Market News

US-Iran deal, Fed meeting, Crude oil prices, FIIs activity among key market triggers to watch this week

.png)

4 min read | Updated on June 14, 2026, 10:59 IST

SUMMARY

Indian markets enter the week of June 15 on a cautiously positive note after NIFTY50 and Sensex snapped a two-week losing streak. The recovery was led by strong gains in banking stocks, while IT, metal and energy remained under pressure. The key focus this week will be on the US-Iran peace deal, India WPI inflation, the U.S. Fed decision, Bank of Japan policy, crude oil movement and FII flows.

So far in June 2026, FIIs have sold equities worth nearly ₹46,430 crore keeping pressure on the domestic markets. | Image: Shutterstock

Indian markets ended the week with modest gains, boosted by a sharp rally on Friday. The NIFTY50 closed at 23,622, marking an increase of almost 1.1% over the course of the week, while SENSEX finished at 75,527. Friday’s rally was driven by hopes of a peace deal between the US and Iran, a fall in the price of Brent crude towards $87 per barrel, and improved global sentiment.

The sectoral trend was mixed. Private banks led the recovery with a 5% gain, followed by PSU banks, which rose 3.2%. On the other hand, IT, Metal and Energy stocks remained under pressure, limiting the overall market upside.

As markets enter the week of June 15, the focus will remain on the US-Iran peace deal, global central bank decisions, crude oil movement, rupee weakness and FII flows. The key question now is whether NIFTY50 can build on Friday’s recovery and sustain above its short-term moving averages.

Banking stocks were the biggest support for the market recovery last week. The Bank NIFTY surged nearly 3% on Friday, with all 14 constituents ending in the green. The strength came as lower crude oil prices and easing geopolitical tensions improved risk appetite. Banks usually benefit when crude cools off because it reduces pressure on inflation, bond yields and the rupee. This also improves sentiment for domestic-facing sectors. AU Small Finance Bank led the gains with a 5.7% rise, followed by IDFC First Bank, which gained 5.6%.

India’s May Whole Sale inflation (WPI) data will be in focus this week after it jumped to 8.3% in April, the highest level in nearly three-and-a-half years. The May reading will be important because another sharp rise in WPI can keep inflation concerns alive.

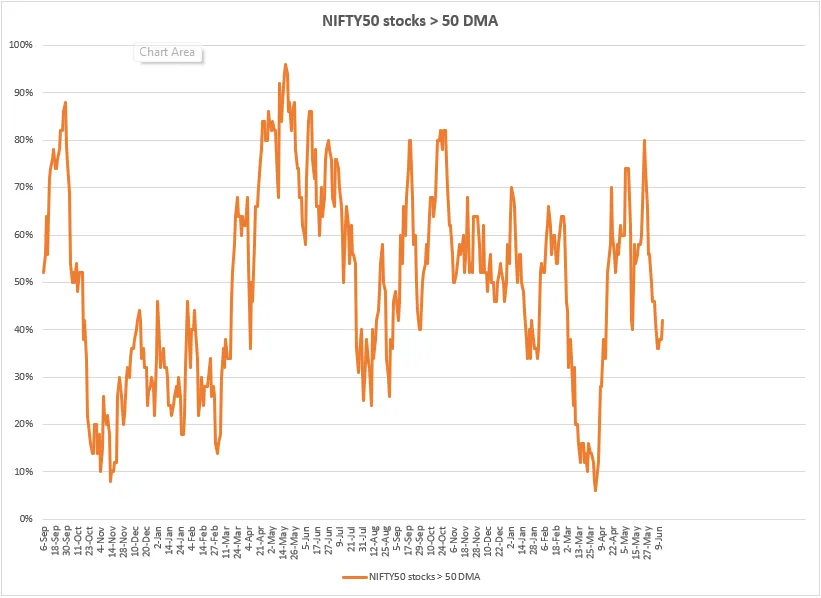

Market breadth

Market breadth weakened despite the headline recovery in NIFTY50. The share of NIFTY50 stocks trading above their 50-day moving average has slipped from nearly 80% in early May to around 40% now. This shows that participation has narrowed sharply. The index recovery is being driven by select heavyweights, especially banks, while many stocks are still struggling to regain short-term momentum.

