Upstox Originals

The curious case of the Chinese stock market

6 min read | Updated on March 16, 2026, 17:59 IST

SUMMARY

Indian markets have risen almost 10x, since the lows of 2008. If you were asked to guess the same for the Chinese equity markets, what would the answer be? Think about it. Would it surprise you to learn that the Chinese markets have not yet recovered their 2008 (yes, that’s correct) highs! What are some key reasons for this? Is there a systemic slowdown or fundamental shift in the country? Keep reading to find out.

The Chinese stock market, has yet to reach its 2008 highs | Image: Shutterstock

As a student of finance or economics, if someone showed you the following facts about a country, what do you think would be a logical conclusion about the country’s stock markets?

| Particulars | 2008 | Recent* |

|---|---|---|

| GDP (Nominal) | $4.6 Trillion | $19-20 Trillion |

| GDP per Capita | $3,500 | $14,500 |

| Total Trade (Goods) | $2.6 Trillion | $6.0 Trillion |

| Inflation (CPI) | 5.9% | 1.3% |

| Foreign Exchange Reserves | $2.0 Trillion | $3.5 Trillion |

Source: World Bank, IMF, Government data; *Most recent available data

Now, if you were told the country in question is China. The second-largest economy in the world, a hub for EVs, semiconductors, and a country with one of the strongest infrastructures.

Would it be a safe assumption that since 2008, the markets have made new highs?

Well, let’s take a look.

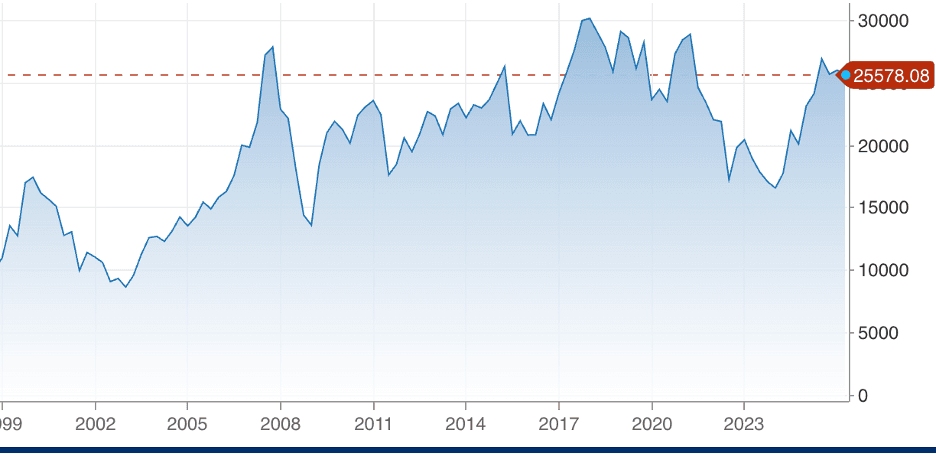

Shanghai Stock Exchange

Source: CNBC; Data as of March 11, 2026

Hong Kong Stock Exchange (Hang Sang Index)

Source: CNBC; Data as of March 11, 2026

When you look at the two charts above,

- Since 2008 (almost 18 years), the Shanghai Stock Exchange has never sustainably reached its 2008 high

- Similarly, the Hang Sang Index has struggled to reach and retain its 2008 high

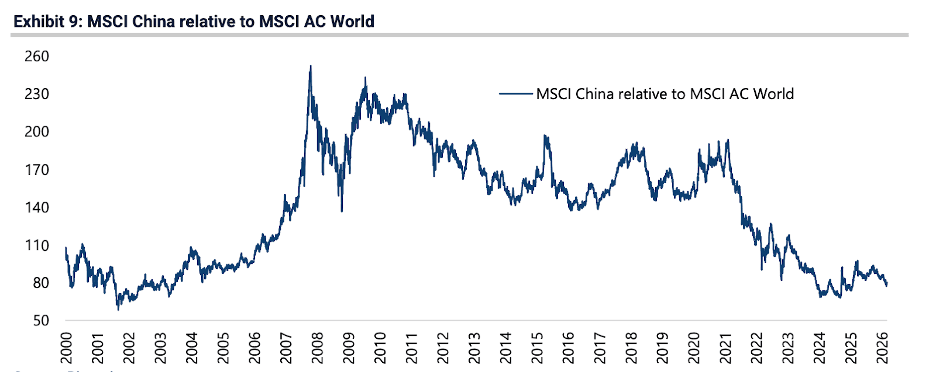

Not only that, the MSCI China Index, which significantly outperformed the MSCI World Index in the early 2000s, has since seen the outperformance deteriorate and finally transition to underperformance (below 100) in the last few years.

