Upstox Originals

INR at 93.3 against USD! How is the RBI responding?

5 min read | Updated on March 20, 2026, 16:47 IST

SUMMARY

With the rupee now hovering around ₹93.34 (vs the dollar) and 10-year bond yields climbing past 6.7%, India’s markets are feeling the full heat of West Asian tensions. The RBI has already swung into action, stepping in across currency, bond, and liquidity markets to keep volatility in check.

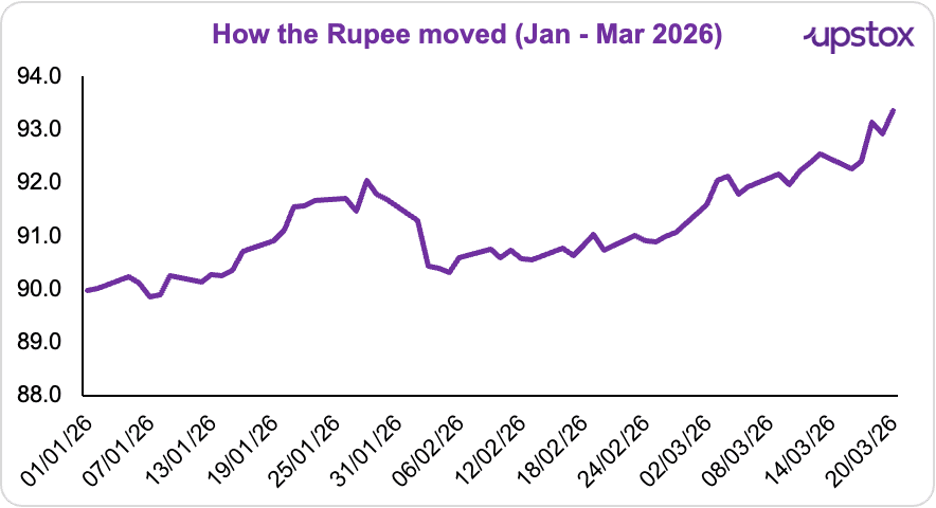

From late Feb 2026 to Mar 20, the Indian rupee slid from ₹91.02/$ to ₹93.34/$ | Image: Shutterstock

Oil is nearing $100. And for a country like India that imports over 85% of its crude, that’s a problem. Higher oil prices can push up inflation, and in turn, pressure both the rupee and bond yields.

The Rupee was the worst-performing Asian currency in 2025. Renewed stress from West Asia has put pressure on it again.

From late Feb, 2026 (marking the start of tensions) to Mar 20, the Indian rupee slid from ₹91.02/$ to ₹93.34/$, a depreciation of about 2.55%.

Source: Investing.com

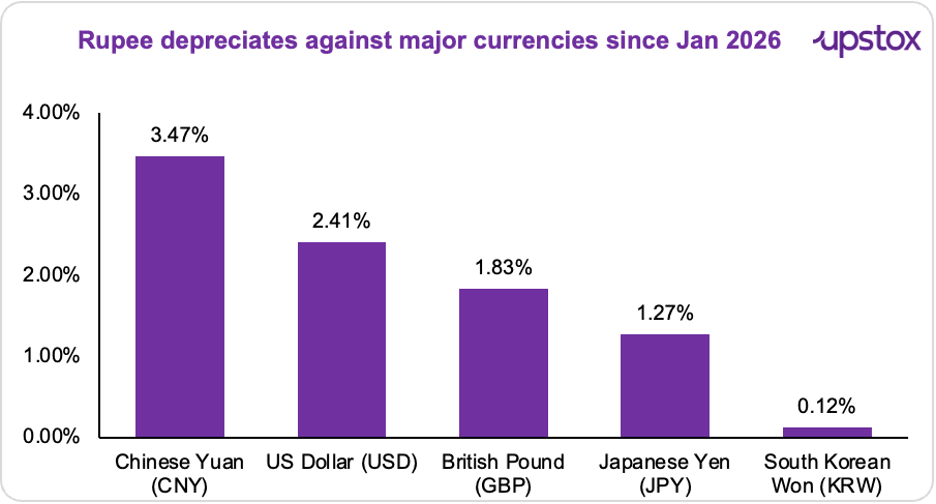

And the weakness isn’t limited to the dollar; it has depreciated against most major currencies since the start of 2026. Here’s a quick look at its slide from January to March 10, 2026:

