Upstox Originals

Decoding India's mall paradox

6 min read | Updated on February 27, 2026, 12:49 IST

SUMMARY

In times when people can order everything online, malls and street stores (yes, the shopping ones) are thriving, but not evenly. Leasing is at a three-year high, and premium Grade-A malls’ occupancy is near 100%. Investors, meanwhile, are lining up, with $3.5 billion+ in capital inflows expected. But if things are so great, why are there reports that nearly 20% of India’s total malls are “ghost assets”? Read on

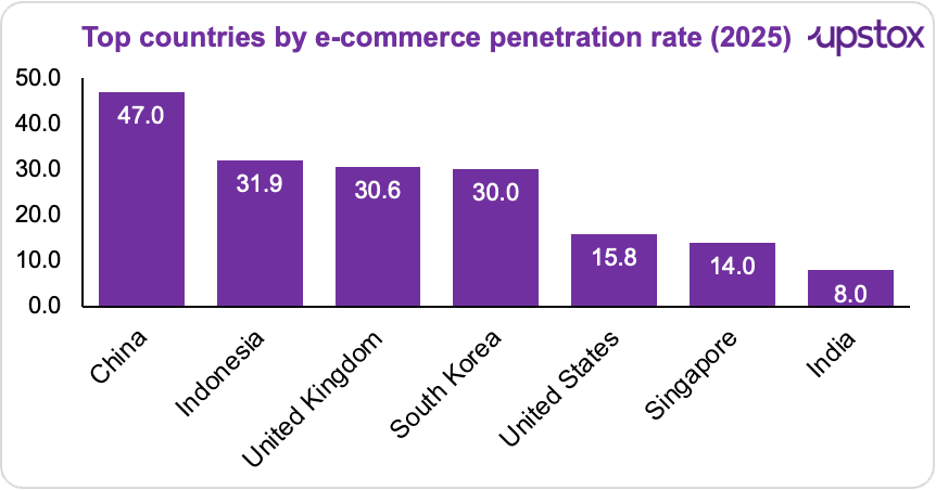

Online retail penetration in India is still only ~8%, compared with 20%+ in developed markets

There was a time when shopping malls had a clear purpose.

They were places you went to buy things. That was it.

Then e-commerce showed up. Convenience improved. Choices exploded. And it was easy to assume that, the mall’s original job was slowly losing relevance.

But today’s story about malls takes a different turn.

What? You see, leasing is picking up. Vacancies are tightening. And rents in top-grade assets are holding firm.

What the numbers are saying:

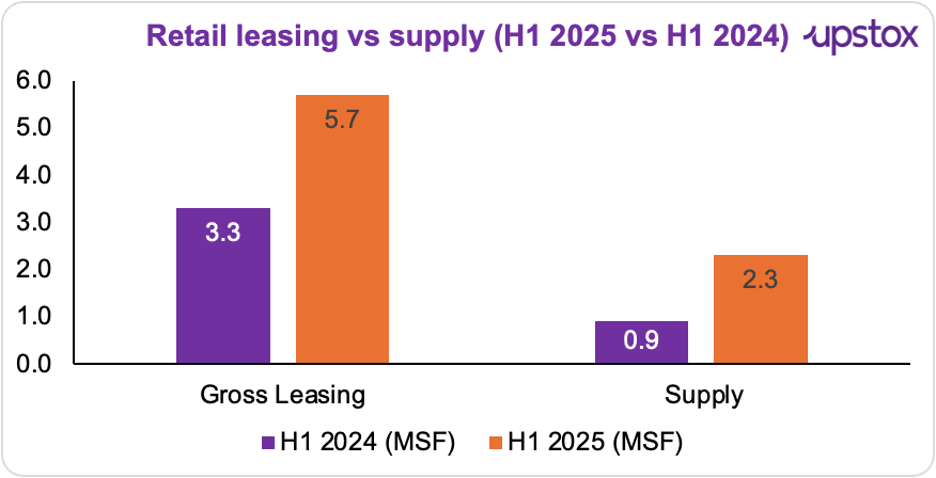

Leasing jumped in H1 2025. India’s top seven cities saw 5.7 million sq. ft. of retail space leased in Jan–June 2025, a 69% YoY increase. Supply also picked up. New retail completions rose to 2.3 million sq. ft. in H1 2025, up 165% YoY.

Source: JLL

Demand is still ahead. On a full-year basis, gross retail leasing reached 12.5 million sq. ft. in 2025, a 54% YoY increase and the highest level in the past three years. Occupancy tells the same story. Premium Grade-A malls are running at 95–100% occupancy, while overall mall vacancy has fallen from 15.4% in 2019 to about 8.1% in 2024.

But here’s a thing. While institutional grade-A (premium) malls are thriving, not every mall in India is seeing the same level of traction.

According to the latest Knight Frank India report, nearly 20% of India’s total malls are classified as “ghost assets.” Of the 365 malls surveyed across 32 cities, 74 have vacancy levels exceeding 40%, despite being operational for more than three years.

The concentration is notable. West India alone accounts for 44% of these ghost malls. This distress is concentrated in the West and South, which together hold 77% of these underperforming properties, largely due to older, outdated inventory.

As a result, leasing activity has effectively decoupled, focusing entirely on newer, premium, experience-led developments.

Why are India’s premium malls booming?

