Personal Finance News

Can you get tax-free ₹1 lakh/month from ₹1.5 crore in RBI bonds? Will it last through retirement?

3 min read | Updated on May 19, 2026, 10:13 IST

SUMMARY

The interest rate on RBI Floating Rate Savings Bonds is pegged to the prevailing National Savings Certificate (NSC) rate with a spread of (+) 35 bps of the respective bps.

RBI floating rate savings bonds are offering 8.05% interest at present.

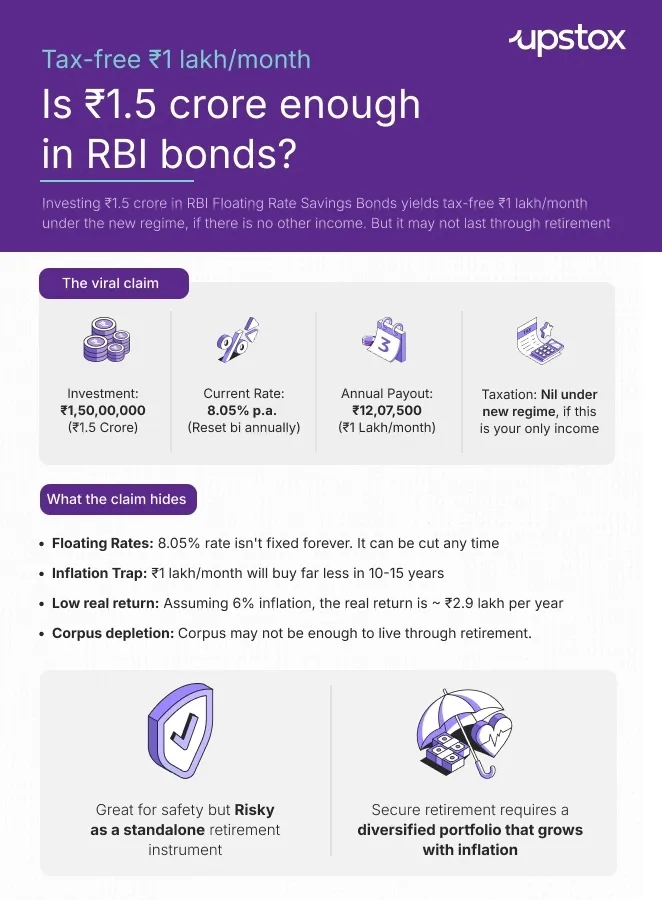

A popular post on X recently claimed that an investor needing ₹1 lakh per month can get it not only hassle-free but also tax-free by investing ₹1.5 crore in RBI Floating Rate Savings Bonds (FRSB). This article examines whether this claim is true and whether such a withdrawal can last through your retirement.

Is this claim true?

Yes, the claim is true, but partially as the corpus may not last forever.

Let's see the math.

Currently, RBI FRSBs are offering 8.05% interest per year. By investing ₹1.5 crore in these bonds, an investor can get around ₹12 lakh per year, which works out to be ₹1 lakh per month.

₹1,50,00,000*8.05% = ₹12,07,500

Is this ₹12 lakh tax-free?

Income up to ₹12 lakh is tax-free under the new tax regime. A person earning ₹12 lakh from FRSB needs to pay zero tax under the new regime, provided he has no income from any other sources.

The interest rate on these savings bonds is pegged to the prevailing National Saving Certificate (NSC) rate with a spread of (+) 35 bps of the respective bps. Offered directly by the RBI, these bonds are also among the safest savings instruments.

Will it last through retirement?

The big question for any wise investor is: will the money invested in FRSB last through retirement? Or, can you fully rely on this income for your ₹1 lakh monthly requirement?

The answer is: No.

And there are at least two reasons.

First, the interest rate on FRSB is not fixed forever. It is reset every six months. While the current rate of 8.05% seems high, there is no guarantee it will remain unchanged forever. In case there is any downward revision of the FRSB interest rate in the future, you may not be able to earn ₹12 lakh per year.

Second, relying fully on FRSB can be risky due to inflation.

The real value of ₹12 lakh per year can diminish over time due to inflation, and it may not last through retirement.

For example, suppose annual inflation is 6%, and you are getting ₹12 lakh per year from FRSB at 8.05% by investing ₹1.5 crore.

Invested amount = ₹1.5 crore

Return = 8.05% (₹12.07 lakh/year)

Inflation = 6%

You are spending the full ₹12 lakh each year

In real terms, your money is growing only at about 1.9% per year [(1.0805/1.06) - 1 = 1.9%].

The real return on ₹1.5 crore is just approx. ₹2.9 lakh per year (₹1.5 crore x 0.019%). But you are withdrawing ₹12 lakh per year, which means every year you are eating into your principal by approx. ₹9.1 lakh in today's value. This also means the corpus will not last through retirement. The corpus depletion may even speed up if the inflation or your withdrawal rate rises further.

To counter the impact of inflation on your corpus, you may invest a small part of your corpus in growth assets like equity after taking guidance from any trusted investment advisor or retirement planner.

Related News

About The Author

Next Story