Upstox Originals

Why are FIIs leaving Indian markets, and what can bring them back?

5 min read | Updated on April 13, 2026, 17:01 IST

SUMMARY

FIIs have been relentlessly selling Indian equities over the past two years. Their ownership in the Indian markets is down to about 17% (vs 19% in FY23), which is the lowest level in the last 20 years but still significant. Everyone is waiting for them to return, but why are they leaving and what will bring them back?

FII ownership is down to about 17% vs 19% in FY23. What could trigger a comeback?

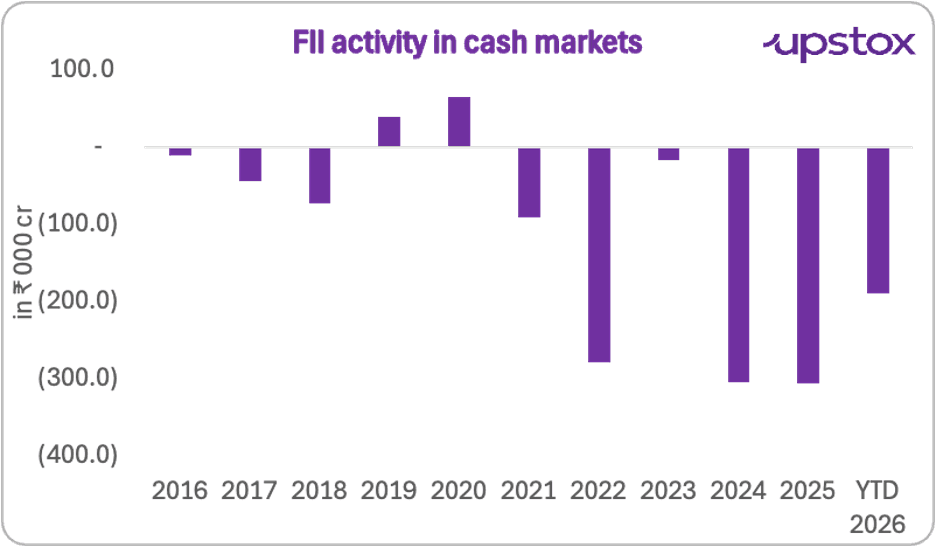

A question often asked in financial news of late is: When will FIIs return? As seen in the chart below, FII selling in the domestic cash markets has not only been relentless, it has made new ‘highs’ each year. Within three months of 2026, the FII sell-off has reached 60% of the levels seen in 2025.

Record FII selling in domestic cash markets

Source: Moneycontrol; Note: YTD 2026 is till April 3, 2026

That said, Indian investors are now wondering what the key factors are that could bring the FIIs back to India. While retail investors only look at the domestic market, for a fund manager abroad, the world is literally the playground. So, the question that must be asked is this: has India delivered robust earnings growth, and is the valuation more lucrative than that of peer countries?

Let’s look at some of these indicators to see where India stands.

Earnings growth - silver linings?

After multiple quarters of below-expected growth, the recent quarter has provided some relief. Backed by a combination of base effects and some fundamental revival, earnings are starting to attract positive attention. That said, the ongoing Middle East crisis could disrupt this momentum.

Source: ICICI Direct Research

Rupee deprecation - hitting a resistance?

For the last couple of years, the Indian rupee has had a rough ride. It has depreciated by ~10% in the past two years and has been one of the weakest-performing currencies. When you look at it from the point of view of a foreign investor, that is nearly 5% wiped out from their annual returns.

Source: Investing.com; *Note: Data is till April 1, 2026

So, is it all bad news? No. The RBI’s recent actions, as highlighted here, seem to indicate that the central bank is ready to defend the INR and contain the volatility and depreciation. To be sure, the INR has historically depreciated between 2-3% annually, and that trend is expected to persist, but that is a known fact and is priced in before taking any decision.

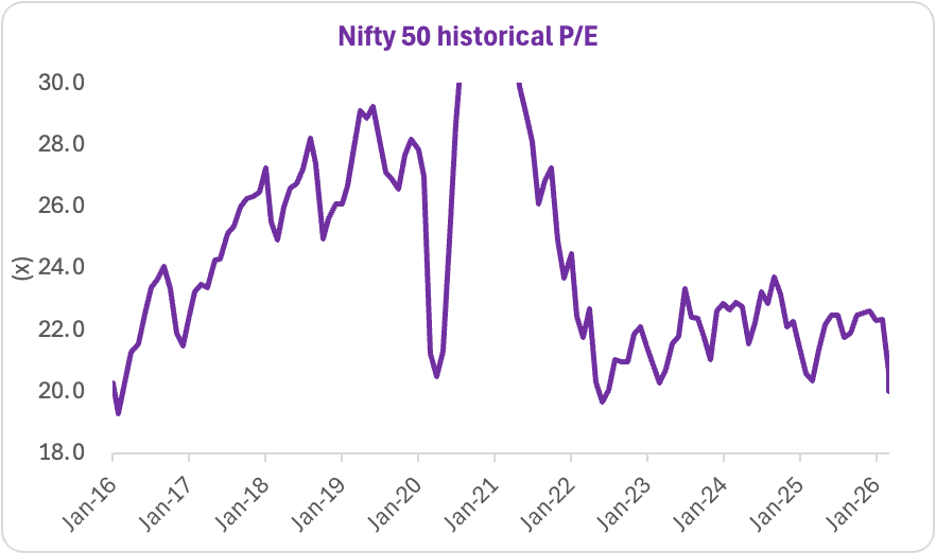

Valuation - cooling off?

The Nifty50’s current valuation at ~20x is near January 2022 levels.

