Upstox Originals

Is ChatGPT the undisputed AI champion or the lagging giant?

5 min read | Updated on May 05, 2026, 13:54 IST

SUMMARY

900 million weekly users and 18 billion messages a week—hardly the profile of a struggling product. And yet, ChatGPT is losing market share. From an unrivaled pioneer, it has become just another participant in a crowded AI ecosystem. The numbers reveal a far more nuanced story than the headlines imply.

ChatGPT still sees 900 million weekly active users and processes over 2 billion prompts a day

For most of its short life, ChatGPT had no serious competition. It was launched in November 2022, crossed 100 million users in two months — faster than any consumer product in history. For a while, “ChatGPT” and “AI” were synonymous.

Today, ChatGPT still sees 900 million weekly active users and processes over 2 billion prompts a day. By any normal measure, those are extraordinary numbers. However, in late April 2026, as per the Wall Street Journal, OpenAI had missed not one but three internal targets:

- Its goal of one billion weekly active users for ChatGPT

- Its full-year 2025 revenue target

- Multiple monthly sales targets in the early months of 2026

The timing is particularly uncomfortable. OpenAI is racing toward what could be the largest technology IPO in years, targeting a Nasdaq listing in Q4 2026 at a valuation of nearly $1 trillion.

So what is actually happening here? Is ChatGPT in decline — or is this something more complicated?

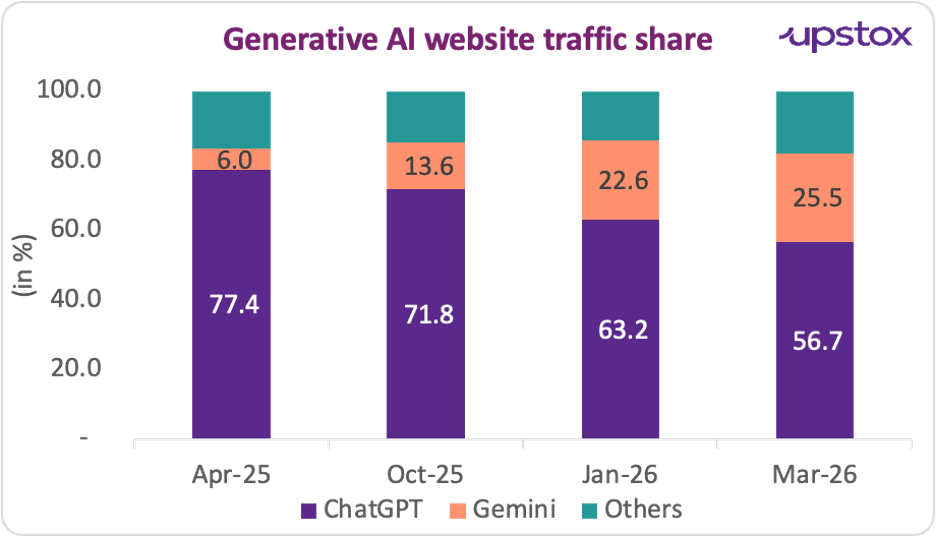

Market share losses

Looking at the web traffic share, ChatGPT has been steadily ceding ground to competition.

Source: SimilarWeb’s Global AI Tracker; GREED & Fear - April 2026

Besides this, ChatGPT’s recent quarterly growth figure has also raised some flags. While ChatGPT is still the largest AI platform by a considerable margin, it is growing at just 4% per quarter. Claude is growing at 14%, and Gemini at 12%. In a market that is expanding rapidly, slow growth is how a player loses market share without losing users.

The real culprit: Distribution

ChatGPT's falling market share highlights a structural problem rather than a quality issue. For instance, Gemini’s gains are driven almost entirely by where it ships, not what it does. Gemini is now embedded by default inside Android phones, Google Search, Google Workspace and NotebookLM.

Research and analytics platform SimilarWeb found that twice as many US users access Gemini through their operating system than through gemini.google.com. Referral traffic from Gemini to the wider web grew 388% year-on-year, compared to 52% for ChatGPT. The implication is stark: ChatGPT is something you choose to open. Gemini is something you stumble into. One requires a decision; the other requires no decision at all.

