Upstox Originals

Oil shock returns: What India learned from the really brutal ones

7 min read | Updated on March 09, 2026, 15:28 IST

SUMMARY

Oil markets have entered uneasy territory again, and India finds itself exposed to major shocks. But this is not the first time oil shocks have tested the country. From the 1970s oil crisis, when the oil prices surged nearly 300% to the Gulf War, India has faced far worse spikes before. What did we learn from those crises and what options does India have today?

India is the world’s third-largest consumer of crude oil | Image: Shutterstock

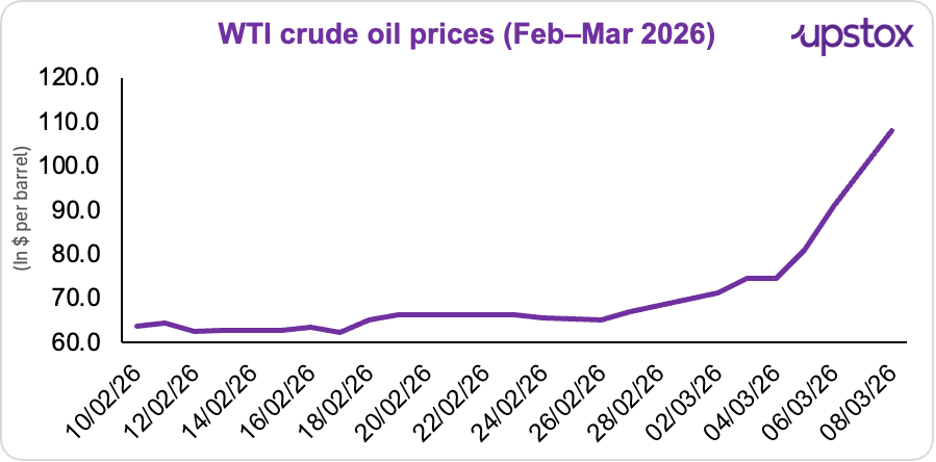

With the Strait of Hormuz shut, oil prices just jumped nearly 61% - from $67 per barrel on February 27 to $108 by March 8, 2026.

Source: Investing.com

For India, this is a major challenge.

You see, India is the world’s third-largest consumer of crude oil, and it imports about 88% of what it uses. Every single day, around 5 million barrels arrive on Indian shores. About 50% of those shipments pass through the Strait of Hormuz.

That’s roughly 2.5–2.7 million barrels a day, mostly coming from Iraq, Saudi Arabia, the UAE and Kuwait.

But well, we’ve seen worse.

Back in the 1970s oil crisis, prices didn’t just climb 61%. They shot up nearly 300% after the shocks of 1973.

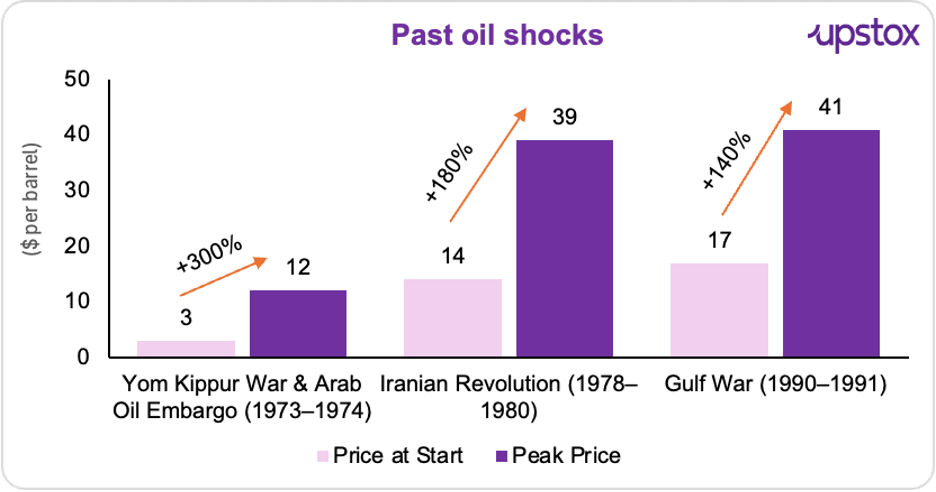

Looking back at some periods of major oil shocks

Oil markets have seen several major shocks over the years. And each of them triggered sharp price jumps.

Source: Equirus Research

The 1973 Oil Shock (Yom Kippur War & Arab Oil Embargo)

In October 1973, global oil markets got their first real scare.

Tensions in the Middle East disrupted oil supplies. Some producers restricted exports. Production was cut too. Suddenly, the world had 4–5 million barrels of oil per day less, approximately 7–9% of global supply (the world was producing ~55 million barrels per day then).

Prices reacted immediately.

Crude that cost around $3 per barrel in early 1973 jumped to about $5 within months, and by 1974 it was nearing $12, a 300% surge in just a year.

India felt the shock almost instantly.

The oil import bill jumped from about $500 million in 1973 to roughly $1.3 billion in 1974. Suddenly, oil imports were eating up around 40% of India’s export earnings. In fact, the oil bill alone was almost twice India’s foreign exchange reserves.

