Upstox Originals

India's corporate bond market is losing steam

5 min read | Updated on May 19, 2026, 14:10 IST

SUMMARY

India’s corporate bond market, at 18% of GDP, remains tiny compared to most global peers. But now, there’s another problem emerging: bond issuances are weakening, companies are favouring equity, and NBFCs are drifting back toward bank loans. So, is this just a temporary rate-cycle problem? Or is India’s corporate bond market revealing deeper structural cracks?

India's corporate bond market could grow from roughly 18% of GDP today to around 35% by 2030 | Image: Shutterstock

India’s corporate bond market may be entering a tricky phase as companies slowly rethink how they want to borrow money.

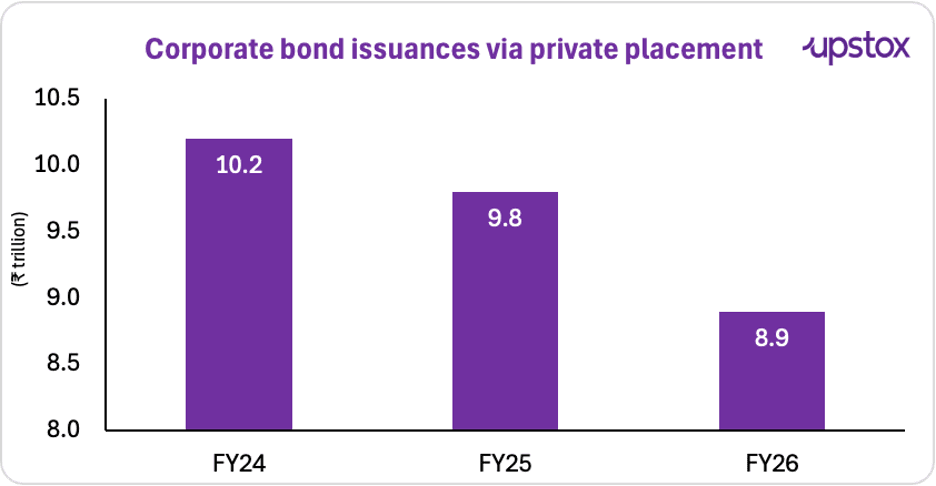

Bond issuances via private placements fell from ₹10.2 trillion in FY24 to ₹9.8 trillion in FY25, and then again to ₹8.9 trillion in FY26.

Now, sure, rising bond yields are part of it. So is the shift toward equity markets, where companies are hoping for rich valuations instead of taking on more debt.

But is that the whole story? Maybe not.

Because there are structural issues underneath all this, too. India’s bond market still remains relatively narrow and concentrated, with a large chunk of issuances coming from a small set of highly rated borrowers.

Which means the moment borrowing conditions tighten, the slowdown starts showing up very quickly.

Source: News articles

Why is this happening?

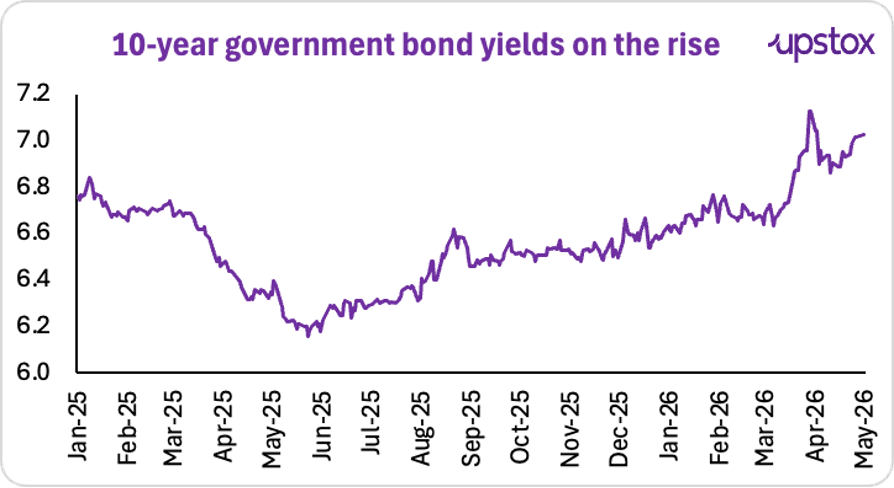

Government bonds (G-sec) are considered to be the safest. Therefore, the cost of borrowing for the companies is typically higher than the G-sec rate. With consistently rising G-sec rates, corporate borrowing gets more expensive too. The 10-year yield stood around 7.01% on May 4, 2026, crossing the 7% mark for the first time since July 2024.

