Personal Finance News

Income above ₹1 crore brings an extra ITR task: Here's how to get it right for AY 2026-27

6 min read | Updated on July 06, 2026, 17:09 IST

SUMMARY

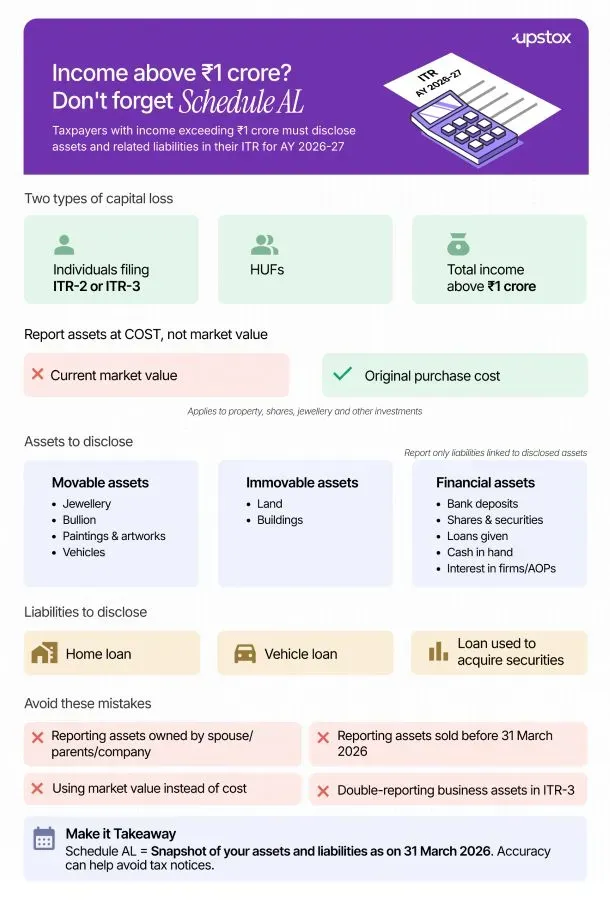

Schedule AL applies to individual and HUF taxpayers filing ITR-2 and ITR-3. Companies filing ITR-6 are required to disclose their assets and liabilities in Schedule AL-1 and Schedule AL-2.

Know about Schedule AL for AY 2026-27.

When your income crosses ₹1 crore, you are required not only to file your return like all other taxpayers but also to complete an extra task: report all your assets and liabilities under Schedule AL of the Income-tax Return (ITR) form. Not doing so correctly can lead to notices.

"‘Schedule AL’ applies to Individuals and Hindu Undivided Families (HUFs) who are required to file this return and whose total income exceeds ₹1 crore in the financial year. This schedule mandates disclosure of details related to assets and liabilities held at the end of the year, aimed at ensuring greater financial transparency and preventing tax evasion," the Income Tax Department says on its website.

Schedule AL applies to individual and HUF taxpayers filing ITR-2 and ITR-3. Companies filing ITR-6 are required to disclose their assets and liabilities in Schedule AL-1 and Schedule AL-2.

As the ITR filing due date for AY 2026-27 approaches, many taxpayers remain confused about what to report under Schedule AL and what to ignore. This article aims to help such taxpayers with a quick guide on how to get Schedule AL right, with inputs from CA Dr Suresh Surana.

Why is this important?

"With increased scrutiny on high‑value taxpayers, Schedule AL (Assets and Liabilities) in Income Tax Returns has become a key compliance requirement. Applicable mandatorily to individuals and HUFs with total taxable income exceeding ₹1 crore, the schedule offers the tax department details of a taxpayer’s financial position as on 31 March of the relevant financial year," said Dr Surana.

"In case of a non-resident or a resident but not ordinarily resident, only assets located in India are required to be reported in Schedule AL," he added.

How to calculate

For calculating the amount to be reported in ITR for AY 2026-27, you should prepare a statement of assets and liabilities as at the end of the previous financial year, i.e., assets held and liabilities outstanding as on 31 March 2026.

