Upstox Originals

Is India’s credit card market entering a reset phase?

4 min read | Updated on April 27, 2026, 11:38 IST

SUMMARY

Credit card perks in India like lounge access, cashback, milestone rewards, are no longer the easy wins they used to be. Banks are tightening eligibility, raising spend thresholds, and closing reward loopholes as rising usage volumes make generosity expensive. What once felt like a standard perk now requires serious wallet commitment.

Credit cards have significantly scaled back their benefits. | Image source: Shutterstock

Credit cards in India were starting to look less like payment tools and more like subscriptions to small luxuries.

Swipe enough and you got lounge access, cashback, reward points, and the occasional free hotel stay or flight deal. Banks were happy to play along, until the costs started adding up.

Now, the perks are being cut, the rules are getting tighter, and what once felt like easy value is becoming harder to unlock.

Why are we saying this? Look at the cut in rewards for some of the more prominent cards

| Card / Program | Earlier Benefit | Current or New Structure |

|---|---|---|

| HDFC Infinia | Relatively easy to retain as a premium card, with even ₹8–12 lakh annual spenders often continuing without strict thresholds. | Retention now requires ₹18 lakh annual card spend or ₹50 lakh relationship value. |

| Amex Platinum Travel | More generous milestone rewards, with 15,000 MR points at ₹1.9 lakh spend and a Taj voucher plus 10,000 MR points at ₹4 lakh spend. | Milestone rewards have been cut to 7,500 MR points at ₹1.9 lakh spend, while the ₹4 lakh milestone now offers 10,000 MR points without the Taj voucher. |

| ICICI Emeralde Private | Accelerated rewards on Amazon Pay / Swiggy / iShop vouchers (e.g., 6×). | Accelerated rewards removed; only base points on these vouchers. |

| Scapia (Federal/BoB) | Easier lounge access with lower monthly spend thresholds (~₹10k). | Lounge access now requires higher monthly spend (~₹20k/month), with exclusions on some categories. |

| SBI Card variants | Up to 8 complimentary domestic lounge visits per year on select cards. | Domestic lounge visits reduced; visit quotas tightened with structured caps. |

Source: News articles

Across cards, benefits are not disappearing entirely; they are being pushed behind higher spends, tighter conditions, and narrower use cases. The shift is clear: rewards are moving from being easy to access to being earned.

Why rewards are becoming harder to sustain

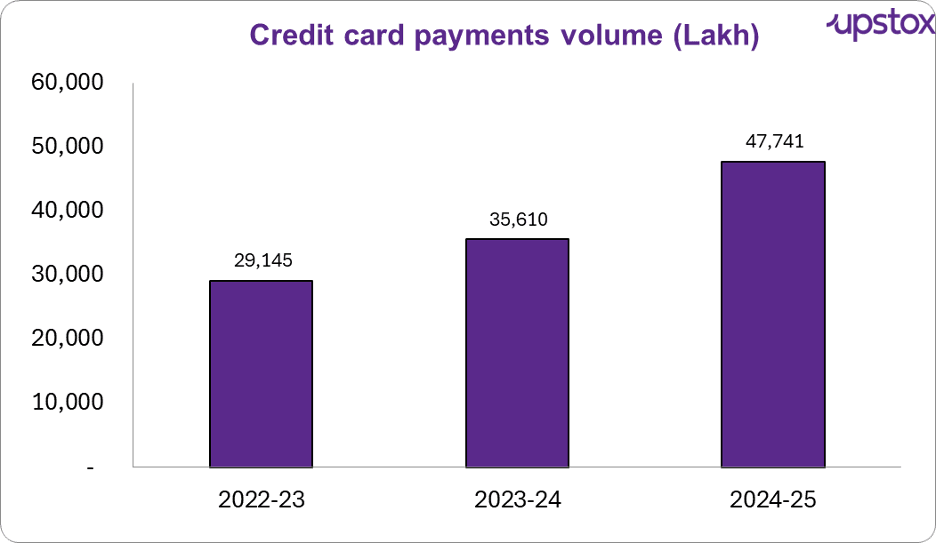

India’s credit card boom has been sharp, and it is visible first in how often people are using their cards.

