Upstox Originals

Is India’s steel furnace heating up again?

7 min read | Updated on June 25, 2026, 17:38 IST

SUMMARY

Steel rarely gets attention as a market signal, but right now, it may be pointing to something bigger. Across the industry, companies are stepping up investments. This isn’t just about steel production. It reflects expectations around infrastructure, manufacturing, and a potential broader pickup in economic activity.

Stock list

The country’s five largest steelmakers are expected to spend at least ₹75,000 crore in FY27 alone. | Image: Shutterstock

Steel is usually seen as an old-economy business, blast furnaces, construction rods, railway tracks and factory sheds. But right now, it may be one of the clearest signals of where India’s economy is headed.

Across the industry, steelmakers are stepping up capital expenditure to prepare for a larger domestic market. India’s steel capacity is already around 220 million tonnes in FY26, with a target of 300 million tonnes by 2030.

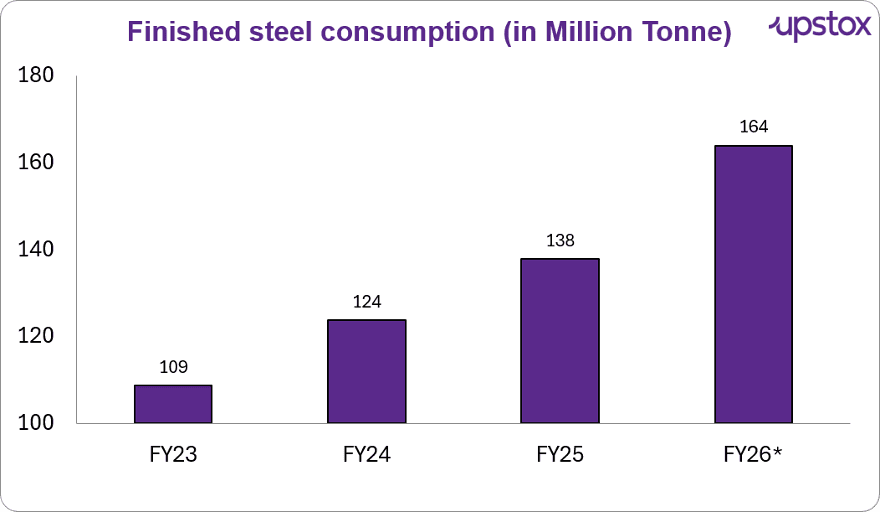

But capacity is only one side of the story. The demand side is moving too: finished steel consumption has risen by about 50% since FY23, giving companies more confidence to build ahead.

Source: Ministry of Steel / PIB. Note: FY26 figure is provisional; values rounded.

The country’s five largest steelmakers are expected to spend at least ₹75,000 crore in FY27 alone, compared with the ₹55,000–60,000 crore per year capex run-rate Crisil had earlier projected for the top five players. In steel, that kind of jump matters: companies only spend this much when they believe demand will last longer than one cycle.

That makes the current capex push more than a company-level expansion story. It is a bet on India’s next phase of growth, and like all big industrial bets, the timing matters as much as the ambition.

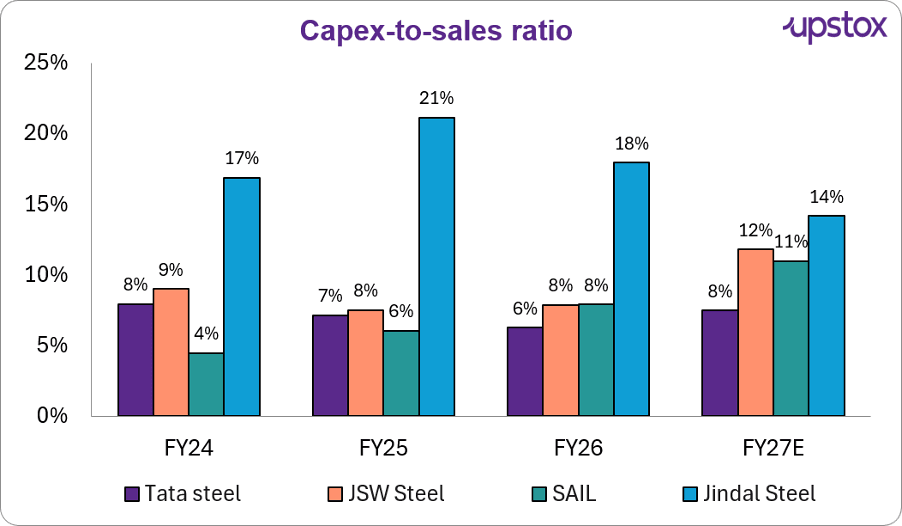

Why this capex matters financially

Source: Company earning calls, brokerage reports, and Screener.in, Note: Capex-to-sales is calculated as capex divided by sales/revenue. Values rounded.

