Upstox Originals

The world is de-dollarising, BRIC by BRIC

.png)

7 min read | Updated on April 25, 2025, 09:47 IST

SUMMARY

Currently, over 80% of global transactions are in the USD. The Trump tariffs have spurred nations to re-evaluate their dollar dependence. This article examines how the BRICS+ nations are reducing their dollar dependence. From payment system diversification and gold accumulation, we anlayse the progress made and the impact of these moves on economies, investors, and the global balance of power.

Currently over 80% of global transactions are in the USD

With US tariffs making headlines, China and Brazil, members of the BRICS group, have announced a shift to trade in their local currencies instead of the US dollar. This decision marks one more step in a slowly rising global trend - as nations aim to reduce dependency on the dollar and strengthen economic ties beyond the USA.

As seen in the chart below, this trend is mirrored in the broader global financial landscape. Over the past eight years, the total amount of FX reserves held in US dollars across all countries has increased. However, its share as a percentage of the overall composition of reserves (which includes currencies beyond the dollar), has significantly declined.

Source: IMF

How does this benefit them? What are the global implications? We will dive into these questions in this article and many other related angles surrounding this pivotal decision.

Before we unpack this, let’s take a quick look at how the dollar became a dominant global force.

The road to global dollarisation

Currently, the Dollar is about 88% of all foreign exchange transactions. The origins of the dollar’s global role can be tracked back to the aftermath of the World Wars. Post which, the USA held ~70% of the world's gold. Besides that, it was one of the only major global economies not directly impacted by the war. Both of which gave the country robust economic and financial strength.

The Bretton Woods Agreement in 1944 further established the dollar’s dominance by pegging most currencies to the U.S. Dollar, which was itself convertible to gold at a fixed rate, effectively making the dollar the world’s reserve currency.

Why is de-dollarisation rising?

The trend for de-dollarisation, while becoming popular recently, is not a new one. Multiple countries in the past have agreed to trade in their own local currencies. India and Russia have explored conducting their oil trade in local currencies since 2014, if not earlier. Today, 90% of that trade in local currency.

In 2015, China launched the Cross-Border Interbank Payment System (CIPS ), to facilitate the clearing and settlement of cross-border transactions in Chinese yuan (RMB). CIPS in a way is a direct competitor to SWIFT (Society for Worldwide Interbank Financial Telecommunication), which facilitates global trade.

While we explore the benefits of de-dollarisation later, on the face of it, it has helped countries reduce dependence on one currency, reduced forex volatility among other benefits.

Coming back to China and Brazil, let’s talk about BRICS+?

BRICS represents a group of emerging market countries: Brazil, Russia, India, China, and South Africa. BRICS+ refers to the expanded version, which includes additional countries, such as Egypt, Ethiopia, Indonesia, Iran, and the UAE.

Why are we talking about BRICS+?

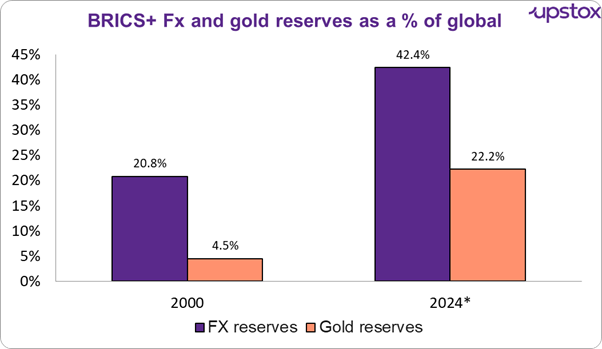

In the past 10 years, the BRICS+ nations have bolstered their gold reserves by 5x, significantly enhancing their buying power and also worked on establishing a universally trusted safeguard for their financial transactions.

During the same period, their foreign reserves have doubled, which gives them enough dry powder to confidently trade in the global markets. Together, these strides empower BRICS+ countries with greater autonomy in global trade and finance.

Source: IMF, WB, BIS, SWIFT, Refinitiv, national sources, ING, Note: *Latest available data of 2022-24

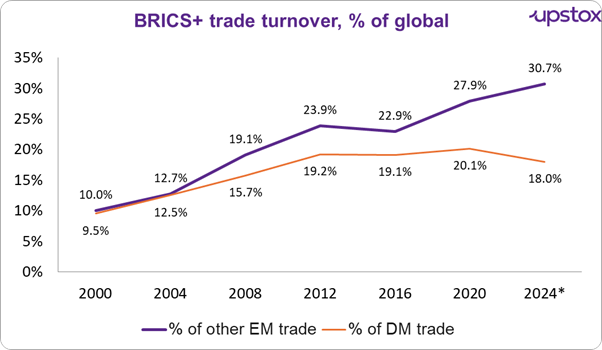

At the same time BRIC+ countries continue to hold a meaningful amount of US dollar which provides them with flexibility to engage in trade with developed markets or nations that predominantly rely on the US dollar.

