Upstox Originals

Housing slowdown: Minor leak or foundation issues?

.png)

5 min read | Updated on October 17, 2024, 11:51 IST

SUMMARY

India's housing market saw a decline in Q3 2024, with both sales and new property launches dropping compared to the previous year. Factors such as rising home prices, increased mortgage rates, and oversupply in key markets contributed to this shift. While some cities like Delhi-NCR performed better, most experienced reduced demand and slower sales.

Home launches and sales in major cities have seen a decline in Q3CY24

India's housing market experienced a notable slowdown in the third quarter of 2024, with a 5% decline in sales and a sharp 25% drop in new property launches across major cities. This shift follows a period of rapid growth and is influenced by factors such as rising property prices and decreased affordability. Although some markets like Delhi-NCR bucked the trend, most cities saw reduced demand as potential buyers adjusted to the new market realities.

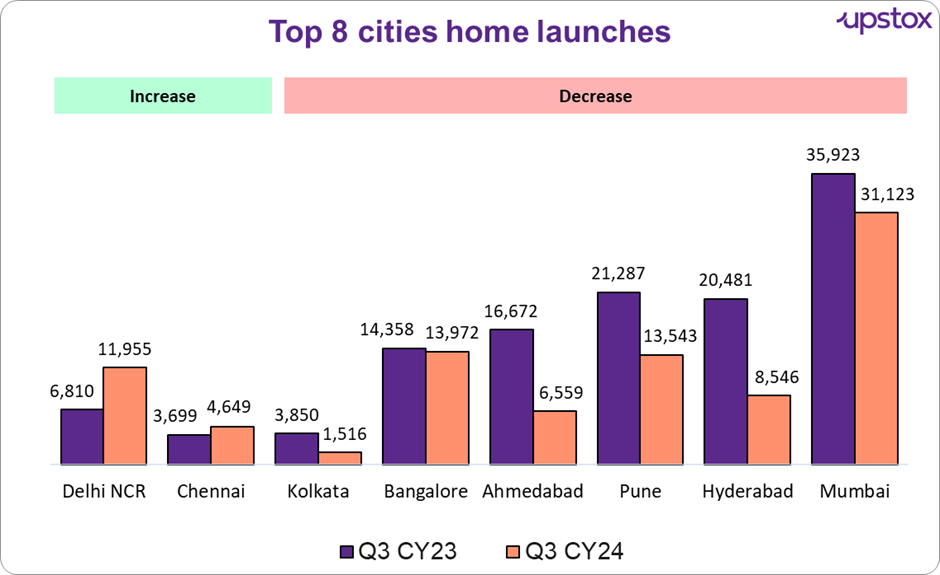

Home launches

In Q3 CY24, the launch of new residential units in the top 8 markets dropped by 25%, going from 1,23,080 units in Q3 CY23 to 91,863 units. Only Delhi NCR and Chennai saw increases in new launches, with 76% and 26% rises, respectively.

Meanwhile, cities like Mumbai, Pune, Kolkata, Hyderabad, Bangalore, and Ahmedabad experienced significant declines ranging from 3% in Bangalore to a huge 61% in Ahmedabad and Hyderabad.

