Upstox Originals

Exploring the potential of the Indian semiconductor industry

.png)

4 min read | Updated on May 09, 2024, 18:49 IST

SUMMARY

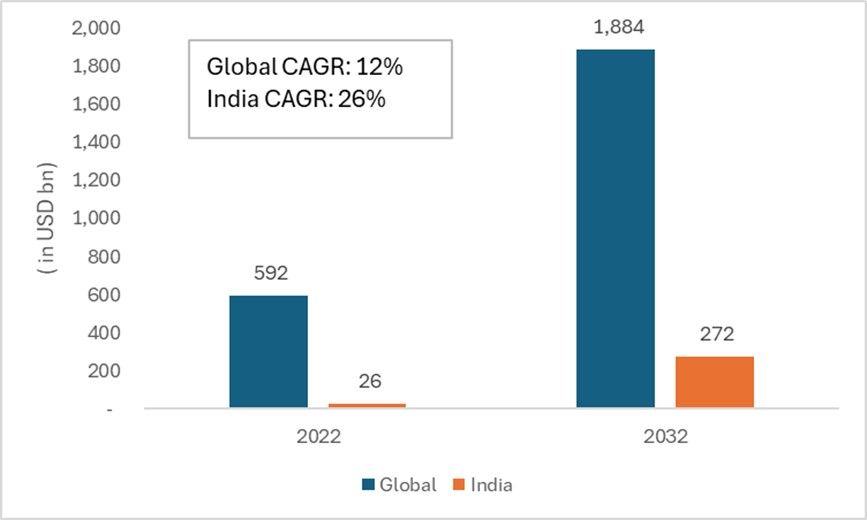

The Indian semiconductor sector is expected to rise ~10x or ~26% CAGR over 2022-2032E to touch ~$270 billion and account for ~14% of the global semiconductor industry. In this article, we explore the various growth drivers of this industry and look at some of the market plays.

The increasing use of electronic equipment across industries is a key driver of semiconductor demand.

Every country is working towards enhancing its semiconductor manufacturing capabilities and ensuring sufficient supplies. But why? Semiconductors are “the brains” behind most modern technological developments (from routers to weapons).

India is also working on the same. In this article, we look at the potential of the semiconductor industry in India, key growth drivers, recent developments and some investment opportunities for investors.

Market size and growth expectations

As seen in the chart below, the Indian semiconductor industry is expected to outpace the global industry and account for ~14% of the overall industry (versus ~4% at present).

India semiconductor industry expected to outgrow global industry

Source: News articles, press releases, industry research; *Approximate / rounded up numbers

What are the key growth drivers for this industry?

A widespread increase in the use of electronic equipment across industries is a key driver of semiconductor demand. Besides that, technological advancements - from cloud computing, 5G, and EVs to AI and VR - are also boosting demand. For example, studies indicate that EVs require about 2-3x the number of semiconductors, compared to normal cars.

Finally, government initiatives are also helping drive growth. In 2021, India launched the India Semiconductor Mission with an outlay of ~$10 billion for semiconductor manufacturing, packaging, and design units. The government has also announced a scheme for setting up semiconductor fabrication units, which offers fiscal support of up to 50% of the project cost.

One major advantage India has is its talent pool. A 2023 article by InvestIndia.gov suggests that Indian engineers account for around 20% of the world's semiconductor design workforce.

With our credentials established, let us look at some of the key players in the industry. We note that the contribution of semiconductor revenues to total revenues is not consistently available for this dataset, but we have tried to include it wherever possible.

Select semiconductor plays in India

| # | Company | Select details related to semiconductors only |

|---|---|---|

| 1 | HCL Technologies | Well entrenched player with a strong track record of providing services to the semiconductor companies |

| 2 | Vedanta Ltd | Signed MoUs with Gujarat Government (September 2022) to set up semiconductor and display fabs. Also, exploring technology partnerships to launch its own chips |

| 3 | Tata Elxsi | Established global player in technology design and services for the semiconductor industry |

| 4 | CG Power | Filed an application to set up an outsourced semiconductor assembly and test (OSAT) facility with an estimated investment of $791 million |

| 5 | Moschip Tech | Semiconductor design and verification company which has developed IP for >30 designs and verification modules each Semiconductor revenue: >80% of revenue |

| 6 | MIC Electronics | Specialises in semiconductor packaging and testing solutions |

| 7 | RIR Power Electronics | Prominent manufacturer of power semiconductor devices for power electronics solutions. Semiconductor revenue: ~50% of revenue |

| 8 | ASM Tech | Engineering services firm that advises semiconductor equipment manufacturing companies |

| 9 | SPEL | India’s first assembly and test facility for semiconductor integrated circuits. SPEL has been servicing the demanding US market for > 20 years. Semiconductor revenue: ~100% of revenue |

Source: News articles, press releases, company financials

What should investors do?

The overall industry is set for a multi-year robust growth trajectory. While a rising tide could lift all boats, investors should look for companies with strong fundamentals, a differentiated business moat and an ability to handle any capex cycle to bolster their overall portfolio performance.

About The Author

Next Story