Source: GREED & Fear report dated March 12, 2026

Let’s explore some key reasons why the Chinese equity markets have had almost two decades of stagnant performance.

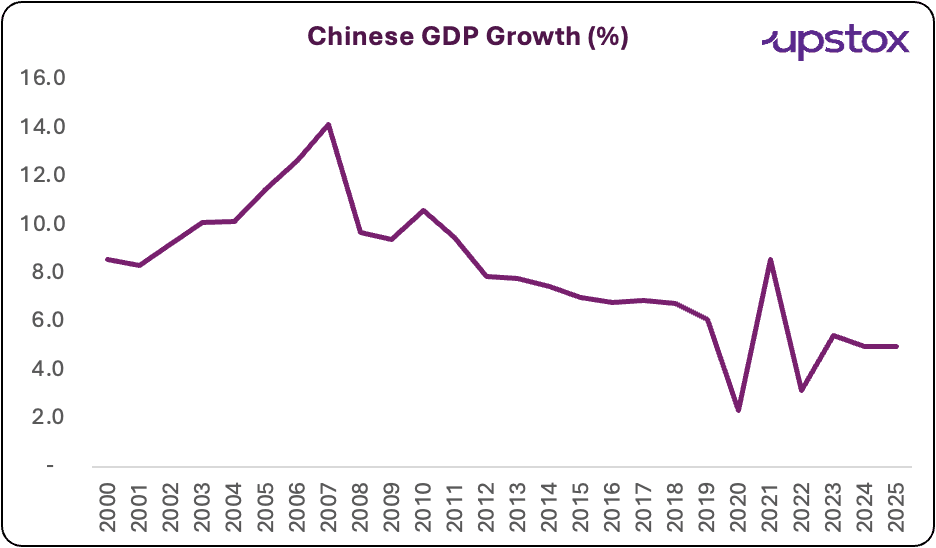

Weakening GDP growth

China's GDP growth rate has slowed from the highs of 10% in the 2000s to under 5% in 2025. In fact, for 2026, China has set a target of 4.5-5%, the lowest since 1991.

Source: World Bank

The robust growth of the 2000s was driven by two factors: 1) a strong focus on infrastructure spending (mainly real estate) and 2) a rise in exports. China became (and still is) the factory to the world. From clothes, toys, and cell phones, most day-to-day use items had their origin in China.

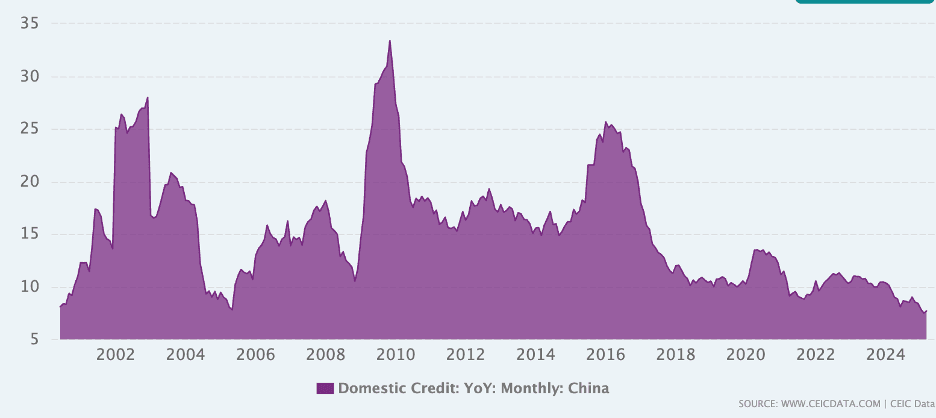

That said, the focus on infrastructure and real estate has led to overcapacity. We are all aware of the famed ghost cities and towns in the country —places with fancy buildings and smooth roads but almost no inhabitants. Consequently, both domestic credit growth and industrial growth, two vital pillars of economic growth, started to moderate.