Source: Real Insight Residential – July-September 2024, Housing Research

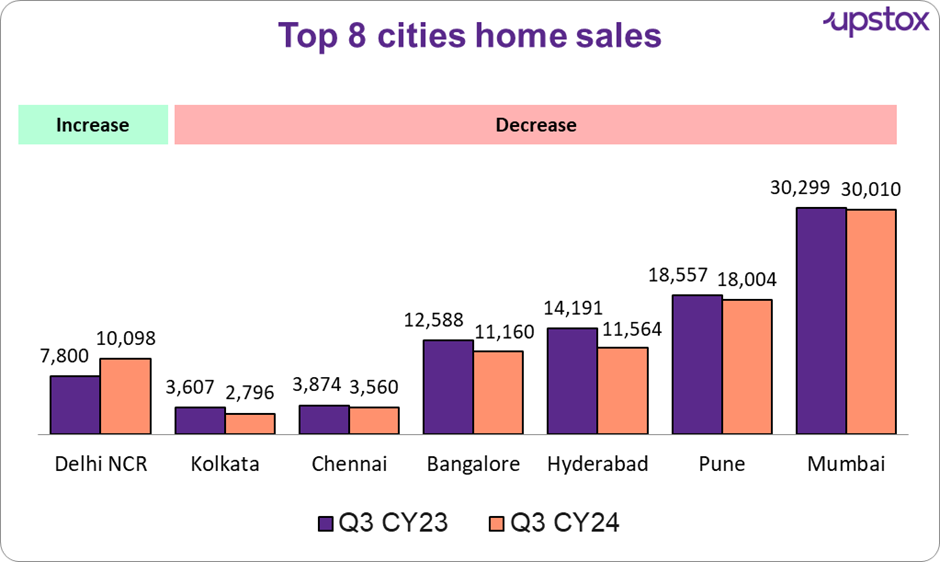

Home sales

Sales in Q3 CY24 showed a dip with 96,544 units sold, down 5% from the 1,01,221 units sold in the same period last year. Among the top cities, only Delhi NCR experienced a significant sales boost, rising 29% year-over-year. Meanwhile, other major cities like Mumbai, Hyderabad, Bangalore, Ahmedabad, Chennai, Kolkata, and Pune saw declines of 1% in Mumbai to a strong 22% in Kolkata.

Source: Real Insight Residential – July-September 2024, Housing Research

Reasons behind the fall in house prices:

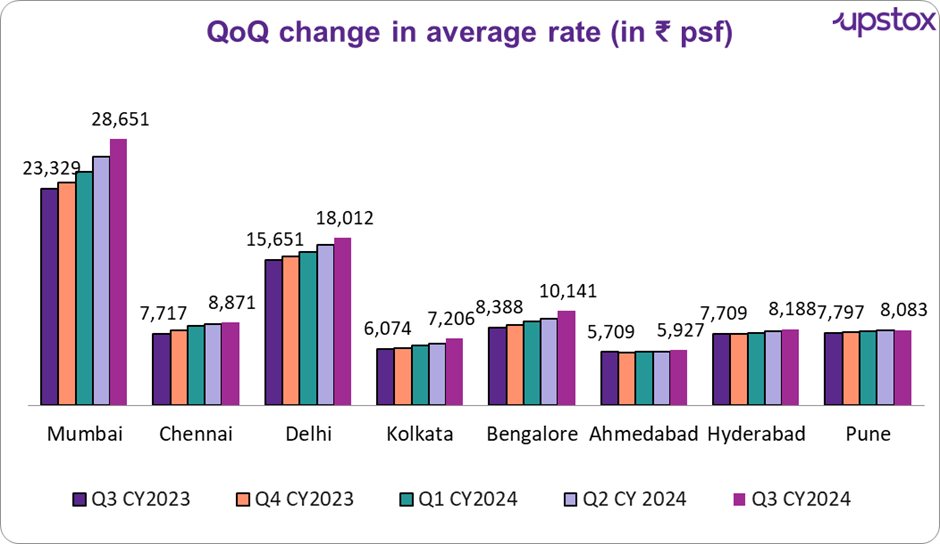

Rising home prices

A significant increase in property prices (up to 20% in some cities) has made homes less affordable. As can be seen below over the past year, the average rate of a house per sq ft has risen, with Mumbai seeing the highest jump at 22%, while Pune and Ahmedabad had the lowest increases at 4%. As more individuals continue to migrate to these major cities from other parts of India, the cost of owning a house is likely to increase further.

