Upstox Originals

Dark stores are pricing the neighborhood kirana store out of its own street

7 min read | Updated on April 28, 2026, 19:54 IST

SUMMARY

When you hear of lower commercial vacancy rates in the news, you would assume it's a positive sign. But what if the players competing for that space aren’t on an equal footing? On one side are PE-funded quick-commerce companies; on the other side, your local kirana shop. As dark stores scale, rents are rising, and prime spaces are getting locked in. So is this just a convenience upgrade, or a deeper shift in how our cities work?

India’s quick commerce market is projected to grow at a ~46% CAGR between 2025 and 2028. | Image: Shutterstock

Struggles for the local kirana stores continue to persist. Just when business had adapted and stabilised post the surge in quick commerce, they have a new challenge coming.

Supply is becoming expensive. Rents across markets are rising and hurting margins. The question is - how long can the local stores persist?

Here is what is happening

Somewhere between your third Blinkit order this week and the fourth, quick commerce became part of your routine.

Point is - they dont need to be fancy or even in prime locations, just large enough to ensure that they can fulfill orders.

India had around 2,500 dark stores in 2025. By 2030, that number is expected to rise to ~7,500; a threefold increase in just five years.

This expansion is no longer limited to metros. Nearly one-third of these stores are already in Tier 2 cities and towns, signalling that quick commerce is moving deeper into the country’s consumption patterns.

As Tier 1 markets begin to tighten, the next phase of growth is clearly shifting outward. ANAROCK estimates that total dark store area in Tier 2 and Tier 3 cities had already reached 4–5 million sq. ft. by the end of 2025, with cities like Lucknow, Jaipur, Chandigarh, and Kochi among the fastest-growing markets.

Scale and network build-out across players

| Company | Particulars |

|---|---|

| Blinkit | 1,816 stores (Sep 2025); 3,000 stores by Mar 2027 |

| Zepto | Expanding network - 100+ new stores through 2026 |

| JioMart | 600 quick-commerce stores; 3,000+ total; 5,000 PIN codes Ongoing expansion in high-volume catchments |

| Swiggy | ~5 million sq. ft. network (Nov 2025); ~6.7 million sq. ft. by Dec 2028 |

| Flipkart (Minutes) | 500+ stores; 30+ cities (Dec 2025); 1,000+ stores; 60+ cities by Mar–Apr 2026 |

| Amazon (Now) | Launched 2024; expanded to Bengaluru, Delhi, Mumbai, Gurugram (2025); Scaling at ~2 centres per day |

Source: India Logistics Market Outlook 2026, CBRE

Expansion sounds great, until you ask: who’s actually paying for that 10-minute delivery?

Dark stores are expanding, deliveries are faster, and everything you need is just 10 minutes away. The total footprint of dark stores is projected to scale from ~13 million sq. ft. to ~38 million sq. ft., as expansion moves beyond the top eight cities into Tier I and II markets, and eventually Tier III cities.

But, here’s the part we don’t see as easily.

This expansion isn’t just about convenience. It’s changing how cities price space, and in the process, who gets to stay in business.

The real estate reset

As quick commerce companies race to deliver faster, they’re all chasing the same thing, space close to where people live. And there aren’t enough of them. So naturally, prices are going up.

Vacancy in these micro-markets is down to just 3–5%. Which means every suitable space now sees multiple takers.

But demand isn’t just about opening more stores. It’s also about stocking more. As platforms move beyond groceries into electronics and premium categories, they need bigger spaces. According to ANAROCK, demand for 3,000–5,000 sq. ft. dark stores is growing at 20–25% annually.

And that’s pushing rents even higher.

Rents have risen 15–20% over the past year, with landlords in NCR and Bengaluru quoting ₹100–180 per sq ft per month, while Chennai, Hyderabad and Pune are seeing ₹70–110 levels.

And while quick commerce players can afford to pay these prices, local stores simply can’t.

For landlords, the choice becomes obvious.

Because suitable spaces are limited, quick commerce players often pay a premium to secure them; often 30–40% higher than what traditional stores can afford.

Lower margins

The structural disadvantage for local stores is difficult to overcome. Operating margins typically range between 7% and 15%, leaving limited room to absorb rising rents or invest in delivery infrastructure. In contrast, quick commerce platforms benefit from optimised inventory, higher throughput per location, and private labels generating 25–35% margins, compared to 8–15% for branded goods.

