Upstox Originals

Decoding the silent surge in India's fixed deposits

5 min read | Updated on June 15, 2026, 14:07 IST

SUMMARY

India’s fixed deposit pile has swelled to its biggest share of bank money in years. But the easy explanation, that nervous savers are fleeing a shaky market, turns out to be the smallest part of the story. Behind the surge sit three quieter forces: vanishing savings-account returns, a banking system in need of deposits and a tax change. Stranger still, what's driving most of this surge isn't ordinary households. Here’s what the numbers actually show.

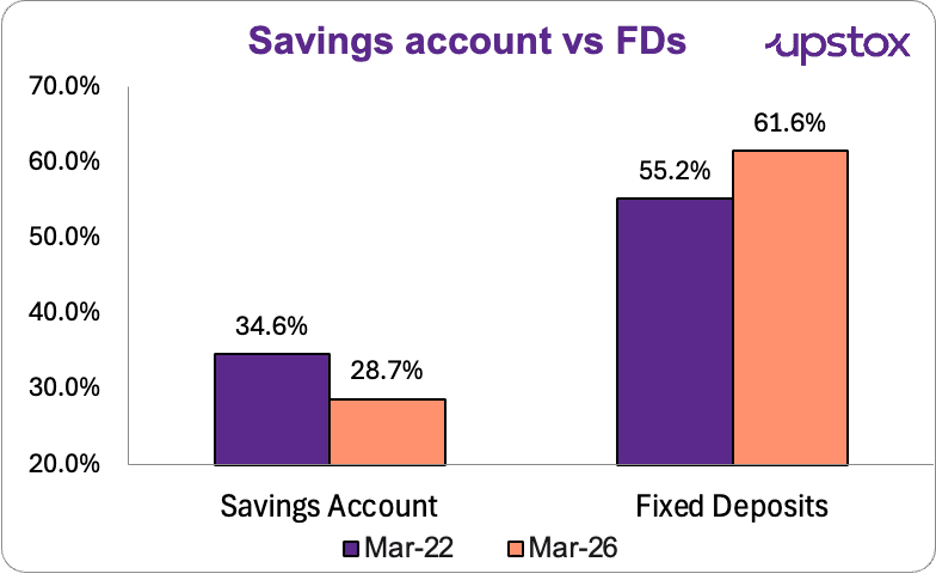

As per the RBI term deposits now make up 61.6% of all bank deposits, up from 55.2% four years ago. | Image: Shutterstock

By the Reserve Bank of India’s latest count, term deposits (FDs) now make up 61.6% of all bank deposits, up from 55.2% four years ago. Over the same period, the share of the humble savings account has shrunk from 34.6% to 28.7%.

Money is unmistakably moving into FDs. The interesting question is why, and the popular answer, that frightened savers are bolting from the markets, turns out to be only part of the story.

Source: RBI, Annual Basic Statistical Return (BSR)-2, March 2026.

The maths nudging your money

Start with the most boring reason, which is also the biggest. As the RBI cut its policy rate throughout 2025, banks trimmed what they pay on savings accounts. SBI now offers just 2.5% on a savings balance, while a 1–3 year FD fetches 6.25%–6.45%. For anyone with cash sitting idle, the decision makes itself: shift it next door to the higher-paying deposit.

Banks need the money

The second force comes from the banks themselves.

From 2024 to 2025, loans grew faster than deposits, leaving lenders short of funds and pushing the system's credit-deposit ratio up to around 80% — its highest in over six decades. In simple words, banks were lending out nearly every rupee they took in as deposits, leaving little spare cash to fund fresh loans.

In 2025-26, bank credit grew roughly 16% against deposit growth of about 13%. To plug the gap, banks competed hard for term deposits — sweetening FD rates and raising well over ₹14 lakh crore through certificates of deposit during the year. When banks are scrambling for funds, fixed deposits get more generous, and savers’ money follows the rate.

A tax change that quietly levelled the field

Here is a nudge few savers clocked. Until 2023, debt mutual funds enjoyed a tax edge over FDs: held long enough, their gains were taxed lightly, with the benefit of indexation.

