Upstox Originals

Is India being underplayed by global markets?

5 min read | Updated on June 23, 2026, 15:45 IST

SUMMARY

India has quietly slipped in some of the world’s most important market benchmarks. And when that happens, money moves. Much of this shift has to do with where the world is investing right now, particularly AI and semiconductors. But markets are rarely linear. In India, valuations have cooled, and expectations have reset, raising the question - is India once again becoming an interesting opportunity?

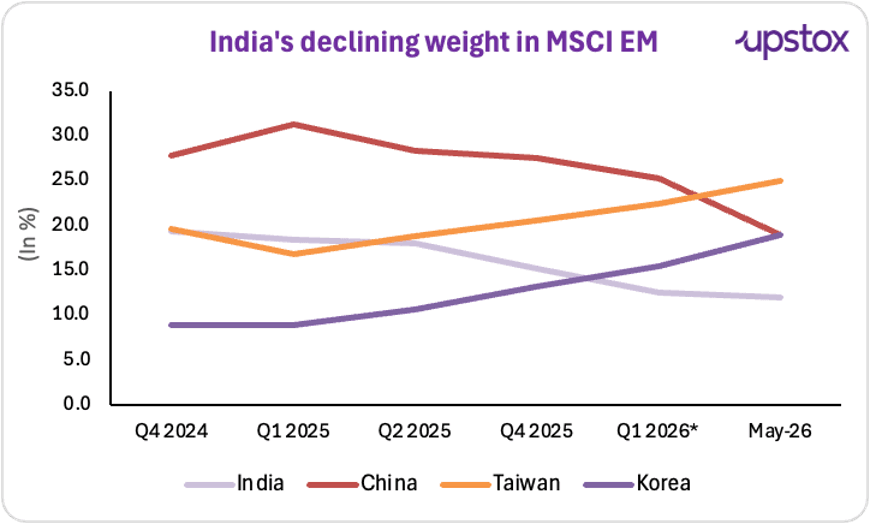

India’s weight in the MSCI EM Index has fallen from ~18% to ~11% now. | Image: Shutterstock

Imagine pouring money into what everyone called the “brightest star” in emerging markets, only to watch its influence in the global benchmark quietly erode. In mid-2024, India’s weight in the MSCI Emerging Markets (EM) Index hovered around a heady 20-21%. By mid-2026, it had fallen to roughly 11%, placing it behind Taiwan (~26%), China (~20%), and South Korea (~23%).

Source: MSCI

But that said, what if the most compelling opportunity in emerging markets is not where capital is flowing today—but where it quietly moved away from?

What is the MSCI index and why does it matter?

The MSCI Emerging Markets Index is where global money decides how much to invest in countries like India. Roughly $750 billion is invested in funds that automatically track this index—they don’t make active choices, they just follow it. On top of that, many larger investors use the same index as a reference when deciding where to put their money.

Here’s the key part: when India’s weight in the index changes, money moves automatically. A 1% shift can push a few billion dollars in or out of Indian stocks—not based on sentiment, but because funds have to follow the index.

And when that happens, markets can move fast.

Why did India hold so much weight before?

In October 2020, India's MSCI EM weight was a modest 8.1%, just 87 Indian stocks were included in the index. Then two things happened simultaneously. In April 2020, the government relaxed FPI investment limits, raising the ceiling from a fixed 24% threshold to the full sectoral FDI cap. For many large Indian companies, this effectively doubled or tripled the amount of foreign capital that could theoretically flow in. MSCI noticed. It began raising India's inclusion factors, and more Indian stocks started qualifying for the index.

At the same time, Indian equities simply started outperforming. By November 2021, India's weight had jumped to 12.3% with 106 stocks, a 420 basis-point rise in barely 13 months. By May 2024, 136 Indian stocks were in the index and the weight had climbed to approximately 18%.

Why is this falling now?

The catalyst for the current rebalancing of the EM index is the scale of AI-driven demand for semiconductors.

Taiwan's semiconductor industry alone now accounts for 14.4% of the MSCI EM Index on its own, contributing to IT's surge to nearly 37% of EM, up from 31.8% just one month earlier.

Leading the charge has been Taiwan Semiconductor Manufacturing Co. TSMC's shares have more than doubled in the past year. It makes up more than 40% of Taiwan's benchmark Taiex index. And at 14.21% of the MSCI EM index, TSMC on its own now carries a larger weight than the entire Indian equity market.

A single Taiwanese chipmaker outweighs a $5 trillion economy's entire listed market in the world's most tracked emerging markets index.