Source: Investing.com *Data as of May 4, 2026

Second, equity markets are looking more attractive. India saw 113 mainboard IPOs raise ₹1.91 lakh crore in FY26, up from ₹1.82 lakh crore in FY25. Overall public equity fundraising during the year stood at roughly ₹3.05 lakh crore.

Put simply, if companies can raise capital at attractive valuations, taking on more debt may not be the first choice anymore. Don’t they have to dilute their shareholding to raise equity? Yes, they do. But if a company can command steep valuations and raise money, the level of dilution is considerably reduced. The money is raised and the balance sheet continues to look debt free.

So where is the funding shifting now?

Let’s take NBFCs, one of the largest issuers in the bond market. They are now leaning more toward banks for borrowing.

Source: RBI

As shown in the table below, bank lending to NBFCs in FY26 exceeded bond issuances, making banks the largest incremental source of funding, and pushing bonds into second place.

The Reversal - Bank Lending vs Bond Issuance to NBFCs

| Funding Source | H1 FY26 (₹ Lakh Crore) | H2 FY26 (₹ Lakh Crore) | Full Year FY26 (₹ Lakh Crore) | Change H2 vs H1 |

|---|---|---|---|---|

| Bond Issuances | 2.1 | 1.4 | 3.5 | -33% |

| Bank Lending (Net Increase) | -0.20 | 2.50+ | 4.3 | +1350% |

Source: RBI Sectoral Bank Credit Data

Wait, shouldn't higher bond yields also mean higher bank rates? Then why are NBFCs shifting to banks?

Not always. Bank lending rates are linked to the repo rate, which the RBI cut from 6.50% at the start of 2025 to 5.25% by December 2025. Naturally, bond yields should have fallen too, right? Because, RBI rate cuts usually reduce borrowing costs across the economy.

But while 3-month yields dropped from 6.10% to 5.30% because they closely track RBI policy rates; long-term bond yields depend on far more than repo cuts; including inflation expectations, government borrowing, liquidity, global yields, FPI flows, rupee movement, and overall market sentiment.

But, isn’t this a temporary dip?

Maybe. At this point, a reasonable person might say: "Okay, but this is just a rate cycle thing, right? Yields will come down eventually. Equity markets may cool off too. But, there are structural problems in India's bond market that existed before this two-year decline began. Here's the thing. India's corporate bond market stands at roughly 18% of GDP. South Korea is at 54%. Malaysia's at 79%.

See the gap?

Think of it this way. A deep, well-functioning bond market should be able to absorb a rate cycle without losing issuers to banks.

So, what's the real problem here?

Too short, too fast?

