Market News

Week ahead: US-Iran tensions, crude oil prices, auto sales number, US jobs data among key market triggers to watch

.png)

4 min read | Updated on June 28, 2026, 11:07 IST

SUMMARY

NIFTY50 ended the week above 24,000 but remains range-bound, with 24,200 acting as a key resistance and 23,650 as immediate support. The week ahead will be guided by June auto sales, U.S. labour-market data, crude oil prices and developments around US-Iran tensions, while FII flows and market breadth will remain important for assessing the strength of the recovery.

FIIs continue to remain net seller this month as well, selling equities worth over ₹45,000 crore in cash market. | Image: Shutterstock

Indian markets ended the holiday-shortened week on a positive note, with the NIFTY50 reclaiming 24,000 during the week. This comes on the backdrop of easing geopolitical concerns and easing crude oil prices lifted risk-on sentiment.

For the week, SENSEX gained 0.3% to 77,100, while the NIFTY50 index rose 0.1% to 24,056. Broader markets also paused two weeks' momentum and ended the week on a negative note. The NIFTY Midcap 150 slipped 0.9% to 22,751 Smallcap 250 index closed flat at 17,704.

Sectoral action was also selective. The Pharma (+2.8%), Tourism (+2.7%) and Private Bank (+1.0%) indices, while Metals (-4.3%), IT (-4.0%) and CPSE (-3.2%). Meanwhile, as markets enter the new week, investors will watch whether the fall in crude sustains.

For the coming week, investors should track the direction of the U.S. dollar, evolving expectations around the Fed’s rate path, and movements in LME base-metal prices. Against this backdrop, shares of Vedanta (-10.6%), National Aluminum (+9.7%) and Hindustan Zinc (+9.3%) were the top losers.

On the domestic front, investors will watch the Manufacturing and Services PMI readings for an update on demand conditions and private-sector activity. Additionally, June monthly automobile sales will also keep the auto sector in focus.

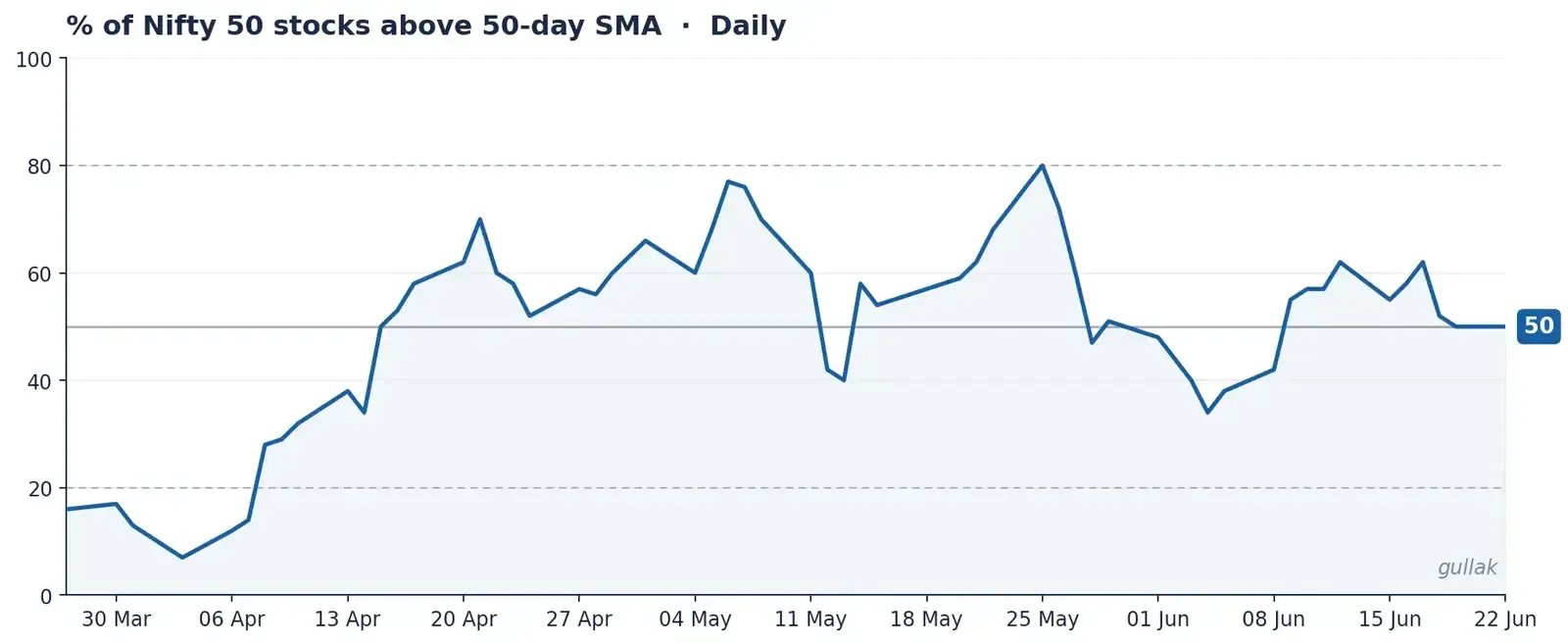

Market breadth

Market breadth improved sharply in the second half of June, with the proportion of Nifty50 stocks trading above their 50-day simple moving average rising from 34 percent in early June to 62 percent around the middle of the month. However, the breadth has since eased back to 50 percent, meaning only 25 of the 50 Nifty stocks are currently trading above their 50-day average.