That’s the kind of situation that keeps policymakers up at night.

India couldn’t control global oil prices. But it could rethink how it powered the economy. Soon after, in 1974, ONGC discovered Bombay High, India’s largest offshore oil field, a major turning point that reduced dependence on imported oil.

At the same time, India leaned more on coal. Production, which had been stuck around ~75 million tonnes a year, rose steadily to about ~109 million tonnes by 1980 as coal-powered more electricity and industry.

The crisis also triggered a longer-term shift. It eventually led to institutions like the Petroleum Conservation Research Association (PCRA), focused on improving fuel efficiency and reducing oil consumption.

The Iranian Revolution & the Second Oil Shock (1978–1980)

Just as the world was beginning to recover from the first oil shock, chaos struck again. In 1978, Iran, one of the world’s largest oil producers, was hit by the Iranian Revolution, disrupting its oil industry. Suddenly, the world lost around 4–5 million barrels of oil per day, roughly 6–8% of global supply.

Now look at what happened next.

Oil that cost about $14 per barrel in 1978 surged to nearly $39 by 1980, a ~180% jump. India felt the heat too. The Economic Survey (1979–80) shows the Wholesale Price Index rising from 191.0 in March 1979 to 229.1 by March 1980, a 19.9% spike in just a year. And the economy actually shrunk, with GDP contracting 5.2% in 1979–80.

So how did India keep the lights on?

First came the Soviet lifeline. Through Rupee–Rouble trade agreements, India could buy oil from the Soviet Union without using scarce US dollars. But the pressure was still too high. So in 1981, India turned to the IMF, securing a $5 billion loan (did you know this was India’s first major IMF bailout?) to stabilise the economy.

The Gulf War (1990–1991)

When Iraq invaded Kuwait in 1990, oil markets panicked.

Prices jumped from $17 per barrel in July 1990 to nearly $41 by October, a ~140% spike. Now imagine being a country that depends heavily on imported oil.

For India, the shock was brutal. The oil import bill surged to ₹10,820 crore, up 72% from ₹6,273 crore the previous year. Meanwhile, foreign exchange reserves fell to barely three weeks of import cover.

Then came another blow. Moody’s and S&P downgraded India to “junk.” (What does that mean? Simply put, lenders start seeing you as risky. So borrowing money abroad suddenly becomes very difficult.)

So what did India do?

In October 1990, the government imposed a 25% Gulf Surcharge on petroleum products (except domestic LPG). But the crisis ran deeper. In May 1991, the State Bank of India sold 20 tonnes of gold, raising about $200 million.

Then in July 1991, the RBI shipped another 47 tonnes of gold abroad to raise more dollars.

The crisis ultimately was one of the major drivers that pushed India to dismantle the License Raj and launch the 1991 economic reforms.

Other global events that triggered oil price spikes

| Event (Year) | Price at Start (USD) | Peak Price (USD) | % Increase | Price at End (USD) | Impact on Actual Supply During Crisis | Impact as % of Total Global Supply |

|---|---|---|---|---|---|---|

| Iran–Iraq War (1980–1981) | 32 | 40 | 25% | 28 | Severe damage to oil facilities; exports from both countries reduced early in the conflict | ~5–6% (global supply ~65 mb/d) |

| Iraq War (2002–2003) | 25 | 35 | 40% | 23 | Initial disruption of ~2 mb/d; instability slowed recovery of Iraqi production | ~2–3% (global supply ~80 mb/d) |

| Libyan Civil War (2011) | 95 | 125 | 30% | 110 | Around 1.5 mb/d of Libyan exports temporarily halted | ~1.6–2% (global supply ~90 mb/d) |

| Russia–Ukraine War (2022) | 75 | 130 | 73% | 85 | 2–3 mb/d of Russian exports disrupted or rerouted due to sanctions | ~2–3% (global supply ~100 mb/d) |

Source: Equirus Research

What levers does India have this time?

India still has a few buffers. India currently holds around 100 million barrels of crude oil in refinery and commercial storage. Based on current consumption levels, this stock can meet the country’s oil requirements for roughly 40–45 days, according to estimates by energy analytics firm Kpler, as reported by PTI.

If needed, India could also cut exports of fuels like diesel and jet fuel to keep more supply at home.

Another option is buying crude from elsewhere; the US, West Africa or Latin America. But those shipments take 25–45 days to reach India, compared with just 5–7 days from the Gulf, making them slower and costlier.

Could Russian oil help again?

Possibly.

Earlier, the US had pushed India to reduce Russian oil purchases (after the recent deal signed). But with tensions rising, Washington has now opened a temporary 30-day window for India to import Russian crude.

Indian refiners were already buying around 1 million barrels per day, and flows could rise to 1.6–2 million barrels per day.

There’s supply available too. Around 145 million barrels of Russian crude are currently floating on ships across the Indian Ocean, Red Sea/Suez routes and near Singapore.

But, China is also chasing the same barrels, so the Russian oil may not be available at the same discount.

So yes, India has a few levers to pull. But if tensions around Hormuz worsen, the real test will be how long those buffers can last.

About The Author

Next Story