Source: Financial Express *Data as of March 10, 2026

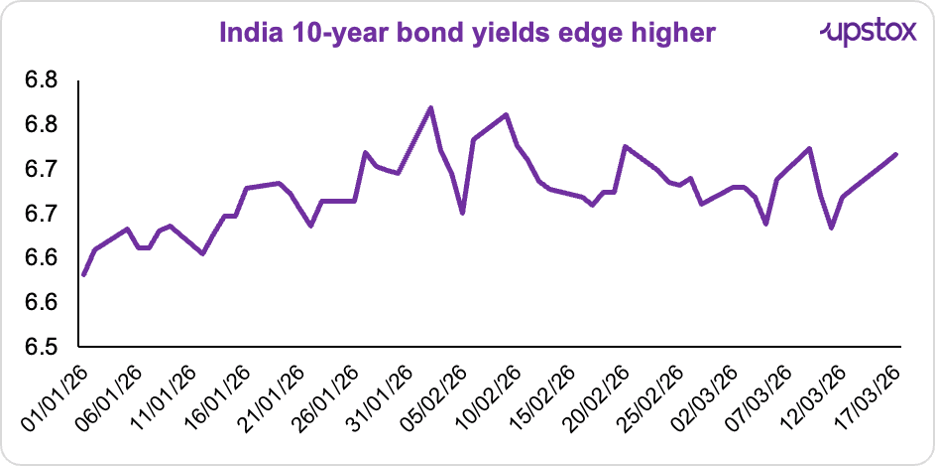

Now, the bond market is reacting too. The benchmark 10-year yield was trading at 6.71% on Mar 17, 2026.

Source: Investing.com

The obvious reason? Oil.

When oil prices rise, India’s import bill goes up, putting pressure on the rupee. On March 18, Brent crude jumped 5.01% to $108.60 per barrel, marking a sharp uptick in oil prices.

At the same time, foreign investors continue to pull money out, selling ₹6,267 crore (Mar 11), ₹10,716 crore (Mar 13), and ₹9,365 crore (Mar 16), as per NSE data.

What has RBI done so far?

The RBI is taking a two-pronged approach to maintain market stability. It is stepping in across both bond and currency markets to contain volatility.

Here’s how that looks in action.

RBI taps forex reserves

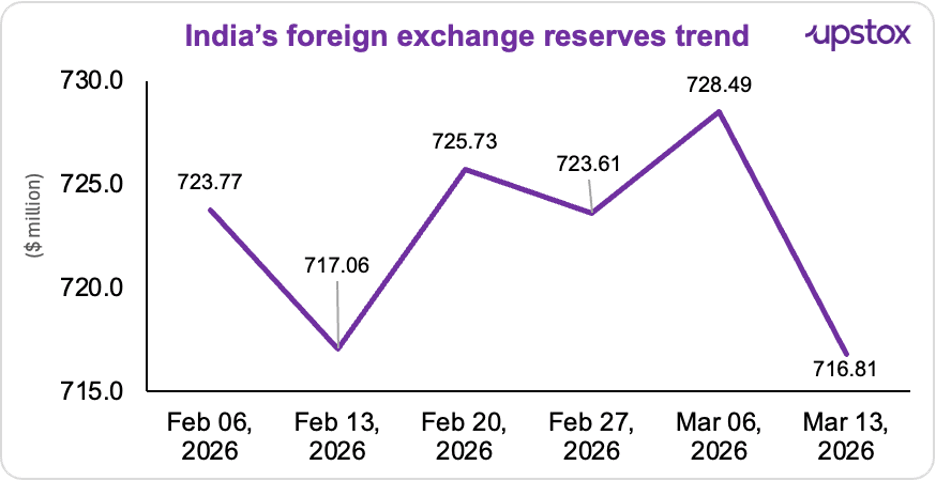

In the week ending March 6, India’s forex reserves fell from $728.49 billion to $716.81 billion, a sharp $11.68 billion drop in just one week.

