Upstox Originals

Why was June 2026 Microsoft's worst month since the dot-com crash?

7 min read | Updated on July 08, 2026, 18:09 IST

SUMMARY

Microsoft's stock plunged nearly 19% in June, its worst month since the dot-com crash. Strange, because the company's core business is still delivering strong growth. Is this about soaring AI costs, an increasingly complicated OpenAI partnership, slowing businesses elsewhere, or simply a market that's demanding more from Big Tech? Let's unpack what really went wrong, and whether the sell-off has gone too far.

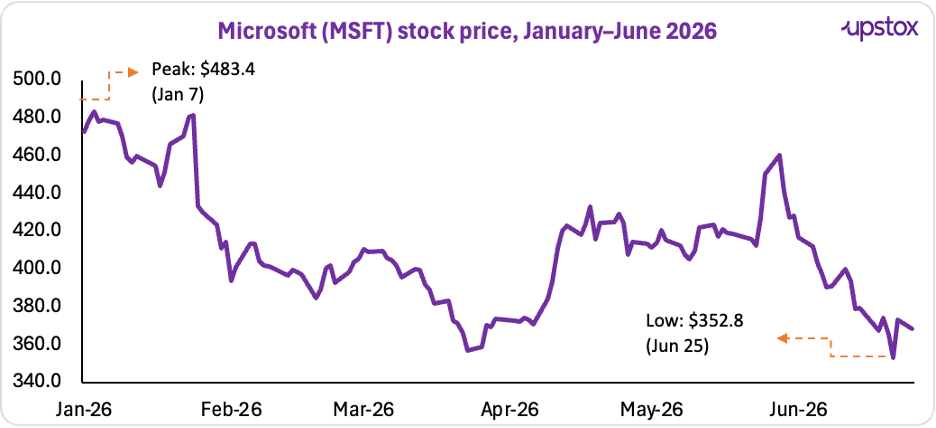

Microsoft has corrected 19% in June 2026. | Image: Shutterstock

The company that many investors have long viewed as Big Tech's safest heavyweight erased nearly $650 billion in market value in just one month.

In June 2026, Microsoft's shares plunged nearly 19%, marking their worst monthly performance since December 2000, when the dot-com bubble was unravelling. What made the sell-off even more surprising was that it came in the middle of a blockbuster year for Microsoft's AI business.

But the correction also did something investors hadn't seen in years: it made Microsoft look meaningfully cheaper. The stock briefly traded at ~19x forward earnings, below the S&P 500's ~20x forward multiple and well below Microsoft's own 10-year average of 27x.

While the stock has since recovered modestly to around 20x forward earnings in July, it still trades at a notable discount to its historical valuation.

Source: Investing.com; *Data as of June 30, 2026

Why is this happening now?

The partnership that's starting to cost Microsoft

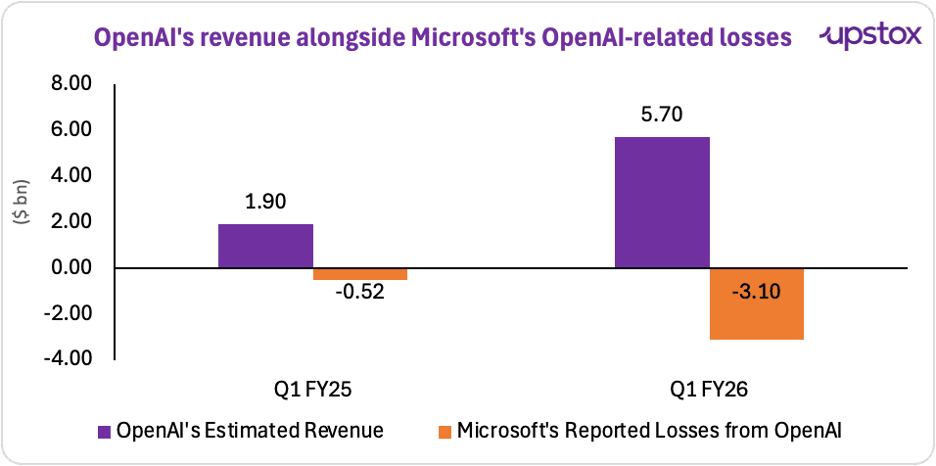

One thing was making investors uncomfortable. Microsoft's relationship with OpenAI. Microsoft owns a 27% stake in OpenAI worth roughly $135 billion, holds royalty-free rights to its technology, and the two are tied together through a partnership that runs until 2032.

Then came reports that OpenAI could push its IPO to 2027. Now, companies don't usually delay IPOs unless they want stronger financials, a better valuation, or more favourable market conditions. Naturally, investors began wondering if Microsoft's AI investment would take longer to pay off.

The numbers are beginning to tell that story.

Source: Company fillings, Fortune Note: Q1 2025 revenue (~$1.9B) is a derived estimate, calculated by working backward from OpenAI's disclosed Q1 2026 revenue of $5.7 billion, which multiple sources reported as a "year-over-year tripling." OpenAI has not separately disclosed Q1 2025 revenue.

The AI bill is getting bigger

Microsoft spent $38 billion on capital expenditure (think: datacenters, chips, servers, the physical stuff AI runs on) in just the last quarter. Bank of America now expects the full-year 2026 number to approach $190 billion, which is more than 60% higher than last year.

While all this spending was happening, free cash flow, the actual cash Microsoft has left over once the bills are paid, fell about 10%. That's less money for buybacks, less for dividends, less for shareholders.