This is particularly evident when you look at the increase in trade between BRICS+ nations and other emerging markets which we will explore below.

Source: IMF, WB, BIS, SWIFT, Refinitiv, national sources, ING, Note: *Latest available data of 2022-24, Emerging markets (EM), Developed market (DM).

Since 2000, the trade turnover between BRICS+ nations and all emerging market countries has tripled as a share of total trade. Similarly, their trade share with developing markets has nearly doubled during this period.

So what does de-dollarisation actually look like in practice? One country that’s already deep into this shift is Russia—and its experience offers a glimpse into the challenges and workarounds involved.

Case study: How Russia is surviving without the dollar

When Western sanctions hit in 2022, following the invasion of Ukraine, Russia was swiftly cut off from most of the dollar-based global financial system. Key banks were removed from SWIFT, the country’s foreign reserves in the West were frozen, and access to the US dollar was heavily restricted.

But instead of being paralysed, Russia pivoted fast.

-

It began settling the bulk of its trade with China in rubles and yuan—a share that crossed 90% by the end of 2023. The use of CIPS, China’s own cross-border payment system, rose sharply as an alternative to SWIFT. Meanwhile, trade with countries like India shifted to non-dollar arrangements, including the rupee and even barter-like systems in some cases.

-

Russia also dumped most of its US Treasury holdings and boosted its gold reserves, reinforcing its financial defences. Domestically, the government pushed firms to repatriate foreign earnings and reduce exposure to Western banks.

Of course, the process hasn’t been smooth. India-Russia trade has hit snags due to rupee convertibility issues, and alternative systems like CIPS which handles around 25,900 transactions on average still lack the scale of SWIFT of about 44.8 million .

But the key takeaway is this: Russia didn’t just talk about de-dollarisation—it acted, under pressure, and created new trade channels outside the traditional dollar-based system. It’s not perfect. But it’s real—and it shows how de-dollarisation can move from concept to reality when the stakes are high. Next we will look at the global implications of de-dollarisation

What are the global impacts of these?

The good

-

Lower costs and faster trade: Skipping dollar conversions speeds up transactions and cuts fees.

-

More breathing room for weaker economies: Countries with dollar shortages (like Argentina or Ethiopia) gain a practical lifeline.

-

Freedom from US policy swings: By reducing reliance on the dollar, nations limit their exposure to Fed rate hikes, sanctions, and US-centric financial shocks.

-

Boosting local currency strength: Nations like Brazil and Russia are pushing the yuan and ruble to strengthen regional trade ties and promote currency self-reliance.

-

Greater financial autonomy: Moving away from a dollar-dominated system gives BRICS+ countries more control over their trade and monetary decisions.

-

Multipolar currency system: Establishing alternatives to the dollar fosters diversity in the global financial system, potentially creating a fairer balance of economic influence.

The bad

-

Exchange rate volatility: Moving away from the dollar could lead to greater fluctuations in currency values, especially in nations with less developed financial markets. This instability could disrupt trade and investment.

-

Liquidity constraints: BRICS currencies and other alternatives are far less liquid and less widely accepted than the US dollar, making global trade a bit trickier and slower.

-

Implementation hurdles: Adopting local currencies or introducing a BRICS currency faces practical barriers. For instance, banking concerns over US sanctions have slowed progress in India-Russia trade.

The ugly

-

Fragmentation of the financial system: As regional monetary blocs strengthen, the global financial system could become more fragmented. This risks reducing economic efficiency and destabilising international trade networks.

-

Potential dominance of China: As the largest economy within BRICS+, China’s push for the yuan’s internationalisation raises concerns about it overshadowing other member nations’ interests, such as those of India or Brazil.

-

Impact on US global standing: De-dollarisation could weaken US economic leverage, reducing the effectiveness of dollar-based sanctions and shifting power to new financial centres. This poses challenges for US diplomacy and economic policies. As such the USA is unlikely to take this lightly. It may respond aggressively, employing assertive measures to safeguard its global influence.

Outlook

We’re talking about de-dollarisation because it’s not just political chatter anymore—it’s starting to reshape real trade flows, reserves, and risk exposure globally. For investors, this could signal long-term shifts in currency dominance, market dynamics, and where the next financial power centres may emerge.

About The Author

Next Story