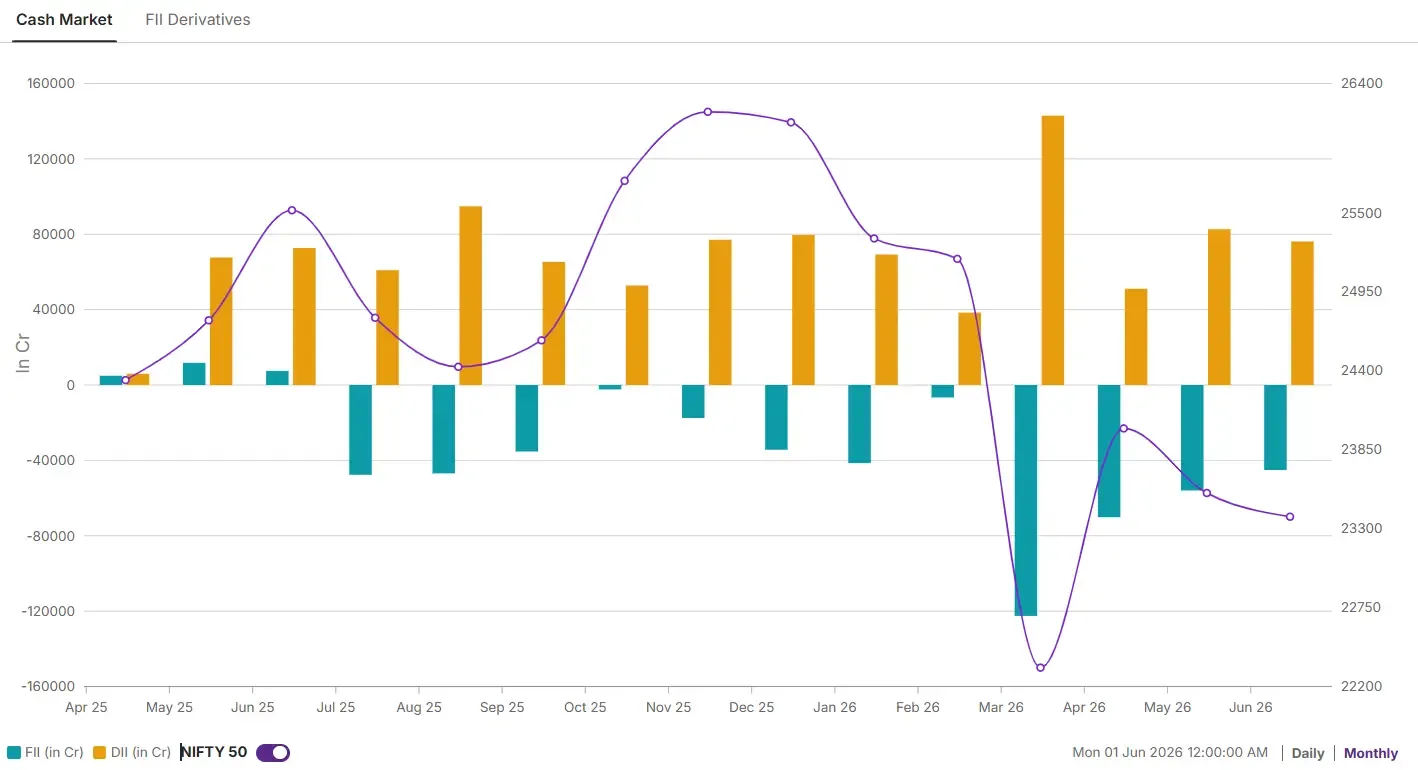

Foreign investors positioning

Foreign institutional investors continued to remain on the sell side in June, offloading Indian equities worth around ₹45,000 crore in the cash market. This marks the fourth consecutive month of net selling and follows outflows. Meanwhile, the Domestic institutional investors continued to absorb the selling pressure, with net purchases of about ₹76,000 crore in June.

NIFTY50 outlook

The Nifty50 index continues to face selling pressure near the 24,200 zone, which coincides with the June 18 swing high. A decisive close above this level will signal an improvement in momentum and could open the door for a move towards higher levels.

On the downside, the 23,650 zone remains the immediate support to watch. This area also aligns with the June 15 gap and the 20-day EMA. A close below 23,650 would indicate renewed weakness and may lead to further profit booking.

For now, the index remains range-bound between 23,650 and 24,200. A breakout on either side of this range is likely to determine the next directional move.

Disclaimer:

Derivatives trading must be done only by traders who fully understand the risks associated with them and strictly apply risk mechanisms like stop-losses. We do not recommend any particular stock, securities, or trading strategies. The securities quoted are exemplary and not recommendatory. The stock names mentioned in this article are purely to show how to do analysis.

About The Author

Next Story