From April 1, 2023, that advantage vanished — debt-fund gains are now taxed at your income-slab rate, exactly like FD interest. With the tax gap closed, one common reason to prefer a debt fund over a plain deposit went with it. Just how much money this shifted is hard to pin down, but the direction is clear: it made the unglamorous FD look relatively better.

The surge isn’t really in households

Now, let's look at the detail that punctures the ‘nervous small saver’ picture. Within all term deposits, those of ₹1 crore and above make up 46.3% of the pile — and the ₹5-crore-plus bracket alone accounts for 34.8%. The FD boom, in other words, is driven largely by companies and wealthy individuals parking large sums rather than by ordinary families seeking shelter.

Term deposits by size (March 2026)

| Term deposits by size (March 2026) | Share of all term deposits |

|---|---|

| ₹5 crore and above | 34.8% |

| ₹1 crore to under ₹5 crore | 11.5% |

| Below ₹1 crore | 53.7% |

| Total | 100.0% |

Source: RBI BSR-2, March 2026

Are people scared?

Markets have been volatile since September 2024. In 2026 alone, the Nifty 50 and Sensex have corrected almost 10%. It would be logical to wonder – are people afraid of something and that is why they are parking more money in FDs?

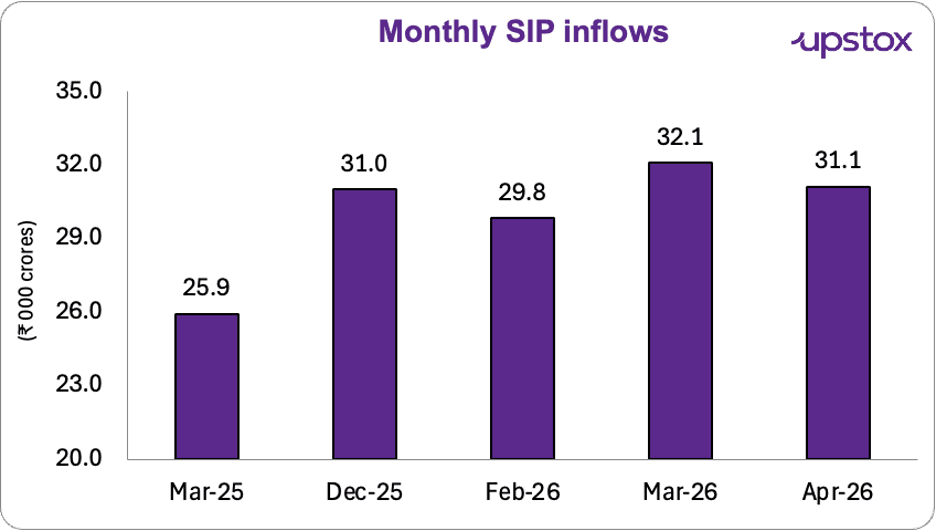

If savers were genuinely frightened, the money flowing into shares should be drying up. It did the opposite. In March 2026, the month the Nifty 50 fell 9.4%, Indians poured a record ₹32,087 crore into equities through SIPs, about 24% more than a year earlier.

Source: Association of Mutual Funds in India (AMFI).

What this means for your own savings

Two quieter signals are worth noting — as context, not advice. First, the high-rate window that made FDs so tempting is already closing.

The share of term deposits earning less than 7% has jumped to 61.8%, from just 27.3% a year ago, as rates turn down.

Savers have been locking in for longer: deposits maturing in 1 to 3 years now make up 69.8% of the total, up from 50.4% in 2022. A great many people have committed money for years — just as interest rates head lower.

| Earlier | March 2026 | |

|---|---|---|

| FDs earning less than 7% | 27.3% | 61.8% |

| FDs maturing in 1–3 years | 50.4% | 69.8% |

Source: RBI BSR-2, March 2026. ‘Earlier’ = a year ago for the rate row; March 2022 for the maturity row.

Closing thoughts

For the ordinary saver, the useful lesson is not to follow the crowd but to understand why deposit rates look attractive right now. Knowing the "why" behind a trend is what lets you judge whether it fits your own goals, rather than simply chasing it.

About The Author

Next Story