Upstox Originals

The terminal value trap: Valuing Indian IT in the age of AI

6 min read | Updated on June 08, 2026, 13:19 IST

SUMMARY

The recent sharp correction in IT stocks could be a reaction to something deeper than just near-term growth. Most of a stock’s value comes from what we assume happens far into the future. But what if that future is changing faster than ever? As AI reshapes how IT companies operate, even steady businesses face uncertain long-term outcomes. Should your DCF model also mirror that uncertainty? What if the number you trust most in valuation is the one you understand the least?

IT company valuations face novel challenges due to AI. | Image: Shutterstock

In 2007, Nokia was the most dominant handset maker on the planet. It had loyal customers, formidable scale, and profits that analysts could map out with confidence. Any diligent investor running a Discounted Cash Flow (DCF) model that year would have arrived at a reassuring number. Six years later, Nokia sold its handset business to Microsoft for a fraction of what those models implied.

Imagine building a beautiful skyscraper where 75% of the weight rests entirely on the foundation, only to discover the soil underneath is slowly shifting. This is exactly the dilemma you face today when valuing Indian IT majors.

So, here is a question for all you DCF fans: with the Indian IT business model fundamentally changing, what should be the perpetual growth rate or the terminal value you would assume?

For those who are unaware, the perpetual growth rate is the rate at which something keeps growing forever at a steady pace. It assumes the growth will continue at the same rate year after year, indefinitely.

Why does this matter?

Anywhere between 60-80% of any company’s value lies in the terminal value. If you get this wrong, then effectively your entire valuation model is wrong!

The stock market has begun to feel the tremors. The Nifty IT index hit a 52-week high in February 2026, before plunging in recent weeks. The sell-off was not triggered by a bad set of quarterly numbers. It was triggered by a growing fear that the earnings model itself is changing.

Evolving business model

For decades, the Indian IT business model worked on one straightforward principle: labour arbitrage. Hire and train engineers and bill global clients by the hour. More headcount would therefore equal higher revenue. Because this model was so linear, investors could easily map out the next 5 (even 10) years of free cash flows, add a stable perpetual growth rate, and calculate an intrinsic value.

But AI has fundamentally disrupted this linear equation, introducing uncertainty that can leave investors’ spreadsheets vulnerable.

The central challenge for tech companies is no longer the volume of work—enterprises are demanding more automation, cloud integration, and AI pipelines than ever before.

The real issue is pricing power.

Analysts are calling this "AI Deflation." When an AI tool allows a junior engineer to complete a coding task in 30 minutes instead of two days, global clients naturally expect those productivity gains to be passed back to them.

Consequently, contract renewal prices are facing immense pressure. The industry is rapidly transitioning from a labour-based billing system to an outcome-based or "digital labour" model.

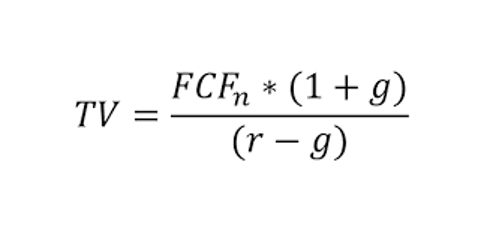

The DCF crisis: What happens to perpetuity?

This brings us to the core of the DCF problem. In a typical DCF model, the vast majority of a company's calculated worth does not actually come from the explicit forecast period. It is stored in the terminal value (TV) — the mathematical estimate of what the business is worth in eternity.

The formula is deceptively simple.

Source: Investopedia

A perpetual growth rate. A stable discount rate. A steady state.

It works beautifully — if the future resembles the past. In a stable industry, analysts routinely set the terminal growth rate at a comfortable 4% to 5% to match long-term economic growth.

However, the traditional assumptions baked into terminal value begin to look fragile:

-

Stable growth? Growth may persist, but its drivers are changing.

-

Pricing power? Already under pressure from AI-led efficiency gains.

-

Linear scaling? Revenue is no longer tied neatly to headcount.

The challenge, then, is not mathematical — it is conceptual and philosophical. If AI does compress traditional revenue lines, can we confidently assume any legacy IT firm will grow at 5% forever?

More existentially: will the traditional service architecture even exist in 20 years? To illustrate how sensitive a stock's value is to the terminal phase, consider this conceptual breakdown of a typical IT company's valuation structure:

| Valuation component | Contribution to share price (%) | Core underlying assumption |

|---|---|---|

| Years 1 to 5 | ~10% to 15% | Digital engineering pipelines and current deal books |

| Years 6 to 10 | ~15% to 20% | Successful transition to AI operating models |

| Terminal value (Year 11+) | ~65% to 75% | Perpetual survival and stable, inflation-linked growth |

If 70% of an IT stock's value is derived from assumptions about the year 2036 and beyond, a minor miscalculation in your terminal assumptions can break your entire valuation model.

Rethinking the spreadsheet

How should an investor approach a DCF model today without making dangerous assumptions? Tweaking the growth number would be the most logical answer. But since we don't know what kind of growth rate to assume, here are potential suggestions:

-

Adjust the discount rate: We know that the business model is fundamentally undergoing a change. Given that the long-term survival of a business is hazy, the risk premium must rise. Applying a higher discount rate could help price in the risk.

-

Build scenario ranges: Instead of relying on a single smooth projection, it may help to think in terms of possibilities, like: 1) AI expands demand faster than it erodes pricing; 2) Efficiency gains are entirely passed through to clients

-

Margin of safety: Follow the wisdom of Benjamin Graham. After you are done valuing a stock, add another layer of safety. Buy a company only if it is available at a considerable discount to its “fair value.”

Final thoughts

The goal here isn't to write off the Indian IT sector. These companies possess massive balance sheets, deeply entrenched client relationships, and some of the world's finest engineering talent. They are actively retraining their workforces to capture high-value AI consulting revenue.

A DCF model will still give you a number. It always does. The idea is to find a more honest way to think about valuation. In a world shaped by AI, where growth, pricing, and even the nature of work are evolving, that number may say less about the company and more about the assumptions you chose to make.

The real skill, perhaps, lies not in calculating terminal value — but in questioning whether “terminal” still means what we think it does.

About The Author

Next Story