Upstox Originals

Why do medical devices cost so much in India?

5 min read | Updated on June 10, 2026, 15:50 IST

SUMMARY

A device that costs ₹15,000 can end up priced at ₹1.5 lakh—and sometimes even higher. In India, medical device prices often rise 5–25x between factory and hospital, driven by imports, distribution layers, and rising input costs. In a market where patients have little time or power to compare prices, the real question isn’t just how prices rise—but where that gap comes from.

In certain cases, the markups on medical devices in India are up to 25x. | Image: Shutterstock

Imagine paying ₹1 lakh for a medical device, and later discovering the device itself cost a fraction of that.

Not hypothetical. Indian regulators have flagged this repeatedly: devices reaching patients at prices several times their import or factory cost. In some cases, markups of up to 25x.

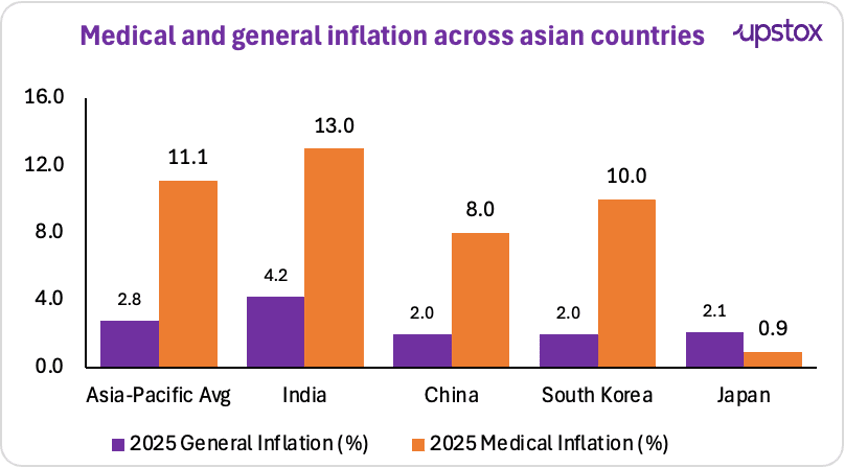

The backdrop makes it worse. Medical inflation in India is running at ~13% annually, among the highest in Asia, well above the Asia-Pacific average of 11.1%.

And in a country where most healthcare spending still comes out of patients' pockets, that gap isn't just a pricing anomaly. It's the difference between a manageable bill and a financial crisis.

So the question is worth asking: why do medical devices cost so much by the time they reach a hospital bill, and where does all that markup actually come from?

Source: Aon

How high are the mark-ups, really?

According to the Association of Indian Medical Device Industry (AiMeD), the pricing gap is visible across categories. In ophthalmology, intraocular lenses that cost ₹200–₹7,000 to produce can be billed at ₹300–₹45,000. In cardiovascular care, cardiac catheters, pacemakers, and heart valves show even wider spreads, with landed costs often rising several-fold by the time they reach hospitals.

| Device | Base / Landed Cost | Typical Hospital Price |

|---|---|---|

| Syringe | ₹3–₹12 | ₹30 |

| Three-way stopcock | ₹5–₹16 | ₹95–₹136 |

| Cardiac catheter | ₹1,500–₹2,000 | ₹7,000–₹11,000 |

| Pacemaker | ₹15,000–₹60,000 landed | ₹1.5–₹2 lakh |

| Intraocular lens | ₹200–₹7,000 | ₹300–₹45,000 |

| Surgical heart valve | ₹80,000–₹1.5 lakh landed | ₹4–₹9 lakh |

| Transcatheter heart valve | ₹5.5–₹6.5 lakh landed | ₹18–₹24 lakh |

Source: News articles

But why are prices so high to begin with?

India imports 70-80% of its medical devices, and that import dependence runs deep. Which means many devices already arrive in India with a hefty landed cost attached to them.

But that's not where the pricing journey ends.

Once inside the country, the device often passes through a chain of sub-stockists, regional distributors, and hospital procurement departments, with each layer typically taking a 10–20% cut before it finally reaches the patient.

Now layer a geopolitical shock on top of all this.

The conflict in West Asia has quietly rattled India's medical supply chain. India imports a significant share of the polypropylene and PVC used in syringes, IV bags, and catheters from Saudi Arabia and the UAE, sourcing over ₹3,000 crore worth of propylene polymers from the two countries in 2024 alone. As supplies tightened, raw material costs for consumables jumped 40–50%, while packaging costs rose 15–25%.

Overall, Indian medical device makers are facing cost increases of 10–50% across segments, and those higher costs eventually find their way into hospital bills.

A quick glance at polypropylene prices:

Source: Trading Economics

Fair question.

After all, markups exist in every industry.

But medical devices operate in a market that's fundamentally different from most consumer markets. Demand is often non-discretionary, purchases are time-sensitive, and patients rarely have the ability to compare prices or defer consumption. In economic terms, the end consumer has very little pricing power.

The concern becomes even more significant when you look at India's insurance landscape.

India's flagship public health scheme, Ayushman Bharat PM-JAY, covers hospitalisation costs of up to ₹5 lakh per family per year for around 55 crore beneficiaries, roughly the bottom 40% of the population by income. It still leaves a vast middle out: salaried workers in the informal sector, self-employed professionals. Private health insurance penetration remains low.

Has the government tried to step in before?

In 2017, the NPPA capped prices on cardiac stents. Overnight, prices fell from as high as ₹2 lakh per unit to around ₹39,000. Knee implant caps followed shortly after, cutting costs by up to 60–70% and making joint replacements accessible to millions of patients who had previously been priced out.

But those interventions were narrow. As of today, only four device categories have formal price caps under the Drug Prices Control Order. For everything else, the NPPA can only monitor MRPs and flag increases exceeding 10% annually. In a market with thousands of product categories and mark-ups running into multiples of cost, that is a very narrow net.

So, what's being proposed now?

The medical devices industry wants to cap trade margins rather than fix prices. The proposed limits vary by product value, 75% for low-cost consumables like syringes, 66% for mid-range devices such as catheters, and 50% for high-value implants like pacemakers and heart valves. It has also suggested capping hospital billing margins at 50% above procurement cost.

The idea is simple: instead of controlling the final price of a device, regulators would limit how much each participant in the supply chain can mark it up.

What happens next?

The medical devices industry sits at the intersection of two competing priorities: affordability and sustainability.

Patients need access to reasonably priced healthcare. At the same time, manufacturers, distributors, and hospitals need viable economics to keep the system functioning. The question, therefore, isn't whether margins should exist. It's whether the current balance is the right one.

As India's medical devices market expands, policymakers will continue searching for ways to improve transparency and affordability without undermining innovation or investment. How they strike that balance could shape the future of healthcare costs for millions of Indians.

About The Author

Next Story