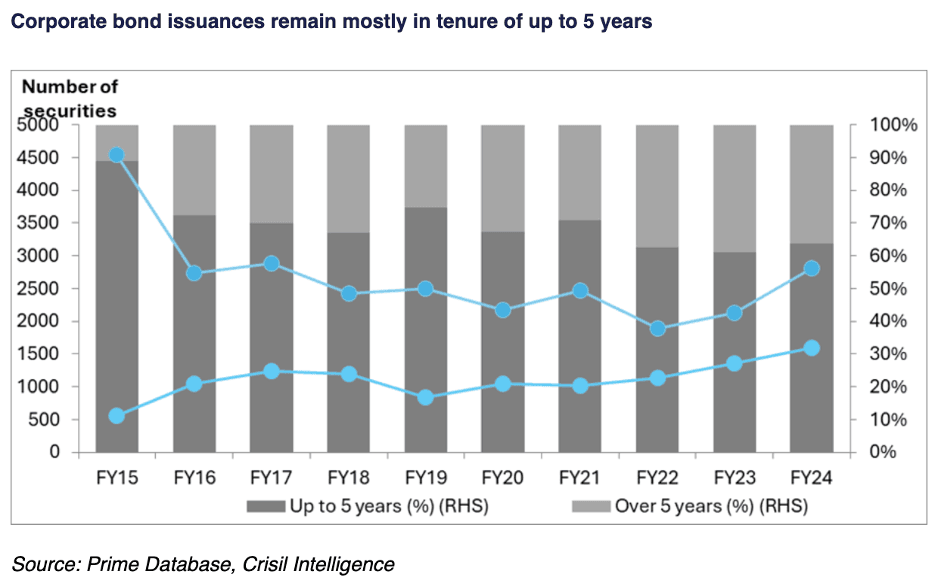

Most corporate bonds in India mature within 3 to 5 years. That's fine if you're refinancing debt or managing working capital. But what if you're building a solar power plant? Or a highway? Or an affordable housing project?

Those generate revenue slowly, over 15 or 20 years. They need patient, long-term capital. As seen below, India’s bond market continues to be dominated by short-term securities. This effectively makes the debt market an ineffective way to raise money for long term requirements.

The narrow borrower base

India’s corporate bond market works for a very small club.

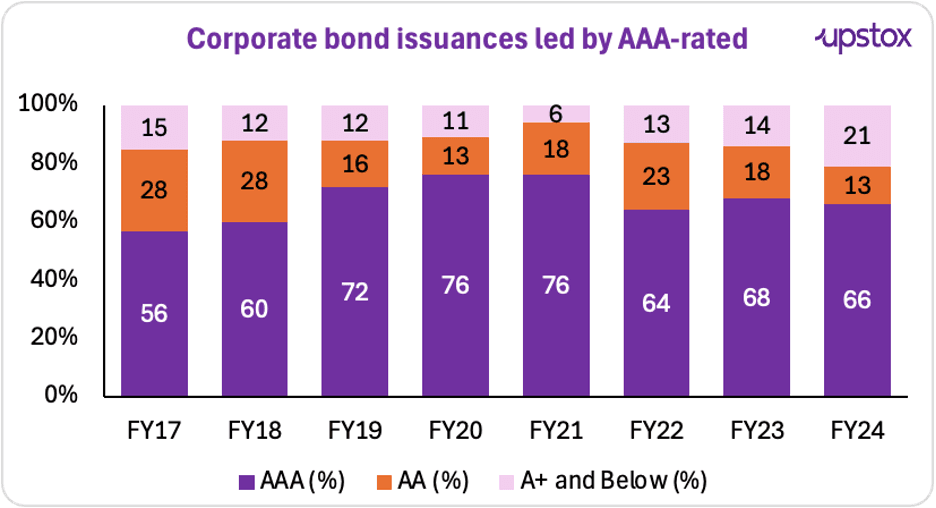

Nearly 97% of issuances come from top-rated borrowers like AAA, AA+ and AA companies. Drop below that, and raising money gets much harder.

Which means the market mostly serves large PSUs and big NBFCs. Mid-sized companies? Smaller firms? MSMEs? Effectively locked out.

Source: CRISIL

Now, what needs to change?

An IMC Chamber of Commerce report released in May 2026 estimates that India's corporate bond market could grow from roughly 18% of GDP today to around 35% by 2030.

Ambitious? Sure. But not impossible, if the market evolves in the right direction, as per the report.

Remember the three-to-five-year concentration we talked about earlier? That's the problem. The IMC report pegs 8.5 years as a realistic target for the average tenor. And honestly? That shift alone would open up an entirely new category of capital demand, patient capital for long-gestation projects that can't be funded any other way.

Then, right now, the market only works for the safest, most creditworthy names. This is why ideas like a ₹25,000–50,000 crore credit guarantee facility are gaining traction. Essentially, a government-backed mechanism that helps mid-rated borrowers, the ones with decent but not perfect credit, become "bondable."

But getting there isn't automatic. It requires deliberate structural changes, not just waiting for yields to come down.

Whether that happens or not? That's the question worth watching over the next few years.

About The Author

Next Story