Market News

Week ahead: Middle East crisis, crude oil price surge, FIIs activity among key market triggers to watch

4 min read | Updated on March 08, 2026, 12:21 IST

SUMMARY

In the week ahead, markets are likely to remain volatile. Investors will be closely tracking the escalating tensions between the US and Iran, the spike in crude oil prices, movements in the rupee and foreign fund flows.

Stock list

FIIs have begun March on a weak note, offloading equities worth ₹15,800 crore. | Image: Shutterstock

Indian equities ended last week on a volatile note, with benchmark indices coming under pressure amid rising crude oil prices and cautious global sentiment. The NIFTY50 ended the week at 24,450, down 2.8%, while the Sensex dropped 2.9% to 78,918, reflecting a broad risk-off mood across the market.`

A key trigger behind the decline was the sharp rise in crude oil prices, which heightened concerns over India’s inflation outlook and trade deficit. Since India is a major crude importer, higher oil prices tend to pressure the rupee, corporate margins and fiscal expectations.

Broader markets also remained under pressure, with Midcap 150 index and Smallcap 250 index witnessed sharper declines of around 3%. Overall, the week reflected a combination of global macro concerns, commodity price volatility, which kept market sentiment fragile.

Sectorally, except for Defence (+4.8%) and Pharma (+0.8%), all the major sectoral indices ended the week in red. PSU Banks (-6.4%), Real-Estate (-4.9%) and Private Banks (-4.1%) declined the most/

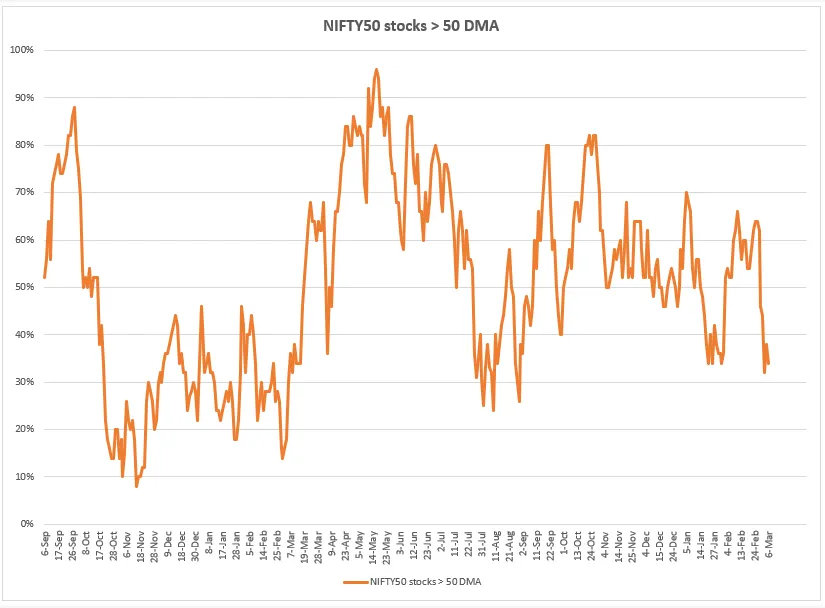

Market breadth

NIFTY’s market breadth weakened sharply this week, with the percentage of NIFTY50 stocks trading above their 50-day moving average slipping from around 60% to nearly 35%. This sharp decline indicates a clear deterioration in participation beneath the index, suggesting that a growing number of stocks have fallen below key short-term trend levels. The move reflects broad-based selling pressure rather than weakness limited to a few sectors.