The enterprise story should also raise some concerns

Consumer market share is one thing. Enterprise is another.

ChatGPT still has formidable enterprise numbers: over one million paying businesses, around seven million enterprise seats, and a reported usage across 92% of Fortune 100 companies.

But the composition of enterprise AI spending has shifted dramatically. The reversal in new enterprise buyer preference is the most striking figure.

Enterprise AI market share shift (2023 vs March 2026)

| Metric | OpenAI (2023) | OpenAI (Mar 2026) | Anthropic (2023) | Anthropic (Mar 2026) |

|---|---|---|---|---|

| Share of new enterprise buyers choosing the platform | ~70% | 27% | ~5% | 73% |

Source: Ramp enterprise spending report (March 2026)

The reason is functional. Only 4.2% of ChatGPT messages relate to programming, while 33% of Claude’s enterprise conversations involve coding. Claude also offers a larger context window, which matters when processing long legal documents, codebases or financial reports.

In comparative reliability studies across specialist domains, ChatGPT produced significantly more errors. For enterprise buyers, especially in regulated industries, these differences are not marginal — they determine which product gets signed.

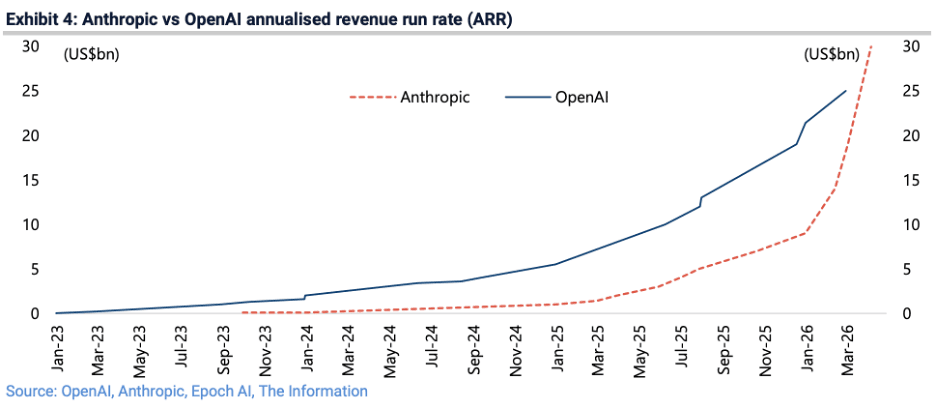

The revenue paradox

The strangest part of this story is what it looks like in revenue terms.

Source: GREED & Fear - April 2026

Anthropic, which has roughly 18.9 million monthly active web users against ChatGPT’s hundreds of millions, now generates a higher annualised revenue run-rate than OpenAI. It reflects a deliberate difference in strategy: roughly 80% of Anthropic’s revenue comes from enterprise contracts and API usage, not consumer subscriptions.

This is further exacerbated by uncomfortable unit economics. Only about 5% of ChatGPT’s weekly users are paying subscribers. That means 95% are using the product for free, and every query those free users submit costs OpenAI real money in compute, electricity and inference time. Sam Altman has acknowledged that even the $200-per-month Pro tier runs at a loss.

OpenAI is aware of the conversion problem. In early 2026, the company began testing personalised advertisements within ChatGPT for free-tier users — a signal that the path to monetising its enormous user base is proving harder than the growth numbers suggested.

So is ChatGPT actually in trouble?

The answer depends entirely on what you are measuring.

In absolute usage, not at all. Nine hundred million weekly users processing 18 billion messages per week is not a company in trouble.

On relative market share, maybe. On monetisation and enterprise relevance, this is the genuine problem.

The IPO question puts a sharp edge on all of it. Public market investors will be asked to buy into a company that plans to lose enormous sums for several more years, betting on eventual dominance that is becoming less certain by the quarter.

ChatGPT did not lose because it got worse. It lost share because AI stopped being a place you visit — and became something you stumble into everywhere else. The question now is whether OpenAI can find a business model that works before the compute bills come due.

About The Author

Next Story