Disclose cost, not FMV

According to CA Sr Suresh Surana, you need to disclose assets on a cost basis and not on their fair market value (FMV). For example, if you hold listed shares. You do not have to report its current market price. Rather, the cost at which you had purchased should be disclosed.

"Schedule AL requires disclosure on a cost basis and not on the basis of fair market value. Therefore, appreciation in the value of immovable property, jewellery, listed shares, mutual funds or other investments should not be substituted for cost merely because the current market value is higher," said Dr Surana.

"In case of jointly held assets, only the taxpayer’s share should generally be reported, supported by ownership records and funding details," he added.

Assets to disclose

Broadly, taxpayers should disclose the following movable, immovable and financial assets:

| Movable assets | Immovable Assets | Financial Assets |

|---|---|---|

| Jewellery | Land | Bank balances, including deposits |

| Bullion | Building | Shares and securities |

| Archaeological collections | Loans and advances given | |

| Drawings | Cash in hand | |

| Paintings | Interest in the assets of a firm or association of persons as a partner or member | |

| Sculptures or works of art | ||

| Vehicles | ||

| Yachts, boats and aircraft |

The following are some examples of three types of assets:

-

Jewellery: Gold necklaces, diamond rings, bracelets

-

Bullion: Gold bars, silver bars, gold coins

-

Archaeological collections: Antique artefacts, historical relics

-

Drawings: Original sketches, architectural drawings

-

Paintings: Oil paintings, watercolours

-

Sculptures or works of art: Bronze sculptures, contemporary artworks

-

Vehicles: Cars, motorcycles, SUVs

-

Yachts, boats and aircraft: Private yachts, speedboats, private aircraft

-

Land: Residential plots, agricultural land, commercial plots

-

Building: Houses, apartments, commercial buildings, office premises

-

Bank balances, including deposits: Savings accounts, current accounts, fixed deposits

-

Shares and securities: Equity shares, bonds, debentures, mutual fund units

-

Loans and advances given: Personal loans to relatives, business advances

-

Cash in hand: Cash held at home or office

-

Interest in the assets of a firm or association of persons: Partnership firm capital, LLP interest, membership interest in an AOP

Avoid double reporting in ITR-3

In ITR-3, Schedule AL specifically captures the taxpayer’s interest in the assets of a firm or association of persons as a partner or member

"Where the taxpayer files ITR-3 and maintains books of account for a proprietary business or profession, taxpayer need to ensure to avoid double reporting. The notified ITR-3 Schedule AL refers to assets and liabilities at the end of the year “other than those included in Part A-BS”. Accordingly, business assets and business liabilities already disclosed in the proprietary balance sheet should generally not be duplicated again in Schedule AL," Dr Surana said.

Liabilities to disclose

Taxpayers are required to report liabilities only to the extent they are relatable to the assets disclosed in Schedule AL.

For example, an outstanding housing loan against an immovable property, a vehicle loan against a vehicle, or a loan taken for acquiring securities may be considered.

The amount to be reported should be the outstanding liability as at year-end.

What can be excluded

Taxpayers can exclude the following from Schedule AL:

- Assets not held as on the last day of the previous year

However, you should disclose any income or capital gains arising from the transfer of those assets separately in the relevant income schedule.

- Assets belonging to another person, even if you are their nominee, facilitator or signatory

"For example, assets of spouse, parents, children, company, firm or trust, should not be reported merely because the taxpayer is a nominee, authorised signatory or facilitator, unless the taxpayer has an ownership or reportable economic interest," said Dr Surana.

- Liabilities not connected with the assets disclosed in Schedule AL

You should not adjust such liabilities against the asset value.

Maintain documents

Dr Surana said that taxpayers should reconcile Schedule AL with property purchase documents, loan statements, bank and fixed deposit statements, demat and broker statements, insurance records, jewellery purchase records, capital account and business balance sheet, wherever applicable.

"Since the schedule seeks disclosure at cost, taxpayers should maintain supporting documents for the cost reported, particularly in respect of old assets, inherited assets, gifted assets, jointly held assets and assets acquired through reinvestment or conversion," he added.

Related News

About The Author

Next Story