Source: Finlive.in; *Note: Data is till April 2026

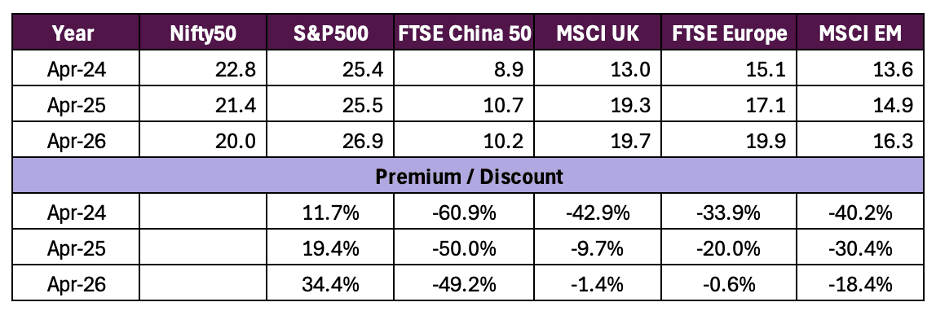

Additionally, India’s valuation differential compared to peers has also been severely reduced. The table below should be read in the following way

-

S&P500: The S&P500 has been trading at a premium valuation versus the Nifty50. Over the past 3 years, this premium has only increased, making the Nifty50 look more attractive than its US counterpart.

-

Other indices: Most other indices were trading at a discount to the INR. Take the MSCI UK for example, in 2024 it was trading at 43% discount to the INR, and is currently trading at an almost similar level.

Improving earnings growth plus supportive valuations should make the Indian equity markets more appealing.

India vs global valuations

Source: Finlive.in, World PE; Data as of 6th April 2026

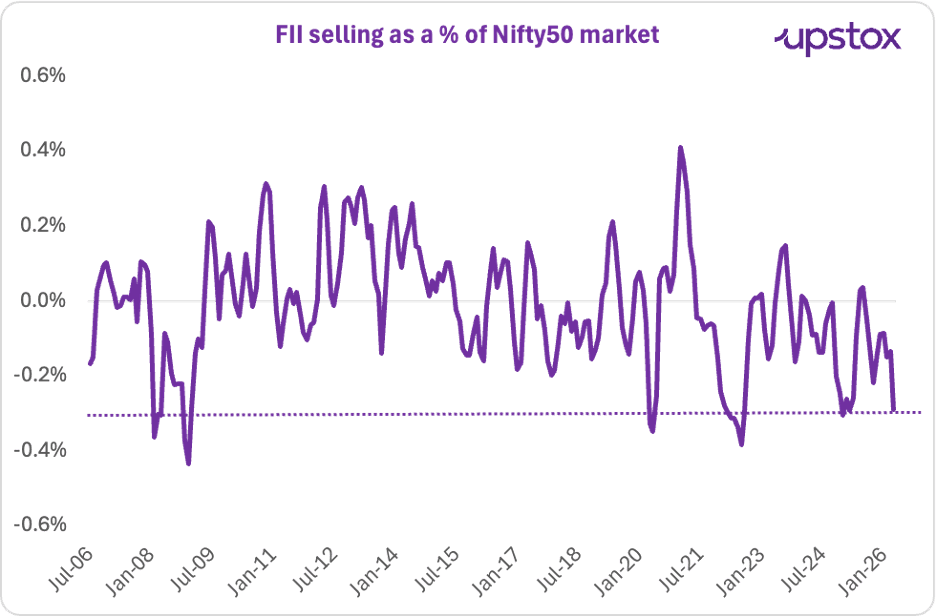

Have they oversold?

The chart below shows the 3-month average FII selling versus the Nifty50 market capitalisation (average of 3-month FII selling / average 3-month Nifty50 market cap). The analysis reveals that FII selling currently is almost near the Global Financial Crisis (GFC) of 2008 and the COVID-19 fall seen in 2020.

At this point, it could be argued that FII selling could possibly be reaching a resistance, and one can expect to see some turnaround here.

Source: Moneycontrol; Note: YTD 2026 is till 03 April 2026

So, they should be coming back anytime now? While there are a lot of positive signs, the FII return story could be impeded by these three facts

-

Global uncertainty: The ongoing West-Asia crisis could be a deterrent. Yes, there is a temporary cease-fire, and India actually has navigated the crisis well (thanks to diversified supply chains), but the uncertainty of this level tends to make investors nervous

-

Elevated oil prices: Oil prices have not only been volatile recently, but are also extremely elevated, adversely impacting India’s current account situation. Simply put, a $100 per barrel oil price does not bode well for India. Reduction, not just stability in oil prices, will be a critical factor that global investors will monitor

-

The AI trade: Last but maybe the most important is the ongoing global AI trade. Basically, AI is the current mega trend that investors are gravitating towards. Whether global AI valuations are fairly pricing growth or are a massive bubble is one of the most highly contested conversations. While India has made some strides, we do not have any strong AI play for investors. Globally, India is therefore viewed as a hedge or an alternative to the global AI trade - meaning if investors want to reduce their exposure to AI, the Indian market is a place they would look. As such, the unwinding of this trade is critical for investors to once again look at India with serious enthusiasm.

To be sure, there are also some structural issues like taxation on equities which have also deterred FII participation in India. However, for the time being there is no easing expected on that front. As such, the points mentioned above are critical to once again bring back foreign flows.

In a nutshell

In the past, we have argued that Indian markets are moving towards an Atmanirbhar stock market. The resilient DII flows have largely proven this theory correct. That said, FIIs still own about 17% of the Indian equity market, making them a crucial participant. Equally important is that steady FII flows can also encourage long-term FDI into a country. Bringing it all together, the stage is set—the fundamentals and valuations both seem favourable—but the external environment needs to be more supportive for the participants to return.

About The Author

Next Story