Upstox Originals

South Korea's stock market crash: What's really going on?

7 min read | Updated on July 14, 2026, 14:39 IST

SUMMARY

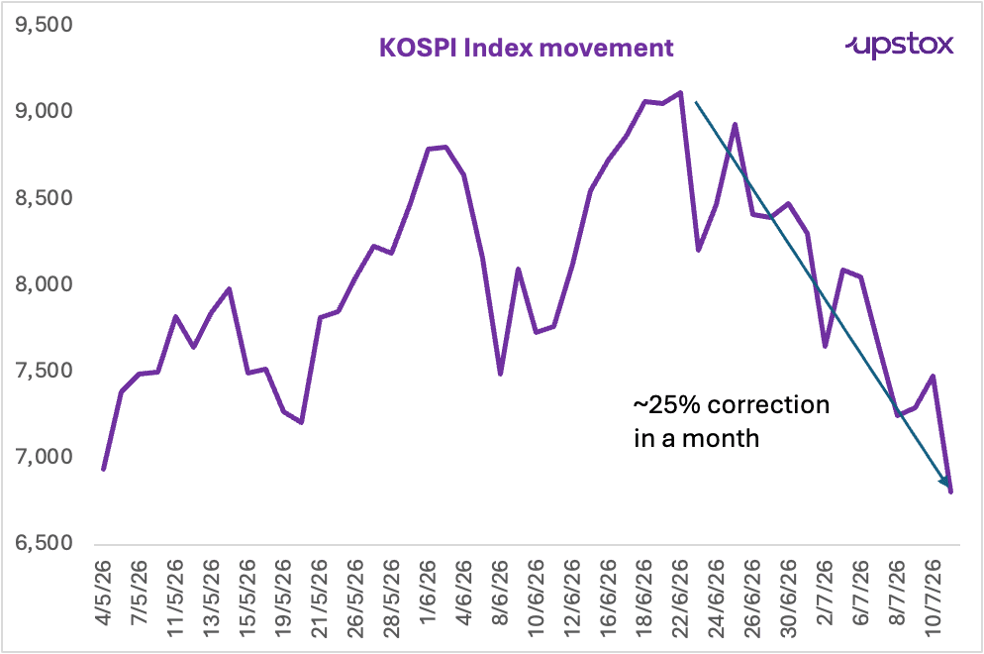

25%, that’s how much the South Korean markets have corrected in less than a month. Typically, that would stoke fears of a recession. It has triggered trading halts and dragged the US markets down with it. The obvious conclusion is that the‘AI bubble has burst.’ But the real story is that the market is so dependent on two companies that it has led to forced selling. Here's what's driving the sell-off, who's actually selling, and whether there's reason to worry.

South Korean markets have corrected almost 25% from their top this year. | Image: Shutterstock

South Korea's stock market has crashed, recovered, and crashed again — sometimes all in the same week. Three weeks into the fall, investors still can't agree whether it's a warning sign or just noise.

Source: Investing.in; *Data as of 13-07-2026

A 25% correction in less than a month would typically stoke fears of a bear market.

So, what is going on?

South Korea's KOSPI index crossed 9,000 points for the first time in its history on June 18, 2026, hit a fresh record high days later, and then began unravelling. Since then, it has triggered trading halts multiple times, wiped out hundreds of billions of dollars from Samsung Electronics and SK Hynix alone.

| Date | What happened to KOSPI |

|---|---|

| 18 June | Crosses 9,000 points for the first time in its history |

| 22 June | KOSPI hits a fresh all-time record high |

| 23 June | Plunges roughly 10% intraday; circuit breaker triggered as AI valuation fears spread from Wall Street |

| 2 July | Another ~8% fall as a fresh US semiconductor sell-off hits Samsung Electronics and SK Hynix |

| 7 July | Kospi falls 4.91% to close at 7,656.31 — the index's 11th circuit breaker ever, and sixth this year |

| 9-10 July | Index stabilises near 7,200-7,300; foreign investors turn net buyers for two straight sessions |

| 13 July (today) | A fresh 'sidecar' trading halt is triggered — the 18th of the year — as volatility persists |

Source: News articles

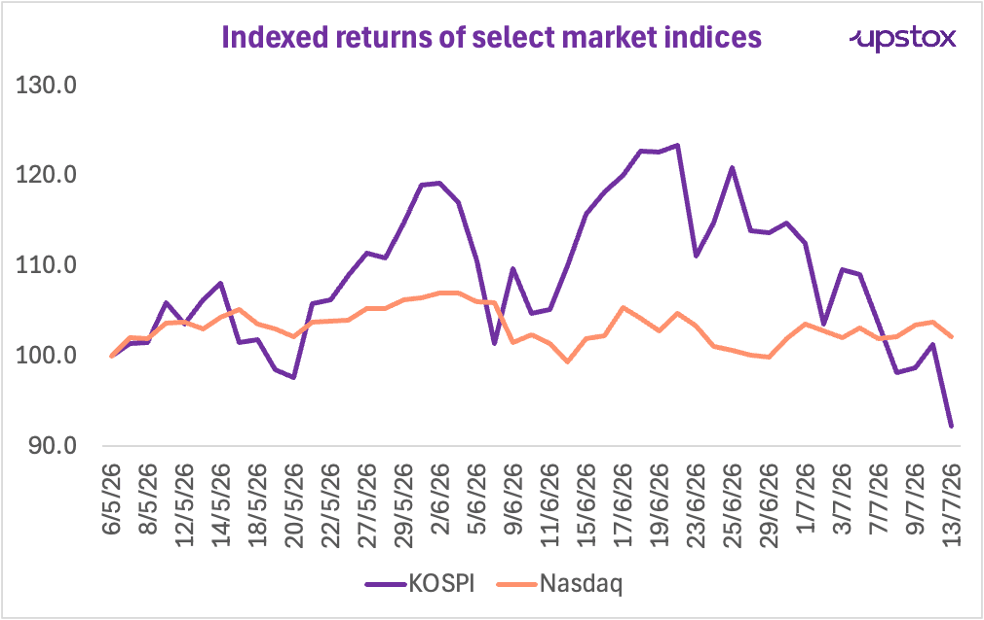

On bad days, it even dragged the US markets down with it.