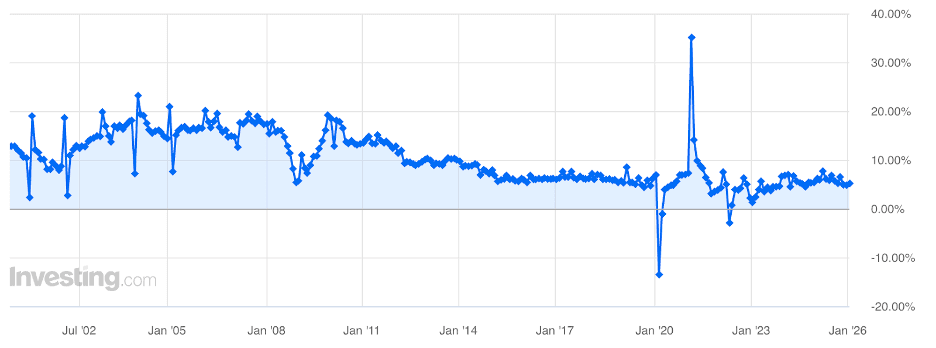

China Industrial Production YoY

Source: Investing.in, Data as of March 11, 2026

China’s credit growth

Source: CEIC, Data as of March 11, 2026

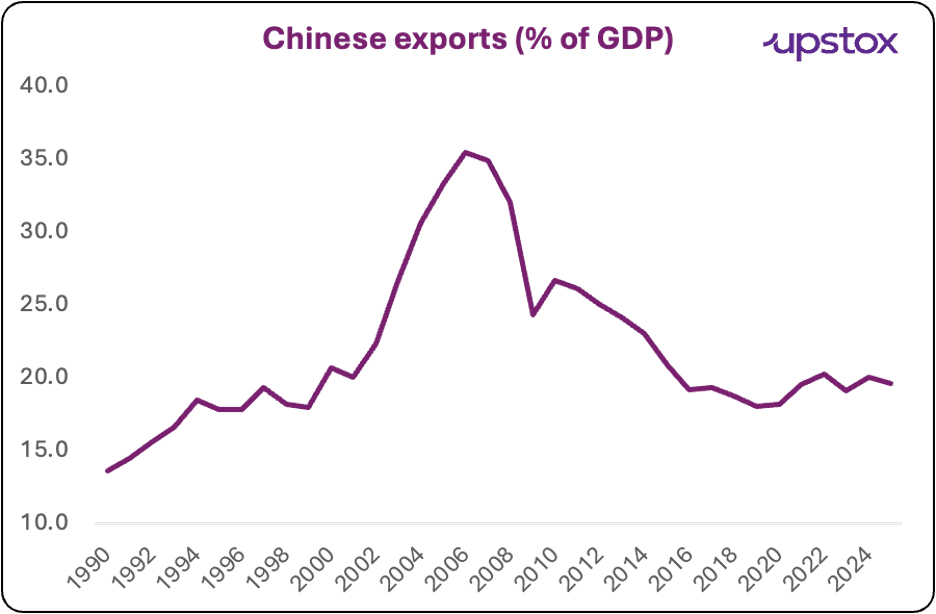

Second, since the Global Financial Crisis, China has progressively pivoted its focus within the country. Consequently, exports have been taking a backseat, as seen in the chart below.

Source: Federal Reserve Bank of St. Louis

Further, China also had a problem of low productivity. A 2018 study by Zhang, Zhang & Zhao found that Chinese state-owned companies, which control a large pool or resources, had a much lower R&D productivity than their private counterparts. As such, not only did exports stagnant but overall economic productivity also took a knock, further hurting the economy.

Weak consumption

While there is definitely merit in savings (if people are not consuming, they are saving), if they are not channeled towards industrial and credit growth are not productive for economic growth.

Real estate oversupply

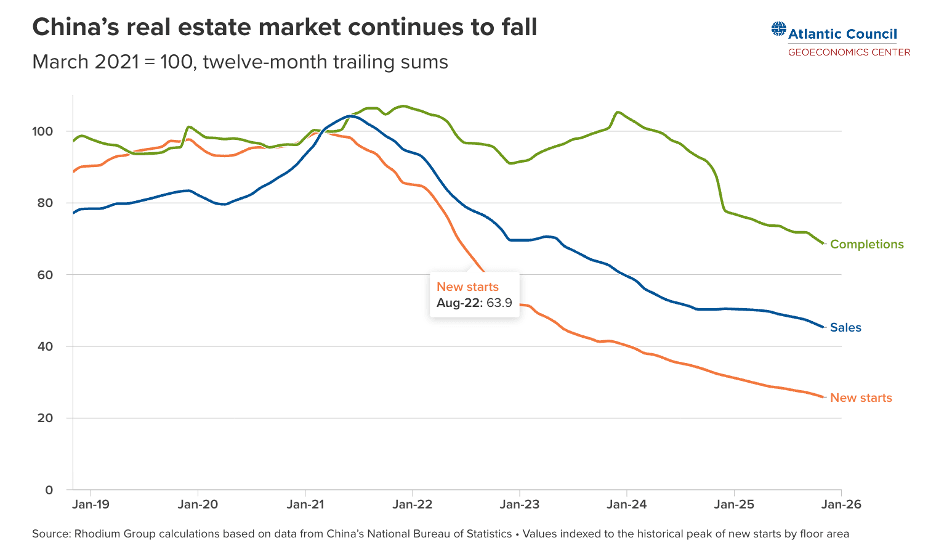

Roughly 70% of Chinese household wealth was tied up in real estate (compared to ~30% in the US). China’s "Three Red Lines" policy was introduced in 2020 to deleverage developers like Evergrande. This began a long slump in the Chinese real estate market, which entered its fifth year in 2026. Once again, while the government’s intention was to contain the contagion, it didn't just stop construction but broke the investor trust.