While property owners are clear beneficiaries of this shift, the impact on traditional retail is significantly more adverse.

A JP Morgan study of 50 offline grocery stores in Mumbai found that 60% reported a decline in sales volumes, with most attributing it directly to competition from quick commerce platforms.

What can we expect ahead from dark stores?

The aggressive rollout of dark stores is rooted in a sharp demand shift. If the current pace of expansion feels significant, it is likely to continue, and so is the pressure on local stores competing for the same neighbourhood space.

India’s quick commerce market is projected to grow at a ~46% CAGR between 2025 and 2028, with Gross Order Value expanding from ₹0.6 trillion to ₹2 trillion.

As demand rises, so does the need for more physical space to support it. Each dark store typically stocks around 2,000–4,000 products, focusing on high-frequency, fast-moving essentials tailored to local demand.

To handle this scale, companies operate on a hub-and-spoke model, a system designed to keep deliveries fast without letting costs spiral.

Think of it as a layered network:

| Stage | Regional Hub (Master Inventory) | Urban Distribution Centre (Cross-docking) | Hyperlocal Dark Store / Micro-fulfilment Centre |

|---|---|---|---|

| Location | City outskirts | Within city boundaries | Radius of 2–3 km (residential suburbs) |

| Size | 50k–500k sq. ft. | 10k–50k sq. ft. | 3k–8k sq. ft. |

Source: News articles

As demand grows, this network has to expand alongside it.

More orders mean more dark stores closer to customers, more distribution points within cities, and larger hubs to support them.

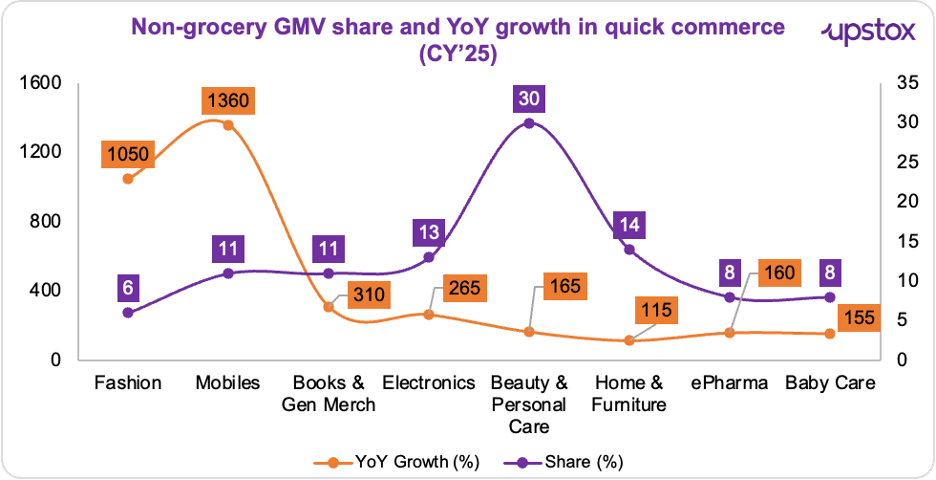

The expansion is not just volume-led, it is also being driven by a shift in what consumers are buying. Non-grocery categories are growing ~1.6x faster than grocery, indicating that demand is moving beyond essential purchases.

Source: ET Retail

Private labels are likely to play a key role in how dark stores make money. Their share has already grown from 1–2% to 6–8%, with projections of reaching 10–15%, as platforms like Zepto scale labels such as Chyll and Aana!, and Swiggy expands Noice with 200+ products.

At the same time, the mix is shifting. There’s a growing focus on perishables; a category with higher margins (25–45%) and repeat demand, which helps strengthen overall unit economics.

In summary

As the sector evolves, the focus is shifting from expansion to sustainability. Dark stores are expensive to run, especially in high-rent areas, and while large platforms can absorb these costs, local stores often can’t, making it harder for them to compete for the same neighbourhood space.

Going ahead, success will depend less on how many stores companies open, and more on how efficiently each one operates, with order density, cost control, and repeat demand becoming critical.

About The Author

Next Story