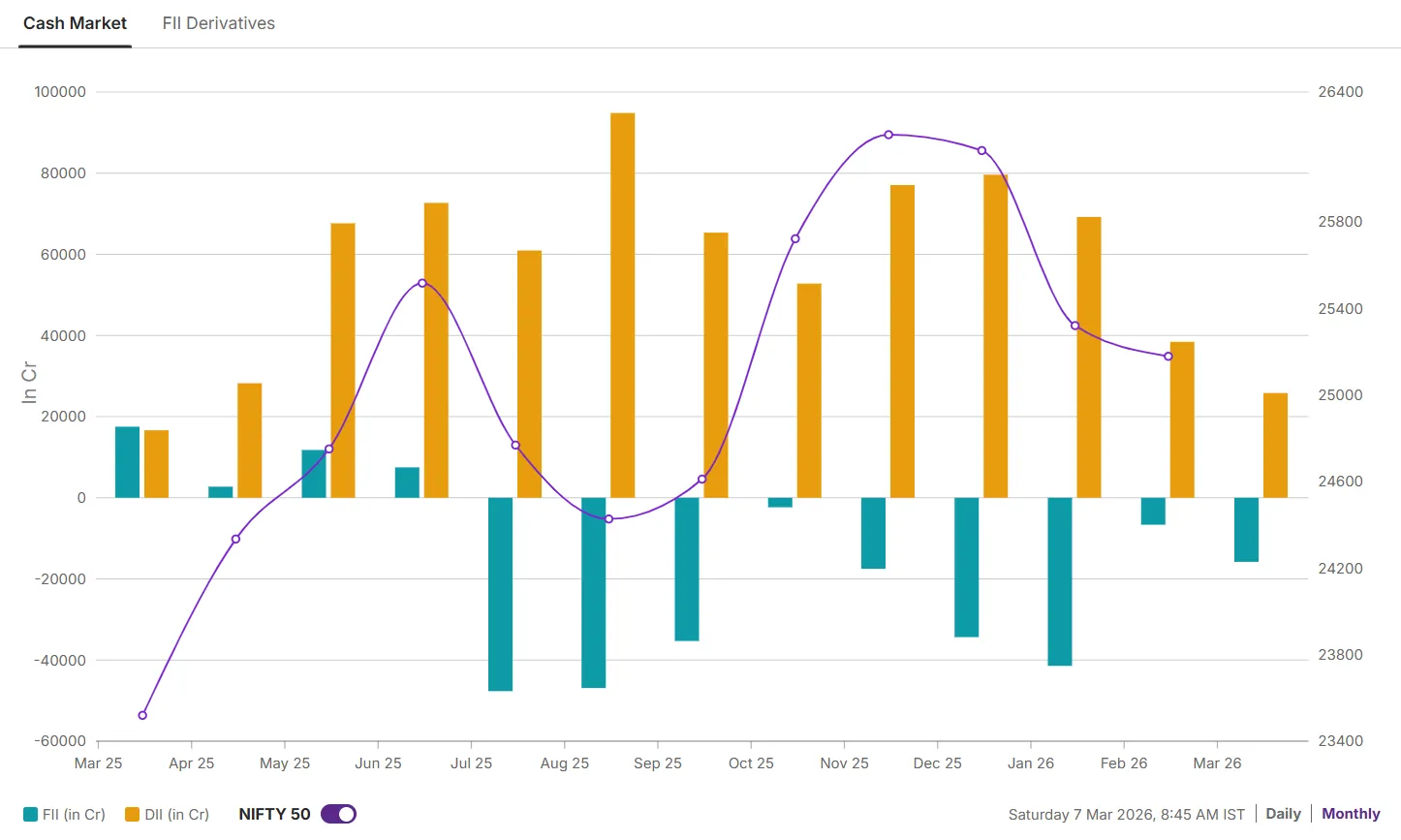

FIIs cash market and derivatives

Foreign institutional investors (FIIs) have begun March on a weak note, offloading equities worth ₹15,800 crore over the last five trading sessions. This selling has already surpassed the total outflows recorded in February and extends the streak of net selling to nine consecutive months, underscoring the persistent cautious stance of FIIs towards Indian equities.

NIFTY50 index outlook

The near-term outlook for NIFTY50 remains cautious, with the index facing selling pressure from crucial resistance zones of all the key exponential moving averages. The immediate support for the index is around 24,300–24,400 zone. A decisive break below this level could open the door for further downside toward 23,800. On the upside, 24,800–25,000 will act as an immediate resistance band, and only a sustained move above this zone can revive short-term momentum. Given the high volatility, short-term traders are advised to take a cautious approach instead of a aggressive directional setup.

Disclaimer:

Derivatives trading must be done only by traders who fully understand the risks associated with them and strictly apply risk mechanisms like stop-losses. The information is only for consumption by the client, and such material should not be redistributed. We do not recommend any particular stock, securities, or trading strategies. The securities quoted are exemplary and not recommendatory. The stock names mentioned in this article are purely to show how to do analysis. Make your own decision before investing.

About The Author

Next Story