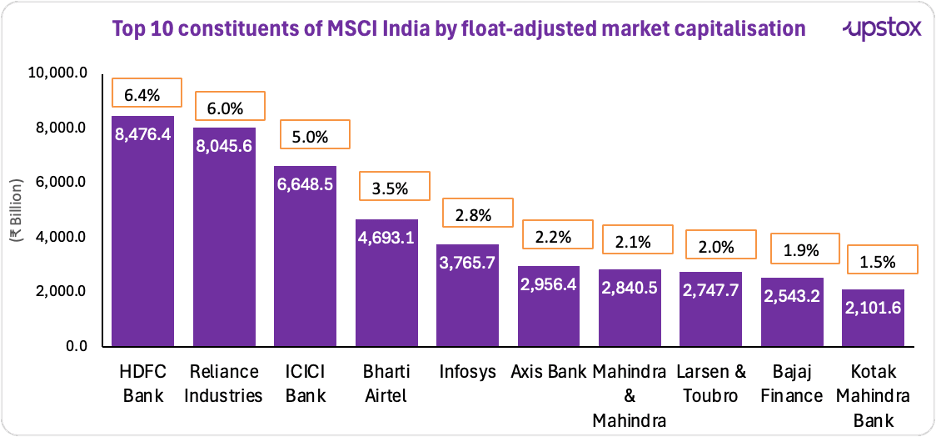

India's highest-profile representatives in the MSCI EM top-10, HDFC Bank and Reliance Industries, each carry a weight of approximately 0.8%. TSMC alone is 17.75x the size of India's largest single MSCI constituent.

What is India missing?

India lost weight because it lacked direct AI hardware exposure. India's index is heavily concentrated in BFSI and other domestic sectors, with minimal exposure to the global AI hardware supply chain.

Source: MSCI; Note: Percentages displayed above the bars represent each company's weight in the MSCI India Index.

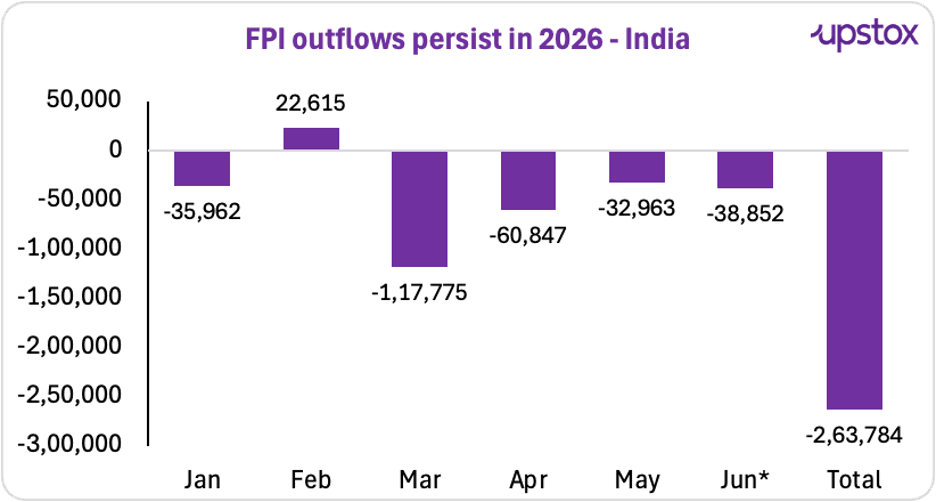

This sector composition has had real consequences. As passive funds adjusted to India's lower MSCI weight and active investors rotated toward AI-linked markets, foreign investors pulled nearly ₹2.6 lakh crore from Indian equities in 2026

Source: NSDL, as on Jun 4, 2026

So does this mean Indian markets are undervalued?

Not quite. But they are certainly less expensive than they were a year ago. As of early June 2026, the Nifty 50 was trading at a P/E of 19.96, near the lower end of its historical fair-value range of 19–22 and well below the 22-plus multiples seen in 2024. The correction reflects a combination of foreign selling, benchmark-driven outflows and a global rotation of capital toward AI-linked markets. While this doesn't automatically make India undervalued, it has certainly made valuations more reasonable than they were at the peak of the India trade.

Where does India go from here?

India's MSCI story isn't over, it's just entered a more demanding chapter. This phase may also be a good moment for investors to pause and rethink what’s really changed. Has India genuinely become less relevant, or has the market’s attention simply shifted elsewhere for now?

Markets often swing too far in one direction before correcting themselves. If those global flows start to turn—whether because valuations look better, earnings improve, or investors grow uncomfortable with too much concentration in a few markets—India could quietly come back into focus. Not as the obvious trade everyone rushes into, but as one that people begin to look at more carefully again.

About The Author

Next Story