Upstox Originals

Indian banks face a stiff fight against rising frauds

5 min read | Updated on July 06, 2026, 15:29 IST

SUMMARY

Banking frauds cost Indian banks ₹48,021 crore in FY26, up 46% YoY, underscoring the growing challenge facing the financial sector. As payment scams become more sophisticated and large-value frauds continue to surface, regulators and banks are stepping up their use of technology to detect suspicious activity and prevent losses. But can better technology solve a problem that keeps evolving?

The RBI noted that India records just 1 fraudulent transaction for every 1,01,242 digital transactions. | Image: Shutterstock

Every few months, India celebrates another milestone in digital payments. Record transactions. Record volumes.

But alongside that growth comes a challenge that's getting harder to ignore. Banking frauds in India are rising, fast. In 2025, nearly 2.5 million people lost roughly $2.5 billion to banking fraud. That's a 4,300% increase since 2021.

To be fair, India's payment infrastructure is holding up remarkably well. The RBI noted at the Shield 2026 Conclave that the country records just one fraudulent transaction for every 1,01,242 digital transactions, with losses amounting to only ₹1.40 for every ₹1 lakh transferred.

But here's the concern. As digital payments surge, so does the scale of the problem. Fraudsters are getting smarter, more organised, and harder to detect. And the sheer volume of transactions means that even a tiny fraction of fraud adds up to billions of rupees in losses every year.

What do the numbers say?

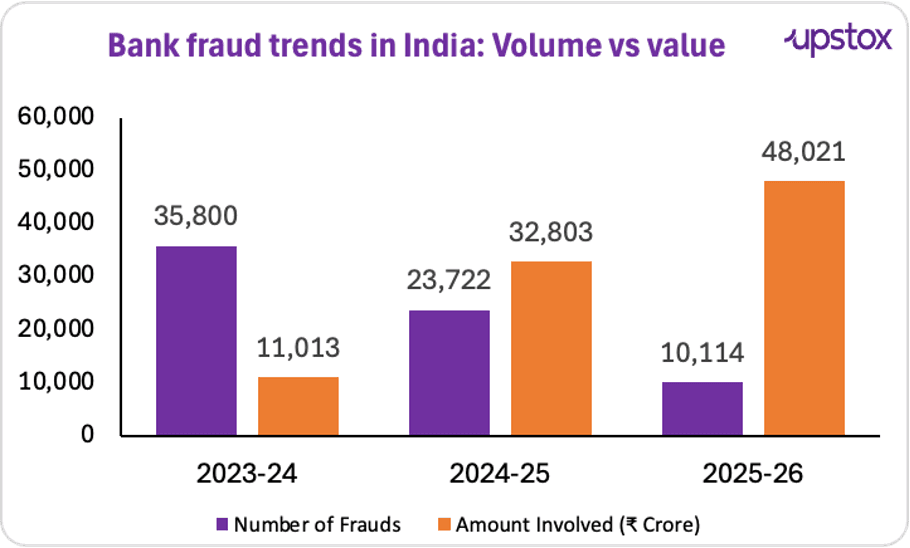

According to the RBI's latest annual report, the total value of banking frauds jumped 46% year-on-year to ₹48,021 crore in FY26, up from ₹32,803 crore in FY25.

Source: RBI

Public sector banks reported 5,418 fraud cases in FY26, involving ₹35,709 crore. That's 74.5% of all banking fraud value in the country, from institutions that account for just over half of all reported cases.

Private banks tell a different story. More cases, 3,956 of them, but smaller in value. ₹11,399 crore in total, or about 23.7% of the fraud amount.

And others; foreign banks, small finance banks, and payments banks barely register. 740 cases, ₹913 crore, less than 2% of the total.

So what's actually driving the surge?

In FY26, loan and advances frauds accounted for ₹40,774 crore, nearly 85% of the total fraud value reported by banks. The data suggests that India's biggest banking challenge is large-value corporate and lending frauds.

| Area of Operation | 2024-25 Number of Frauds | 2024-25 Amount Involved (₹ Cr) | 2025-26 Number of Frauds | 2025-26 Amount Involved (₹ Cr) |

|---|---|---|---|---|

| Advances | 7,924 | 30,367 | 8,640 | 40,774 |

| Off-balance Sheet | 8 | 270 | 8 | 521 |

| Forex Transactions | 23 | 16 | 23 | 125 |

| Card/Internet/Digital Payments | 13,332 | 517 | 293 | 29 |

| Deposits | 1,207 | 521 | 407 | 377 |

| Inter-Branch Accounts | 14 | 26 | 57 | 72 |

| Cash | 306 | 39 | 181 | 35 |

| Cheques/DDs, etc. | 122 | 74 | 84 | 14 |

| Clearing Accounts | 6 | 2 | 3 | 11 |

| Others | 780 | 971 | 418 | 6,063 |

| Total | 23,722 | 32,803 | 10,114 | 48,021 |

Source: RBI

One case study that explains the problem

ABG Shipyard offers a glimpse into the sheer scale that banking frauds can reach. The case, which surfaced in 2022, remains India's largest reported bank fraud by value. ABG Shipyard Ltd., once one of the country's leading private shipbuilders, allegedly defrauded a consortium of 28 banks led by ICICI Bank.

According to investigators, funds borrowed from banks were diverted through a complex network of transactions and used for purposes other than those for which the loans had been sanctioned. The total exposure across lenders stood at ₹22,842 crore. ICICI Bank had the largest exposure at ₹7,089 crore, followed by IDBI Bank at ₹3,634 crore and State Bank of India at ₹2,925 crore.

Can AI help?

The RBI certainly believes so. Over the past year, the regulator has launched a series of initiatives aimed at detecting fraud before money disappears.

-

MuleHunter.AI: One of the most prominent initiatives is MuleHunter.AI. As of December 2025, 23 banks had implemented the RBI-backed system. The platform uses artificial intelligence to identify mule accounts, bank accounts opened or operated to move illicit funds on behalf of fraudsters. According to information obtained through RTI requests, one participating bank reported detection accuracy of nearly 95%. The system is capable of identifying and blocking around 20,000 suspected mule accounts every month.

-

FREE-AI Framework: In August 2025, the RBI released its Framework for Responsible and Ethical Enablement of Artificial Intelligence (FREE-AI). The framework sets guardrails for how banks can deploy AI systems. Importantly, it requires AI-driven fraud detection decisions to be explainable and auditable, ensuring that banks can justify automated decisions to regulators.

-

IDPIC: India's Fraud Intelligence Hub: Perhaps the most significant development came in October 2025 with the creation of the Indian Digital Payment Intelligence Corporation (IDPIC). It has been established as a national fraud intelligence network for digital payments. Its objective is ambitious: detect fraud in real time, share intelligence across banks, and use AI, machine learning and big-data analytics to identify emerging fraud patterns.

Looking ahead

The RBI is already considering a range of safeguards, including a one-hour cooling-off period for certain account-to-account transfers, additional authentication through a trusted person for vulnerable groups such as senior citizens, tighter scrutiny of large credits entering customer accounts, stronger monitoring of mule accounts, and greater customer control over digital payment limits and settings.

While public attention remains focused on phishing links, fake QR codes and OTP scams, the RBI's numbers suggest that the bulk of banking losses continue to come from a handful of high-value frauds. The fight against fraud, therefore, may not be won solely on smartphones, but also through stronger risk controls, better credit monitoring and AI-powered surveillance across the banking system.

About The Author

Next Story