Source: Magibricks research

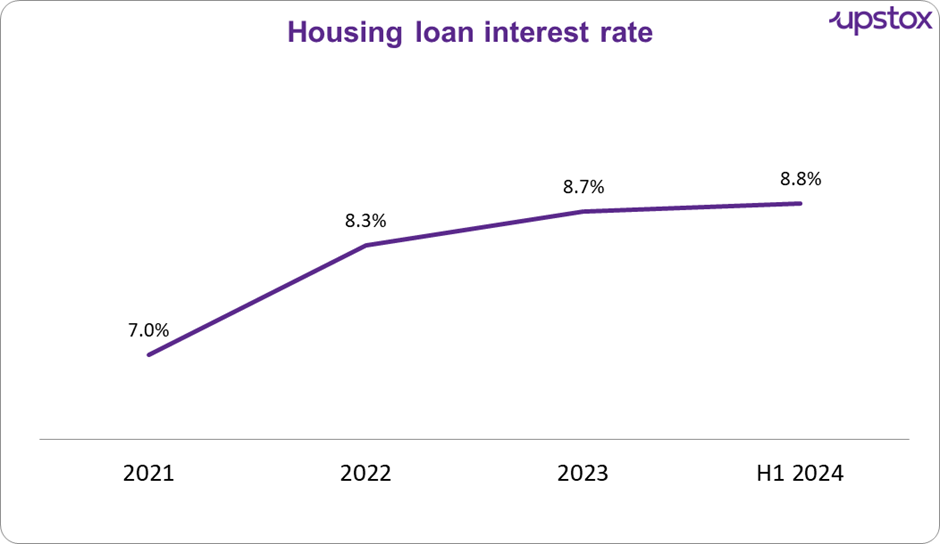

Higher mortgage rates

Elevated interest rates have deterred potential homebuyers from making new purchases, as can be seen in the below chart, loan interest rates have been steadily climbing over the past few years.

Source: Knight Frank Research

Oversupply in certain markets

Excessive new launches in recent years have resulted in a glut of unsold inventory, In particular, cities like Hyderabad and Ahmedabad have experienced a substantial increase in unsold units as per the table below, also notice how long the inventory is taking to be sold in these different cities as of the first 6 months of 2024.

| City | Unsold Inventory, H1 2024 | YoY (H1 2024 vs H1 2023) (%) | Quarters to Sell (QTS), H1 2024 |

|---|---|---|---|

| Mumbai | 1,65,121 | 2% | 7.5 |

| NCR | 1,05,185 | 5% | 7.1 |

| Bengaluru | 51,643 | -4% | 3.8 |

| Hyderabad | 49,232 | 27% | 5.8 |

| Pune | 42,736 | -6% | 3.6 |

| Ahmedabad | 30,222 | 18% | 7.7 |

| Kolkata | 23,116 | 15% | 6.2 |

| Chennai | 16,416 | 8% | 4.3 |

Source: Knight Frank Research

Shift in buyer preferences

Consumers are leaning towards premium properties with modern amenities, which has slowed demand for mid-range options. As stated in the Knight Frank report, While the high-end market is booming, the affordable segment has dropped from 29% of total sales in Q3 2023 to 24% now, a 14% decline.

Only Mumbai and Kolkata have seen growth in this segment. Rising prices and limited supply have deterred buyers, especially for units under ₹50 lakhs. Developers are focusing more on the premium segment, with 53% of development interest in Q3 2024. The mid-segment (₹50 lakh to ₹1 crore) is also slowing down, with a 13% drop in sales year-over-year.

What does this mean for an investor?

Post COVID, the Indian housing market saw a boom. That said, increasing interest rates and consistently rising prices have dampened spirits. Experts expect pricing to stabilize, now that the COVID rebound is long done and markets should reach some balance.

Besides this, easing interest rates and government measures to boost housing could potentially support this sector. Investors should monitor changes in mortgage rates and policy announcements, as these could influence both demand and pricing trends in the coming quarters.

Select stocks in the sector

The table below lists some select Realty companies in India.

| # | Name | Market Cap ₹ Cr. | 3-Year Profit Growth % (2019-2024) | 3-Year Stock Return % (2019-2024) | ROE (%) | Price / Sales | Debt / Equity |

|---|---|---|---|---|---|---|---|

| 1 | DLF | 2,19,016 | 6 | 27 | 7 | 34 | 0.1 |

| 2 | Macrotech Developers | 1,20,952 | 24 | 27 | 11 | 10 | 0.4 |

| 3 | Godrej Property | 89,641 | 58 | 9 | 7 | 32 | 1.1 |

| 4 | Prestige Estates | 80,475 | 3 | 60 | 13 | 10 | 1.2 |

| 5 | Oberoi Realty | 73,386 | 30 | 29 | 13 | 15 | 0.2 |

| 6 | Phoenix Mills | 59,703 | 56 | 51 | 12 | 15 | 0.5 |

| 7 | Brigade Enterprises | 32,330 | 36 | 42 | 12 | 6 | 1.5 |

| 9 | SignatureGlobal | 21,202 | 147 | NA | -7 | 14 | 3.1 |

| 10 | Sobha | 18,410 | 14 | 31 | 2 | 7 | 0.8 |

| Average | 79,457 | 42 | 35 | 8 | 16 | 1.0 |

Source: Screener.in; * Data as on 16th October 2024

About The Author

Next Story