Source: Investing.in; *Data as of 13-07-2026

The obvious conclusion is that the ‘AI bubble has burst.’ But industry experts are not even calling this a “crisis”.

The real culprit: Forced sellers

Here's the twist most headlines miss. Korea's sell-off looks, on the surface, like classic fear-driven panic.

Through the first half of 2026, foreign investors net-sold a record 148.32 trillion won (roughly $95 billion) worth of KOSPI shares — the largest outflow in the first-half ever — even as the index itself nearly doubled. Nearly 90% of that selling was concentrated in just two stocks: Samsung Electronics and SK Hynix.

Why would anyone dump the two companies leading the rally? According to analysts at Nomura and Goldman Sachs, this has had less to do with losing faith in Korea and more to do with maths.

Large global funds that track benchmarks like the MSCI Emerging Markets Index don't buy as much of a stock as they'd like. They follow a rulebook: each country's stocks are only allowed to make up a certain slice of the fund's money, based on how large that country is within the benchmark index.

Let’s take a simple example to understand it better.

As of April 2026, South Korea's weight in the MSCI Emerging Markets Index stood at 18.69%. Most large global funds therefore, will keep the total weight of Korean stocks around this range.

So when Samsung Electronics and SK Hynix kept climbing — Samsung up over 130% and SK Hynix up more than 270% at one point — Korea's slice of the index kept increasing, purely on price gains, with no fund manager buying a single extra share.

Once Korea's weight pushed past what these funds were allowed to hold, they had to trim their positions regardless of how bullish they still were on the companies. That's why foreign investors ended up selling billions of dollars worth of Korean chip stocks even as several brokerages kept "buy" ratings on them — the selling wasn't a verdict on Samsung or SK Hynix, it was funds automatically reverting to their own rulebook.

Nomura's Asia-Pacific equity strategist, Chetan Seth, described this dynamic as "essentially forced selling" — an automatic side effect of Korea's success, not a verdict on it.

Is this the AI trade seeing a dotcom-style crash?

Every fall in Korea spilled over to to Wall Street As well. A disappointing forecast from US chipmaker Broadcom in late June, for instance, hit chip stocks worldwide, Korea included.

That has revived a debate: is the AI rally the new dotcom bubble? The bulls and the bears agree on the facts, but not on what they mean.

| The bull case | The bear case |

|---|---|

| Goldman Sachs has a 12-month KOSPI target of 12,000, implying meaningful further upside from current levels. | Michael Burry (who famously predicted the 2008 crash) has taken large put option positions against the semiconductor ETF SOXX, along with Nvidia, Oracle and Palantir, betting on a correction. |

| Samsung Electronics is projected to generate around 300 trillion won in free cash flow in 2026, funding record dividends and buybacks. | The Philadelphia Semiconductor Index has surged 65-69% so far in 2026 alone, a pace some analysts compare to the months before the 2000 dotcom crash. |

| SK Hynix's free cash flow of roughly 220 trillion won is expected to fund a similarly large shareholder-return programme. | Certain brokerages estimate that a further 260 trillion won of foreign selling is still possible if ownership levels normalise. |

Source: News articles

The honest answer is that both camps are working off real data — the question was never really whether AI is transformative (most agree it is), but whether prices have already priced in a future that goes perfectly to plan.

Why Korean markets swing more than global peers

If the AI-valuation jitters are global, why do Korean markets move so much more sharply than US or even Japanese markets? Three home-grown amplifiers explain most of it.

-

First, concentration: Samsung and SK Hynix alone make up roughly half of the KOSPI's total value, so whatever happens to the two companies happens to the entire index.

-

Second, leverage: South Korea's deputy prime minister, Koo Yun-cheol, has explicitly pointed to leveraged ETFs as a source of amplified volatility, and the government is now discussing ‘supplementary measures’ to ease the volatility.

-

Third, rule-based selling closer to home: the National Pension Service is required to trim its domestic equity holdings once they cross a set threshold, meaning Korea's own pension fund can become a forced seller purely because the market has risen too far, too fast. To add to that, the Korean won has weakened from 1,483 per dollar in May to above 1,530 in July, which triggers further foreign selling to limit currency losses, and small shocks get amplified into large ones.

What Seoul is doing about it

Financial regulators and the Bank of Korea have been holding joint market-monitoring meetings through the volatility, and the finance minister met the central bank governor and regulators on 8 July specifically to discuss the risk of further swings. A special inspection into short-selling practices is also underway.

So, should you be worried?

Here's the number that puts everything in perspective: even after three weeks of selling, the KOSPI is still 60% higher on a YTD basis. This looks far more like a hangover after an extraordinary party than the start of a collapse.

The genuine risk isn't that the AI story is fictional — it's that Korea's market structure (heavy concentration, leveraged products, and rule-bound forced sellers) can turn an ordinary global wobble into an extraordinary local one. That's a story about market plumbing, not about whether AI, or Korea's economy, has a future.

About The Author

Next Story