Brands are rushing in

This boom starts with brands.

Importantly, entering India does not mean all brands are going fully offline. However, most international brands still require a physical presence in malls; whether through flagship stores, limited rollouts, or shop-in-shop formats; to build visibility, acquire customers, and support omnichannel growth.

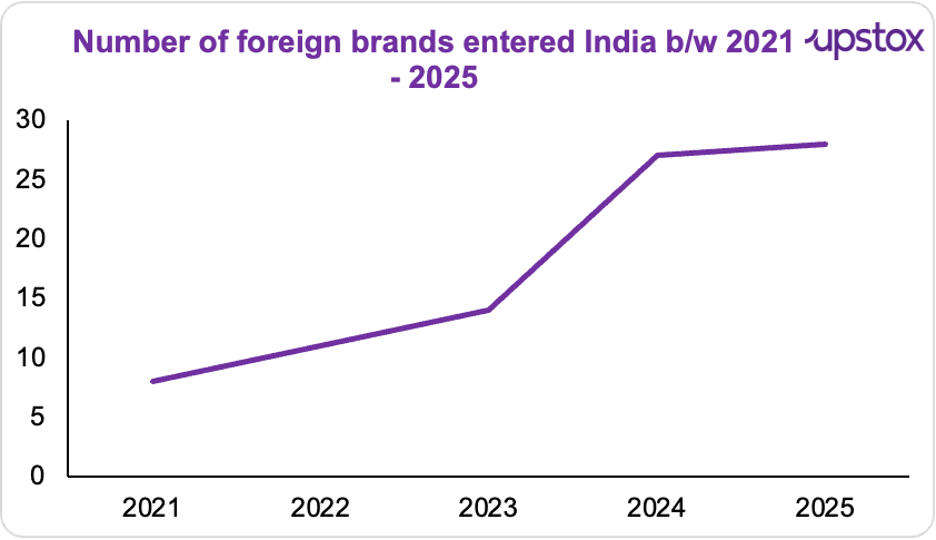

This has translated into higher demand for quality mall space, particularly in top cities. In 2025 alone, 29 new international brands entered India, adding to the pipeline of brands competing for space in well-located malls.

Source: Anarock

D2C brands expand offline footprint

Another shift is easy to miss, but hard to ignore.

D2C brands are going offline.

During the year, online-first brands aggressively expanded their physical presence, together leasing around 0.9 million sq. ft. of retail space. And while global names grab headlines, it’s domestic retailers doing most of the heavy lifting; accounting for 82% of total retail leasing in 2025.

This shift is visible at the brand level. Nykaa added 19 beauty stores in the July–September FY26 quarter, taking its total store count to 265. Other online-first brands such as Giva, The Souled Store, and Snitch have also expanded their offline presence to improve visibility and customer reach.

The shift to phygital retail

E-commerce hasn’t killed Indian malls.

It’s merged with them. Despite rapid digital adoption, online retail penetration in India remains limited at around 8%. Instead of replacing stores, digital has pushed brands toward phygital models; where online discovery meets offline purchase..

Source: News articles

Rising consumption

All of this works because India is turning into a consumption powerhouse.

Consumption already makes up 56% of India’s GDP and is growing at the fastest pace globally. According to a report by Angel One and Iconic Asset, India’s consumption is projected to double by 2034, putting it on track to outpace major economies. Demographics seal the trend. India has more Gen Z consumers than the entire population of the United States, and by 2035, every second rupee spent in India is expected to come from a Gen Zer.

That’s why India is projected to become a $6 trillion consumption economy by 2030. Malls function as mixed-use consumption hubs, with food, beverages, and entertainment already accounting for 30–35% of total footfalls.

The returns that keep capital coming

Grade-A malls in India offer strong and relatively stable returns (around 14–18%), they attract a lot of interest from investors and developers. These returns are supported by rising rents, revenue-sharing with brands, and very low vacancy levels, which make malls a dependable income-generating asset. As more capital flows into this space, developers are encouraged to build better and larger malls; adding momentum to the overall mall boom.

But is this a demand–supply mismatch?

Supply is picking up, but the concern hasn’t gone away. India still has very little organised retail space relative to its population. Even in Tier 1 cities, retail space works out to only 4–6 sq. ft. per person. In Tier 2 and Tier 3 cities, this falls further to 2–3 sq. ft. per person.

The shortage becomes more visible when looking only at premium assets. Grade-A mall space is just 0.6 sq. ft. per person in India. In comparison, the United States averages close to 23 sq. ft. per person, while China sits above 6 sq. ft. per person.

This gap explains why industry leaders believe supply constraints remain, even as new retail space is added.

Over the last decade, India’s per-capita income has significantly increased. Demand showed up quickly. Supply didn’t. As Kejriwal explains, this has created a demand–supply mismatch that’s virtually unheard of in global retail.

You can see it everywhere, Grade-A malls are running at 95–100% occupancy.

In a nutshell

Despite the boom of e-commerce, consumers still remain partial towards physical purchase. Overall, Indian demand still remains robust, and consumers willingness to pay is on the rise. That said. India’s mall story today is less about a broad-based boom and more about a clear split in the market. Strong demand, rising consumption, and steady investor interest are powering premium, Grade-A malls, while weaker assets struggle to stay relevant.

About The Author

Next Story