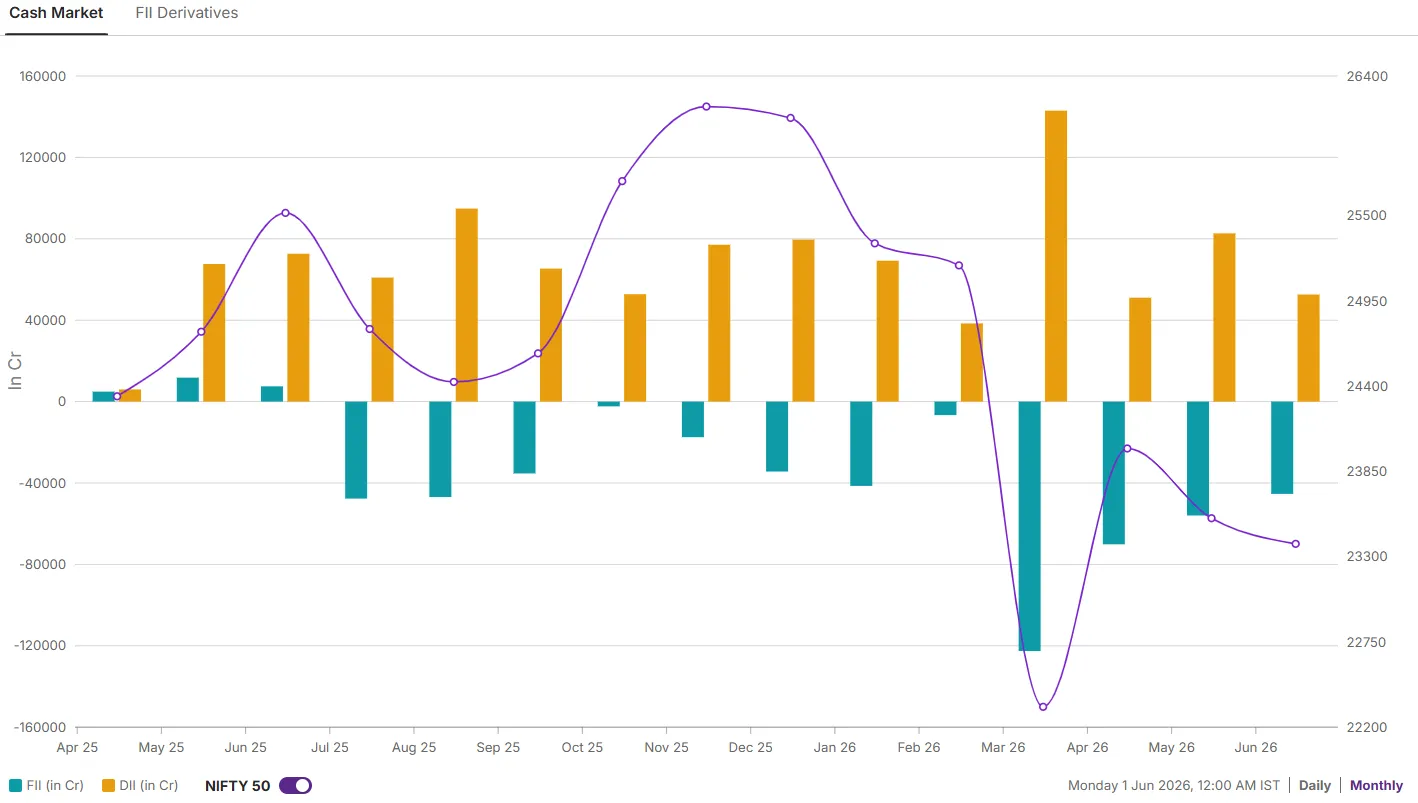

Foreign investors positioning

Foreign investors remain net sellers in the cash market for the third straight month. In June so far, FIIs have sold equities worth nearly ₹46,430 crore, keeping pressure on the market despite Friday’s recovery. Domestic institutional investors continued to provide support.DIIs bought shares worth more than ₹50,000 crore in June so far, helping absorb part of the FII selling pressure.

NIFTY50 outlook

The NIFTY50 ended the week on a stronger note after reclaiming its 20-day EMA. This is an important short-term signal because the index had remained below this moving average for several sessions, showing weak momentum earlier. For the week ahead, the 20-day EMA will be the key level to watch. If NIFTY50 sustains above this zone, the recovery can extend towards 23,750–23,820 first. A move above this resistance band can open the path towards 24,000.

Disclaimer:

Derivatives trading must be done only by traders who fully understand the risks associated with them and strictly apply risk mechanisms like stop-losses. We do not recommend any particular stock, securities, or trading strategies. The securities quoted are exemplary and not recommendatory. The stock names mentioned in this article are purely to show how to do analysis.

Related News

About The Author

Next Story