Source: Atlantic Council

Tech crackdown

Ant Group, an affiliate of the Chinese conglomerate Alibaba, planned an IPO in October 2020 to raise $34.5 billion. This would have been one of the largest IPOs in history, valuing the company at $313 billion. However, a crackdown by Chinese authorities forced its founder Jack Ma to cancel the IPO plan. In 2021, the Chinese government further intensified its scrutiny of tech companies, including Tencent and DiDi.

Back then, there were at least 248 Chinese companies listed on three major US exchanges with a total market capitalisation of $2.1 trillion, according to the US-China Economic and Security Review Commission. The Chinese crackdown weighed heavily on these companies.

Not only did it adversely impact the business, but it also hurt investor confidence, which has not completely recovered.

Financial crackdown

Parallel to the tech crackdown came the government’s scrutiny of financial institutions. Dozens of financial officials and banking executives were investigated or detained, with over 90 targeted in 2024 alone. High-profile cases include that of Fan Yifei, the former vice-governor of the People's Bank of China.

The government believed that the sector prioritised short-term profitability over long-term goals. The crackdown is intended to change that, bringing focus back to sectors like manufacturing.

American tussle

Since 2016, the Chinese government has been consistently entangled in a tussle with the US. Leaving aside the politics, China has consistently been a target of American protectionist policies. While China has steadily been working towards reducing its reliance on the US, from a market point of view, America still houses the largest investor pool. Western institutional investors (pension funds and endowments) have undergone a massive "de-risking" or "China-Free" allocation strategy. Hong Kong, being the most liquid and accessible portal for this capital, bore the brunt of the selling.

Sector composition is important too

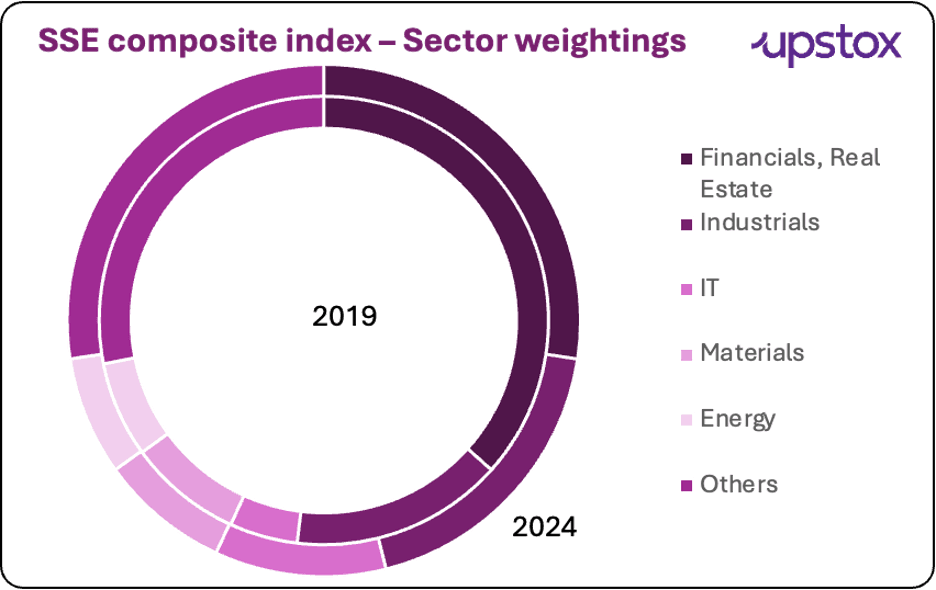

The Shanghai Stock Exchange Composite Index is predominantly composed of Industrials, financials and real estate companies. A large share of this onshore market cap is composed of state-owned enterprises (SOEs). Besides the real estate meltdown mentioned above, these sectors are investment-heavy with long gestation periods, impacting returns.

SSE Composite Index: Sectoral composition

Sources: Sibil Research

Before you go

There is no doubt that China is making great strides in the field of electric vehicles, semiconductors, and AI—areas which are likely to power the future. However, a holistic overhaul of the economy has definitely weighed on the financial markets.

About The Author

Next Story