Capex intensity is not rising evenly, and that is the point. JSW Steel and SAIL look set for a step-up, while Jindal Steel is easing from a heavy investment phase.

But across the board, spending remains meaningful. Steelmakers are not just maintaining plants, they are still putting serious money behind the next demand cycle.

Where the money is going?

The capex push is now showing up across India’s biggest steelmakers. The pattern is clear: add capacity, upgrade plants and move towards higher-value products.

| Company | Capex / expansion plan |

|---|---|

| JSW Steel | Guided for around ₹15,000–16,000 crore capex in FY26, long-term target of 50 MTPA India capacity by FY31 |

| Tata Steel | Around ₹27,000 crore Kalinganagar expansion, raising capacity from 3 MT to 8 MT |

| SAIL | Plans to raise capacity from about 20 MTPA to 35 MTPA by 2030, with projected outlay of nearly ₹1 lakh crore |

| AM/NS India | Expanding capacity and downstream presence, including large investments in Hazira and value-added steel |

| Jindal Steel | Investing in capacity expansion and value-added products across steel and downstream operations |

Source: Company filings, Reuters, Economic Times, PIB/Ministry of Steel.

What stands out is that this is not only a race to make more commodity steel. JSW’s plans point to scale, Tata Steel’s Kalinganagar expansion shows a deeper India focus, and SAIL’s proposed expansion links public-sector steel capex to infrastructure and industrial policy.

AM/NS India and Jindal Steel add another layer, private steelmakers are also preparing for stronger demand in flat steel, downstream products and specialised steel. In simple terms, the industry is preparing for two Indias at once: one that still needs roads, bridges and homes, and another that wants autos, appliances, renewables and advanced manufacturing.

Are balance sheets supportive?

That raises the next question: can balance sheets carry this spending? In steel, capex only works if companies can fund expansion without letting debt run ahead of earnings. That is why the leverage picture matters as much as the demand story.

Source: S&P Global Ratings. Note: FY27 and FY28 are forecasts. Chart represents leading Indian steelmakers accounting for about half of India’s steel output.

The balance-sheet signal is supportive, but it is still a forecast. In the base case, industry debt-to-EBITDA is expected to fall below its 10-year median through FY27–FY28, suggesting steelmakers may have more room to fund expansion than in previous upcycles.

The stress case is the reminder. If earnings weaken, leverage moves back closer to the long-term average, which means the capex story still depends on prices, demand and project execution staying supportive.

Major players involved

Steel capex does not affect steelmakers alone. Large producers such as JSW Steel, Tata Steel, SAIL, Jindal Steel and AM/NS India are directly involved in the expansion cycle, but the spending also flows into connected sectors such as mining, capital goods, EPC, railways, ports, logistics, power and finance. A steel plant needs more than furnaces, it also needs raw materials, equipment, freight movement, energy and funding.

Key risks

The risk is that steel remains capital-heavy and cyclical. Higher domestic capacity can help India meet more of its own steel demand, especially if companies add value-added and specialised grades. But imports will not disappear as a risk, cheaper overseas steel can still pressure domestic prices when global supply is weak.

Raw material costs can squeeze margins, and large projects can face delays or debt stress. So the real test is not whether India will need more steel, but whether companies can expand without losing control over costs, debt and margins.

Top 5 steel companies by market capitalisation

| Company | Market cap (₹ Cr) | P/E | ROE | 3Yr stock return % | 3Yr profit growth % |

|---|---|---|---|---|---|

| JSW Steel | 3,16,980 | 35 | 10 | 19 | 34 |

| Tata Steel | 2,46,425 | 22 | 12 | 20 | 10 |

| Jindal Steel | 1,17,019 | 29 | 8 | 28 | 1 |

| S A I L | 75,423 | 20 | 6 | 29 | 25 |

| Jindal Stainless | 57,796 | 18 | 18 | 29 | 15 |

Source: Screener.in; Data as of 15 June 2026

Why steelmakers are spending now

The demand drivers for steel are not new :- roads, housing, factories and infrastructure have always needed it. What is new is the visibility of that demand. These drivers are now showing up together in stronger consumption numbers, giving steelmakers more confidence to spend ahead of the cycle.

For years, India’s growth push has leaned heavily on government capex, while private-sector investment has been more cautious. Steel may be one of the clearer pockets where that caution is easing, though it is too early to call this a broad private capex revival.

In a long-cycle industry, that matters. Steel capacity takes years to build and thousands of crores to execute, so companies cannot wait for demand to fully arrive before investing. The current capex push is therefore not just about one strong year, it is a bet that India’s demand base is becoming durable enough to justify fresh capacity.

Before you go

Steelmakers are not just betting on higher steel demand, they are betting that India’s growth cycle is durable enough to justify fresh capacity. That makes this capex push one of the clearer signals of confidence in the physical economy. But in steel, ambition only works if companies can protect margins, manage debt and execute projects on time.

About The Author

Next Story