Upstox Originals

The weight is over: Pharma’s $100 million slimdown surge

7 min read | Updated on February 11, 2026, 16:25 IST

SUMMARY

India’s weight-loss story is no longer just about gyms and diets; it’s showing up in pharma sales. In five years, it has grown sixfold to cross $100 million in FY25. Rising obesity and diabetes are driving demand, even as high costs limit access. With patent expiries ahead and local manufacturing gearing up, the big question is: can this shift from premium niche to mass-market healthcare story?

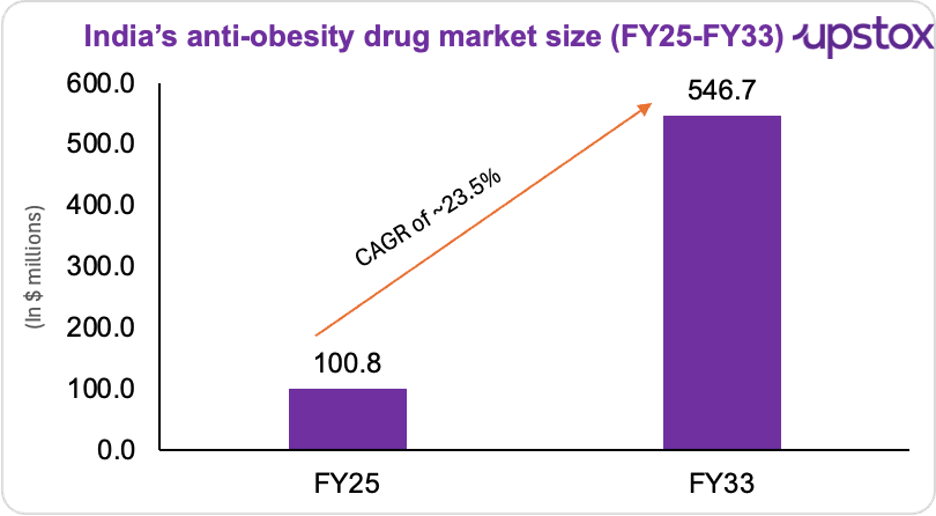

In just five years, India’s medical weight los market the market has grown more than six times

“Health is wealth” applies everywhere. And weight loss, whether driven by health concerns or fitness goals, has steadily moved to the forefront.

The numbers in India’s anti-obesity drug market are beginning to reflect exactly that. In just five years, the market has grown more than six times, increasing from $16 million in 2021 to nearly $100 million today, according to Pharmarack.

It is further expected to grow at a 23.5% CAGR to reach $546.7 million by FY33.

Source: Pharmarack

But this market expansion isn’t happening in isolation. It’s unfolding alongside a growing public health challenge.

We all know how common diabetes has become in India.

Over 77 million adults are already living with the condition. And it’s not just diabetes. Nearly one in four adults in the country is now classified as overweight or obese.

That’s the backdrop against which India’s anti-obesity drug market is expanding. New weight-loss medicines like Ozempic and other GLP-1 therapies are gaining visibility.

Demand is pushing the market into the mainstream

Right now, one name dominates India’s anti-obesity drug market: Novo Nordisk. Its semaglutide-based brands are leading the charge. These GLP-1 therapies; a newer class of medicines that regulate blood sugar and suppress appetite; have quickly become central to modern obesity treatment.

Take Rybelsus. Since its launch in 2022, it has grown to command nearly two-thirds of the market. That’s not gradual adoption. That’s rapid acceptance; from both doctors and patients.

And then came Mounjaro, developed by Eli Lilly. Launched earlier in 2025, it climbed to become India’s second bestselling branded drug by September the same year.

Why is demand exploding?

Rising obesity and lifestyle diseases

According to the National Family Health Survey-5 (2021), 24% of Indian women and 23% of men are overweight or obese; roughly one in four adults. And obesity rarely comes alone. It is closely linked to diabetes, heart disease, and metabolic disorders that require long-term management, not one-time treatment.

That’s the structural backdrop.

Kirti Ganorkar, Managing Director of Sun Pharma, highlighted this shift toward chronic care, noting that rising lifestyle diseases demand “patient-focused solutions.” He also indicated that improving access to GLP-1 therapies could significantly reduce the long-term burden of obesity and diabetes.

GLP-1 drugs go beyond diabetes

Originally developed for diabetes, GLP-1 therapies reduce appetite, slow digestion, and drive sustained weight loss. They’re now moving beyond endocrinology clinics into mainstream chronic-care discussions.

Winselow Tucker, President of Eli Lilly India, calls this a transformative phase in obesity care, driven by better diagnosis, awareness, and access to evidence-based treatments. The only problem? GLP-1 drugs are still expensive.

| GLP-1 Drug | Price (per month) | Annual cost |

|---|---|---|

| Wegovy (semaglutide) | ₹17,000-₹26,000 | ₹2.0 - ₹3.1 lakh |

| Rybelsus (oral semaglutide) | ₹10,000 | ₹1.2 lakh |

| Mounjaro (tirzepatide) | ₹14,000-₹17,500 | ₹1.7 - ₹2.1 lakh |

| Ozempic (semaglutide) | ₹10,000 | ₹1.2 lakh |

Source: News articles

With annual costs between ₹1.2 lakh and ₹3 lakh, GLP-1 therapies are priced at or above India’s per capita income of ~₹1.7 lakh. That keeps adoption largely confined to higher-income urban patients, even though obesity and diabetes cut across income groups. Yet demand remains strong. Rybelsus makes up nearly two-thirds of sales, and the quick uptake of Mounjaro after its 2025 launch signals clear willingness to pay.

