Market News

Paytm Q4: Firm swings to ₹184 crore profit, flags PIDF scheme discontinuation impact

4 min read | Updated on May 07, 2026, 08:44 IST

SUMMARY

Paytm Q4 results: For the full fiscal year 2025-26 (FY26), Paytm reported a revenue of ₹8,437 crore, up 22% YoY, while EBITDA came in at ₹502 crore, against the loss of ₹1,506 crore in the previous fiscal.

Stock list

Its revenue from operations in Q4 FY26 came in at ₹2,264 crore, up 18.4% YoY. Image: Shutterstock

Its revenue from operations came in at ₹2,264 crore, up 18.4% against ₹1,912 crore logged in the year-ago period.

The company, in its earnings release, said that the reported numbers for the quarter are impacted by the discontinuation of the PIDF scheme, and the FY 2026 UPI incentive is yet to be finalised. "We were able to achieve our guidance of 30-40% offset of PIDF impact in Q4 FY 2026," the company said.

What was the PIDF scheme?

The Payments Infrastructure Development Fund (PIDF) scheme was an initiative by the Reserve Bank of India (RBI) to boost digital payment infrastructure in smaller towns and rural areas.

The PIDF incentive was aimed at accelerating digital payments infrastructure across Tier-3 to Tier-6 centres, as well as underserved regions including the Northeastern states and the Union Territories of Jammu, Kashmir and Ladakh.

The PIDF scheme was valid until December 31, 2025. For the six months ended September 30, 2025, Paytm recognised ₹128 crore in incentive revenues under the scheme.

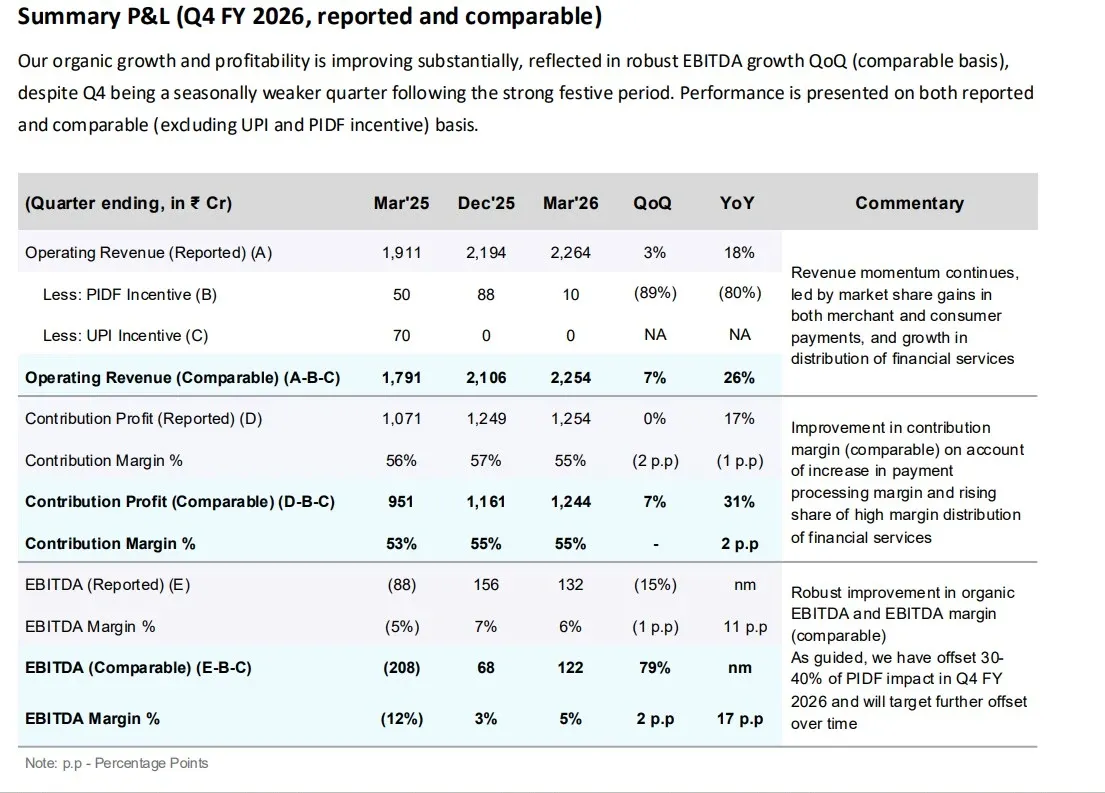

Summary P&L (Q4 FY 2026, reported and comparable)

The company said its organic growth and profitability are improving substantially, reflected in robust EBITDA growth QoQ (on a comparable basis), despite Q4 being a seasonally weaker quarter following the strong festive period.

Revenue Performance

-

Reported operating revenue rose to ₹2,264 crore, up 3% QoQ and 18% YoY, indicating sustained growth momentum.

-

Comparable revenue (excluding incentives) stood at ₹2,254 crore, reflecting a 7% QoQ and 26% YoY growth.

However, PIDF incentives declined sharply (down 89% QoQ and 80% YoY), while UPI incentives remained absent, impacting reported numbers.

Revenue momentum continues, led by market share gains in both merchant and consumer payments and growth in the distribution of financial services.

Contribution Profit

-

Reported contribution profit remained stable QoQ at ₹1,254 crore, up 17% YoY.

-

Comparable contribution profit increased to ₹1,244 crore, showing a 7% QoQ and 31% YoY growth.

-

Contribution margin (comparable) improved to 55%, up 2 percentage points YoY, driven by:

EBITDA Performance

-

Reported EBITDA came in at ₹132 crore (down 15% QoQ), impacted by lower incentives.

-

On a comparable basis, EBITDA rose sharply to ₹122 crore, delivering a 79% QoQ improvement.

-

Comparable EBITDA margin improved to 5%, expanding:

+2 percentage points QoQ;

+17 percentage points YoY

Management indicated that 30–40% of the PIDF impact has already been offset in Q4, with further mitigation expected over time.

Note for investors

In its investor FAQ, the company clarified the difference between reported and comparable numbers and which metric investors should rely on.

It noted that comparable figures exclude the PIDF incentive (₹10 crore in Q4 FY2026 versus ₹50 crore in Q4 FY2025, with the scheme discontinued after December 2025) as well as UPI incentives. “Investors should refer to comparable numbers to assess the underlying performance of the business,” the company said.

FY26 financials

For the full fiscal year 2025-26 (FY26), Paytm reported a revenue of ₹8,437 crore, up 22% YoY, while EBITDA came in at ₹502 crore, against the loss of ₹1,506 crore in the previous fiscal.

Profit after tax (PAT) for FY26 stood at ₹552 crore against the loss of ₹663 crore in FY25.

Other key details

| No. | Key Highlight | Details |

|---|---|---|

| 1 | Market share gains in merchant & consumer payments | Consumer UPI GTV grew at 2.2x industry levels. Merchant GMV increased 27% YoY, driven by continued product innovation and disciplined execution. |

| 2 | Payment processing margin expansion | Margin expanded to >4 bps, up from earlier guidance of >3 bps, supported by pricing discipline and higher share of profitable MDR-bearing instruments (including credit cards on UPI and EMI offerings). |

| 3 | Financial services distribution scaling up | Revenue reached ₹2,593 crore, growing 52% YoY (₹890 crore increase), highlighting a high-growth, high-margin business segment. |

| 4 | AI-led operating leverage & cost optimization | Growth supported by higher contribution margin, cost discipline, and increasing use of AI across operations, leading to strong operating leverage. |

About The Author

Next Story