That’s the steepest decline in over a year.

Now, this isn’t just a random fluctuation.

When the rupee comes under pressure, the RBI typically steps in and sells dollars to stabilise things, and that’s exactly what’s happening here. But the full $11.7 billion drop isn’t purely because of intervention.

According to estimates by IDFC FIRST Bank economist Gaura Sen Gupta, roughly $6.1 billion reflects actual dollar sales by the RBI, while about $5.4 billion came from valuation losses.

India’s reserves include euros, yen and other assets, not just dollars. When the US dollar strengthens, these assets lose value in dollar terms, and the total reserves number automatically falls.

Source: Investing.com

Now, moves of this size don’t happen every week.

Even after adjusting for valuation effects, a $10–12 billion weekly drop is relatively large, and typically coincides with meaningful RBI dollar selling to stabilise the rupee. We’ve only seen similar or bigger moves during periods of stress:

-

November 2024: Reserves plunged $17.8 billion in a week, the largest fall on record (since 1998)

-

October 2008: Reserves dropped around $15.5 billion in a week during the global financial crisis

-

August 2025: Reserves fell to $688.9 billion, a $9.3 billion weekly drop amid tariff-driven uncertainty

Open market operations

The RBI isn’t just defending the rupee. It’s also making sure the bond market doesn’t spiral. Data shows the RBI stepped in aggressively after tensions escalated. In the week following February 28, it net bought bonds worth ₹572.1 billion ($6.2 billion) in the secondary market, helping anchor yields and offset liquidity pressures.

It then doubled down, by announcing ₹1 lakh crore in bond purchases via OMOs, split into two auctions of ₹50,000 crore each.

Both the auctions were completed on March 9 and March 13, respectively. The central bank has already infused ₹3.5 lakh crore into the system through OMO purchases in 2026 so far, including this latest auction.

So, is this a large number?

A good way to gauge that is to look at the last time liquidity conditions were this tight. Back in late 2025, when the banking system slipped into a sharp liquidity deficit, the RBI announced OMO purchases worth ₹2,00,000 crore, conducted in four tranches of ₹50,000 crore each (~$6 billion per tranche) between December 29, 2025 and January 22, 2026.

Now, what are the risks to watch for?

-

States are raising around ₹5 lakh crore via bonds in Q4 FY26, and we’re already in the final stretch of that borrowing cycle. This could worsen the demand–supply imbalance in the bond market, with more bonds chasing limited demand, likely pushing yields higher.

-

Oil is a big import. Every $10 increase in crude adds $12–15 billion to the bill. If prices hit $120, the oil deficit alone could reach ~$220 billion, pushing the current account deficit above 3.1% of GDP.

Outlook

According to various estimates, the rupee is likely to stay under pressure. Goldman Sachs thinks the rupee could slide to 95 against the dollar within a year, if the Iran conflict keeps oil prices elevated.

Others aren’t too far off. HDFC Bank sees USD/INR hovering around 91–93 in the near term, while MUFR Research warns that if oil stays near $100, the rupee could weaken beyond 95.

Which brings us to the RBI.

So far, it’s been selling dollars, buying bonds, and keeping liquidity steady. But if the pressure builds, that may not be enough.

The central bank could step up intervention, or pull in tools like swaps and capital flow measures. And in a more prolonged shock, even rate hikes could come into play to steady the rupee and anchor inflation.

For bonds too, the story is the same, as long as oil stays high and inflation lingers, yields could remain elevated despite RBI’s efforts to keep things stable. For now, one thing is clear, as oil and FPI flows go, so do the rupee and bond markets.

About The Author

Next Story