What happens next?

That equation could change soon.

Semaglutide is set to go off patent in India in 2026; much earlier than in the US. Since Indian patent law doesn’t allow extensions, generic versions could enter the market faster.

That’s a rare setup. India, along with countries like Canada and Brazil, may see affordable generics years before the US does. Pharmarack’s VP Sheetal Sapale notes that nearly a dozen Indian pharma companies already have generic oral semaglutide ready. If prices fall, access could widen beyond metro cities. But doctors warn that easier availability without strong regulation could raise misuse risks.

Investment bank Jefferies calls this India’s “magic pill moment,” estimating the domestic semaglutide market alone could touch $1 billion if pricing and adoption align.

Indian pharma companies aren’t waiting.

Dr. Reddy's Laboratories plans a phased rollout of 15 GLP-1 products. Sun Pharma is developing its own GLP-1 candidate, Utreglutide. Cipla and Lupin are positioning for generic launches in 2026 and emerging markets.

A global gold rush and an investor signal

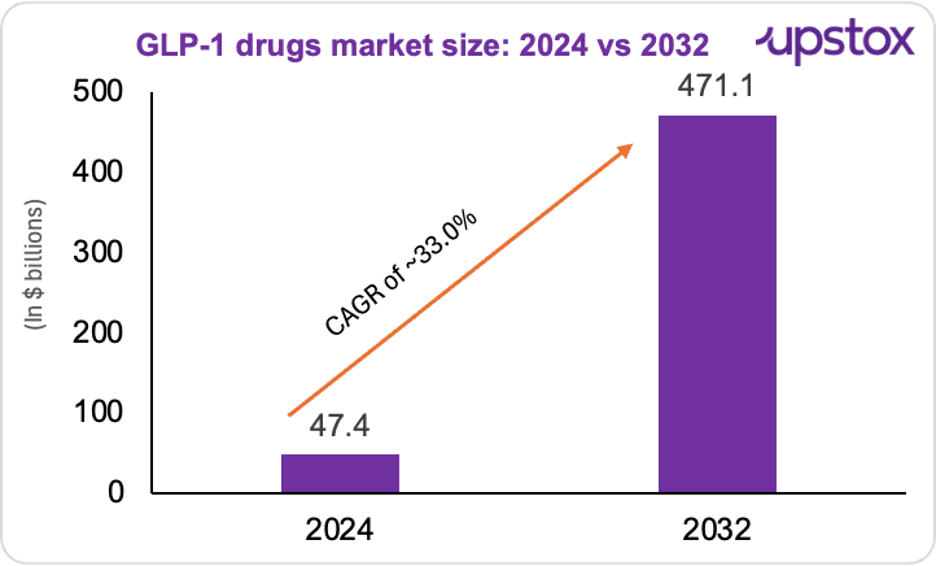

According to a growth forecast report by MarketsandMarketsTM, GLP‑1 drugs are set to grow from $47.4 billion in 2024 to $471.1 billion by 2032. Almost 10 times bigger in less than 10 years. Goldman Sachs says that just the obesity side of this market is worth $95 billion.

Source: MarketsandMarkets

Globally, the money is already flowing. Eli Lilly reported $19.3 billion in revenue in Q4 2025, up 43% year-on-year, driven largely by demand for Mounjaro and Zepbound. The company expects full-year 2026 revenue of $80–83 billion.

In the US, GLP-1 drugs are now the fastest-growing category in pharma spending. The segment already generates over $50 billion annually, and analysts expect it to expand to $150–200 billion by the early 2030s.

India, by comparison, is still tiny.

The domestic GLP-1 and anti-obesity market currently stands at just $75–100 million a year. But projections suggest it could scale to $3–4 billion by 2032; implying growth well above global averages.

The gap between where India stands today and where it could go underscores one thing: this is still an early-stage market, with long-term upside tied to falling prices, wider access, and local manufacturing.

So what’s driving this global weight-loss surge?

The global weight-loss supplements market alone was valued at $7.48 billion in 2025 and is expected to rise to $8.65 billion in 2026. That’s steady, demand-backed expansion. Why? Because the world is becoming heavier; and more medically aware at the same time.

As obesity-linked risks like diabetes and heart disease rise, weight management is shifting from cosmetic concern to clinical priority. GLP-1 therapies are delivering stronger results, boosting doctor confidence and patient interest. Regulatory approvals and retail access are pushing the category into mainstream care.

India is following the same trajectory; just on a smaller base.

Digital distribution and India as a supply hub

Access is widening, thanks to digital.

Online pharmacies are pushing GLP-1 drugs into Tier II and III cities, where advanced therapies were earlier hard to find. According to Pharmarack, India’s anti-obesity market has crossed ₹600 crore in MAT; five times its size five years ago. Semaglutide holds over 60% share, while tirzepatide is gaining ground.

Meanwhile, India is gearing up as a supply hub. With patents expiring in 2026, players like Dr. Reddy's Laboratories, Sun Pharma, Cipla, Lupin, Biocon, and Zydus Lifesciences are scaling their GLP-1 pipelines.

Digital reach at home. Manufacturing scale globally.

In summary

India’s GLP-1 story is still early. High prices may slow adoption for now, but patent expiries, digital reach, and pharma’s pivot toward GLP-1s create strong long-term tailwinds. As evidence expands beyond weight loss to heart, kidney, and metabolic benefits, demand could deepen. The real opportunity? Expand access at home... and scale up as a global manufacturing hub for GLP-1 therapies.

About The Author

Next Story