the Nasdaq-100 after just 15 days. That could trigger buying from every ETF and index fund tracking the index, trillions in passively managed capital that must buy SPCX regardless of valuation view.

Key risks

-

xAI regulatory scrutiny: UK and EU have opened formal investigations into Grok; multiple US state attorneys general have demanded action; SpaceX has set aside $500 million for potential legal losses from content-related lawsuits

-

Governance concentration: Musk controls 85.1% of votes; public shareholders have no meaningful say in board composition or major corporate decisions

-

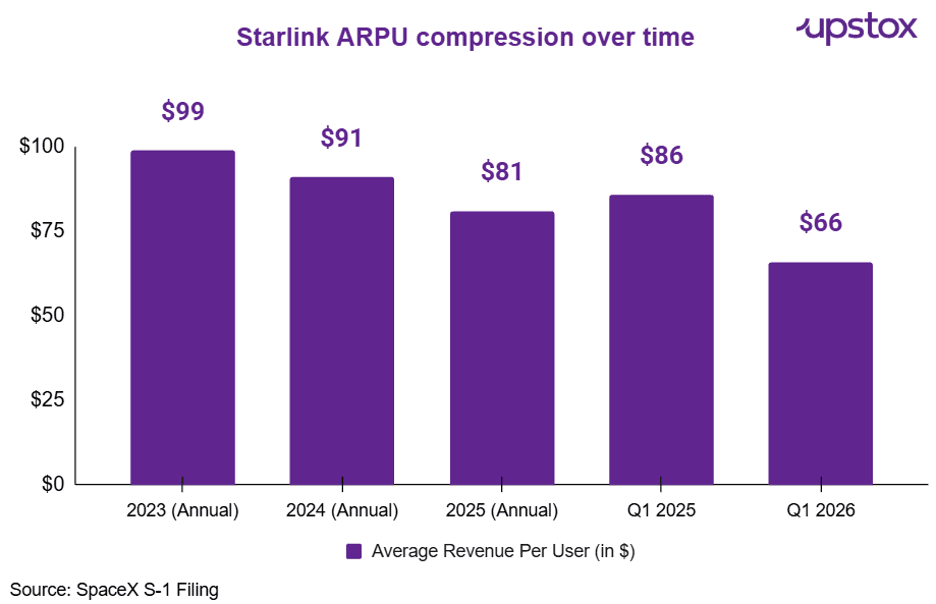

ARPU compression: Starlink’s revenue per subscriber has fallen 33% year-on-year; per-unit economics are weakening even as subscriber volumes grow

-

Starship execution risk: The company explicitly warns that delays in Starship development or cost targets could undermine the entire growth strategy

-

Dual leadership risk: Musk simultaneously runs Tesla, SpaceX, and xAI — a governance concern flagged in the prospectus itself

-

Orbital AI unproven: FCC approval for up to 1 million solar-powered AI satellites has not cleared regulatory review

Before you go

SpaceX is chasing a $28.5 trillion opportunity across Space, Connectivity and AI, but the company gives no clear timeline for consolidated profitability. The path depends on three things: Starlink staying profitable, Starship improving launch economics, and AI compute becoming a real revenue engine.

If Starship delivers, orbital AI scales, and Starlink’s subscriber growth offsets ARPU compression, this valuation could look cheap a decade from now. But if xAI’s regulatory risks deepen or Starship timelines slip further, the losses will belong to public shareholders who have limited voting power to change course.

That is why this is not a normal space company listing. At a possible $1.75 trillion valuation, investors must decide whether they are buying the future early or paying too much for it today.

About The Author

Next Story