Personal Finance News

ITR filing for pensioners AY 2026-27: Which forms, deductions and tax rules apply?

4 min read | Updated on May 26, 2026, 07:19 IST

SUMMARY

For Assessment Year 2026-27, pensioners can choose between multiple ITR forms depending on their income sources. Senior citizens also continue to get several tax benefits, including higher deductions on interest income, medical expenses, and health insurance under the old tax regime.

Most retired salaried individuals can use ITR-1. | Image: Shutterstock.

For Assessment Year 2026-27, pensioners can choose between multiple ITR forms depending on their income sources. Senior citizens also continue to get several tax benefits, including higher deductions on interest income, medical expenses, and health insurance under the old tax regime.

In this article, we try to explain, deductions, tax slabs, and exemptions every pensioner should know before filing returns.

Which ITR form should pensioners file for AY 2026-27?

Choosing the wrong ITR form is one of the most common mistakes made by retirees. The right form depends on the type of income earned during the financial year.

Most retired salaried individuals can use ITR-1.

This form can be filed if total income is up to Rs 50 lakh and income comes from:

-

Salary or pension

-

One house property

-

Other sources such as interest, dividend, and family pension

-

Agricultural income up to ₹5,000

ITR-2 becomes applicable when income is more complex. This form is generally used if a pensioner has:

-

Multiple house properties

-

Higher capital gains

-

Foreign assets or income

-

Income exceeding the eligibility conditions of ITR-1

ITR-3 is applicable where an individual or HUF has income from profits and gains of business or profession.

ITR-4 can be filed by resident individuals, HUFs, and firms (other than LLPs) having total income up to Rs 50 lakh and presumptive business or professional income under Sections 44AD, 44ADA, or 44AE.

It also includes income from:

-

Salary or pension

-

One house property

-

Other sources

-

Agricultural income up to ₹5,000

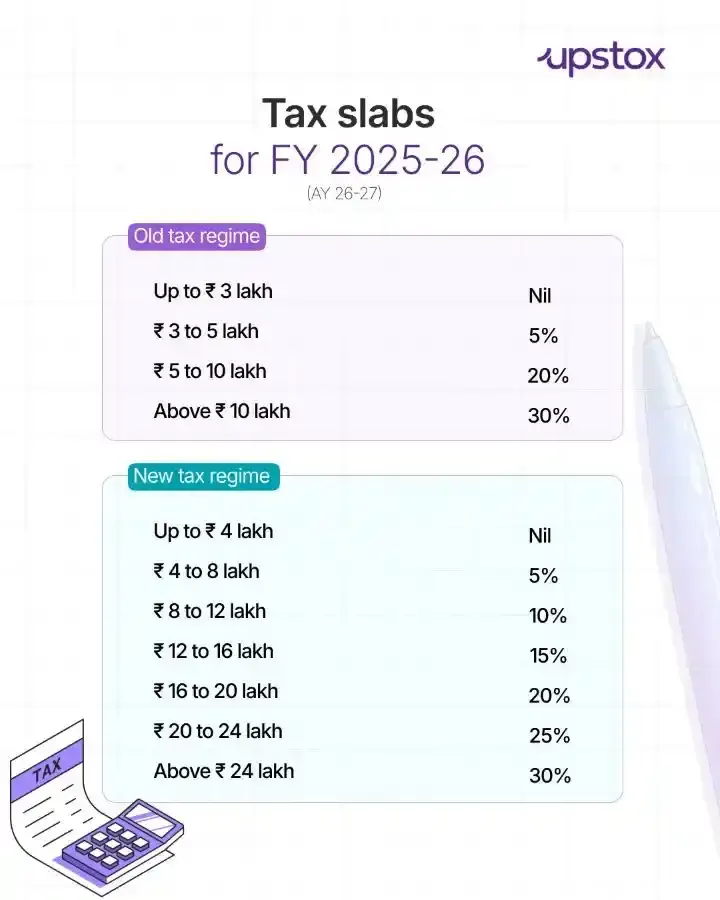

Tax slabs for senior citizens AY 2026-27

Resident individuals under the new tax regime can also claim rebate under Section 87A if taxable income does not exceed ₹12 lakh. The provisions of section 87A are covered under section 156 of the Income Tax Act, 2025.

However, for income earned until 31st March 2026 (FY 2025-26), the provisions in the Income Tax Act 1961 needs to be referred, since the concern income is earned before the new act come into force

Key deductions available to pensioners

-

Savings accounts

-

Fixed deposits

-

Post office deposits

Deduction for health insurance premium:

- Up to ₹50,000 for senior citizens

Additional deduction available for parents if they are senior citizens

Deduction for treatment of specified diseases:

Up to ₹1 lakh for senior citizens

Under the new income tax act 2025 (Income Tax Bill), Section 80C has been restructured and renamed as Section 123.

Deduction up to ₹1.5 lakh on eligible investments including:

-

Life insurance premium

-

Provident Fund

-

NSC

-

Housing loan principal repayment

Section 24(b)

Deduction on housing loan interest:

Up to ₹2 lakh for self-occupied property under old tax regime

The new Income Tax Act, 2025 came into effect from April 1, 2026. However, since AY 2026-27 relates to income earned during FY 2025-26, taxpayers will continue to file returns and calculate taxes under the existing provisions of the Income Tax Act, 1961.

For Assessment Year 2026-27, the tax department has already activated filing utilities for some forms.

The department has enabled both online filing and Excel utility for ITR-1 and ITR-4, allowing taxpayers to begin filing returns for income earned in FY 2025-26.

Related News

About The Author

Next Story