Credit card payment volumes have risen by nearly 64% over the past two years. Cards are no longer occasional-use products; they are becoming part of everyday spending behaviour.

Source: RBI reports

That matters because rewards become costlier for banks when usage becomes habitual. Lounge access, cashback, and reward points were easier to offer when cards were used by a smaller base and with lower frequency. Once transaction volumes surge, the cost of keeping those benefits alive rises quickly.

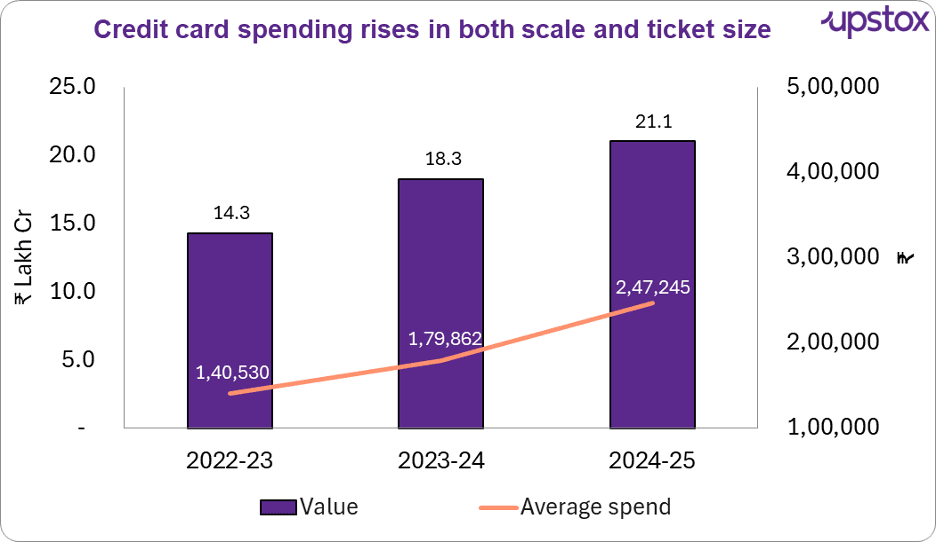

The second shift is in the size of spending.

The total value of credit card payments has grown by about 47% over the same period, crossing ₹21 lakh crore in FY25. So, this is not just about more swipes, it is also about much larger sums moving through cards.

Source: RBI reports,

Note:- Average spend is derived by dividing total credit card payment value by the number of users in each year.

In theory, higher spending should be good news for banks. But the data now shows that not only is total card spending rising, the average spend per user is increasing as well. But higher spending has not translated into higher profitability, and that is a big reason banks are acting now.

Fewer customers are carrying balances and paying interest. The revolver rate (customers who roll over unpaid dues and pay interest) has fallen from over 40% pre-pandemic to around 23–25% now, weakening one of the most profitable parts of the card business.

At the same time, regulation has made this business more expensive. In November 2023, the RBI raised risk weights on credit card exposures from 100% to 125%, forcing banks to hold more capital against this lending.

Add to that rising stress, credit card NPAs have increased by over 28% year-on-year, reaching around ₹6,700 crore, and the economics start to tighten even as spending grows.

That is why rewards are becoming harder to sustain. The credit card business is getting bigger, but the economics of generosity are getting weaker.

Before you go

With more than 100 million credit cards now in force, perks that once felt premium are no longer exclusive.

Banks are responding by making rewards harder to access. Lounge visits, cashback, and milestone benefits are increasingly being tied to higher spends and tighter conditions. That is the larger shift. Credit card rewards are no longer broad-based freebies. They are becoming more selective.

About The Author

Next Story