So now, of course, the question is whether it's growing fast enough to justify a number that large.

But wait a minute. Aren't Meta, Google and Amazon spending billions on AI too? So why is Microsoft taking all the heat?

That's a fair question. After all, Meta expects 2026 capex of $125–145 billion, while Alphabet is guiding for roughly $175–190 billion.

The difference isn't the size of the cheque, it's the expected return on that cheque. For decades, Microsoft perfected the software model: build once, sell infinitely, and enjoy high gross margins. But generative AI changes that equation. Every Copilot prompt incurs an inference cost, requiring GPUs, data centres and power. As AI usage grows, so do depreciation costs and pressure on margins.

Now, investors look at Meta or Google differently because their primary monetisation engine is advertising. If the AI hype cycle slows down, Meta can throttle back its cluster expansion, and its underlying business is selling ads across Instagram and Facebook, giving them more flexibility if demand slows. Microsoft, however, is investing heavily in long-life AI infrastructure, from data centres to Nvidia Blackwell GPUs and long-term power agreements. Those investments are difficult to scale back once committed.

A $627 billion cushion, or is it?

Microsoft currently has a contracted backlog (expected revenue from future contracts) of $627 billion, almost double what it was a year ago.

A large part (~$250 billion) is in areas and technology providers. As a result, investors are beginning to question how dependable that future revenue will be if OpenAI continues to diversify its cloud spending.

Game over for XBox?

While everyone's watching the AI story, Microsoft's gaming business has slowly been weakening. Xbox hardware revenue fell 33% year-over-year. Overall gaming revenue dropped 7% for the quarter, and over the first nine months of the year, it came in at $16.8 billion, down $1.1 billion, or 6%, from a year before.

Microsoft has announced roughly 1,000 layoffs across Xbox Game Studios, marketing, and hardware engineering. And console prices went up again, by $100 to $150, the second hike in under a year, largely because memory and storage costs have gotten so expensive. (Apple, coincidentally, raised its own hardware prices the very same day.)

What happened the last time Microsoft had a month like this?

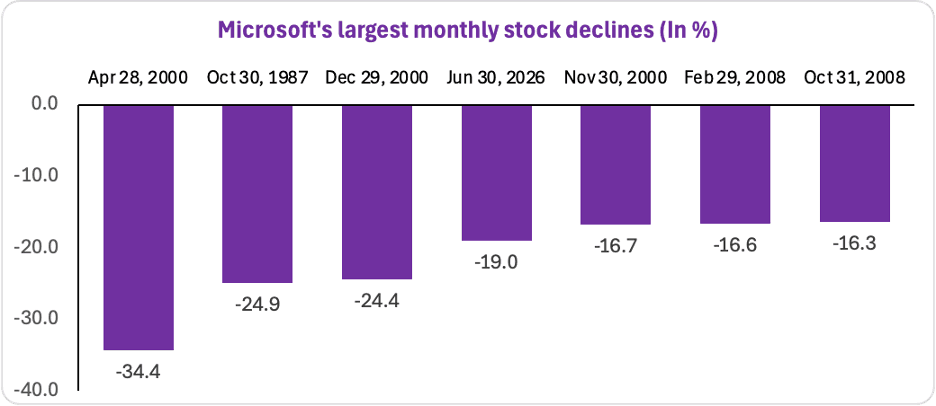

Back in the late 1990s, Microsoft was one of Wall Street's biggest stars.

The internet was taking off, investors couldn't get enough of technology stocks, and Microsoft's shares climbed to a split-adjusted high of $119.94 in 1999. When the dot-com bubble burst, reality caught up with exuberance. By the end of 2000, Microsoft's stock had tumbled to $40.25, a 66% decline from its peak.

And the sell-off didn't happen overnight.

The stock first fell 16.7% in November 2000 (from a month-end closing price of $34.44 to $28.69) before plunging another 24.4% in December, making it the company's worst monthly decline on record. That's precisely why Microsoft's ~19% decline in June 2026 is being described as its worst month since December 2000.

The chart below shows just how rare such declines have been. Apart from the dot-com bust, Microsoft has only witnessed monthly losses of this magnitude during periods of extraordinary market stress, such as the 1987 Black Monday crash and the 2008 Global Financial Crisis.

Source: The Wall Street Journal

Should it worry you now?

Its noteworthy for sure.

Microsoft's AI bill is enormous and free cash flow has slipped. But that's partly because AI infrastructure has become unusually expensive, with high-bandwidth memory (HBM) and advanced chips still in short supply.

As supply catches up over the next few years, those costs could possibly ease. More importantly, Microsoft isn't building AI infrastructure without a plan. It owns one of the world's largest software ecosystems, from Azure and Microsoft 365 to Copilot, GitHub, and Dynamics, giving it multiple ways to monetise every dollar it spends.

So, has Microsoft become a value opportunity, or a value illusion?

It depends on which side of the story you focus on.

On one hand, Microsoft continues to deliver. Revenue reached $241 billion and net profit stood at $98 billion over the first nine months of FY26. Azure is still growing at around 40%, while its AI business has reached a $37 billion annual revenue run rate.

On the other hand, investors are asking a different question: Will Microsoft's massive AI spending generate enough returns to justify the cost? With capex approaching $190 billion, margins under pressure, and OpenAI-related losses rising, the market is demanding proof that today's spending will translate into tomorrow's profits.

Until then, Microsoft's stock will likely be driven less by its earnings and more by confidence in the ROI of its AI investments.

About The Author

Next Story