Upstox Originals

Decoding India’s silent equity transformation

.png)

5 min read | Updated on April 17, 2025, 15:39 IST

SUMMARY

India's equity market is experiencing a historic shift as individual investors now hold a larger share than FPIs for the first time since 2006. Domestic investors are demonstrating resilience and moving beyond blue-chip Nifty 50 stocks. This evolution signifies a structurally wider and more mature Indian equity market increasingly powered by domestic capital.

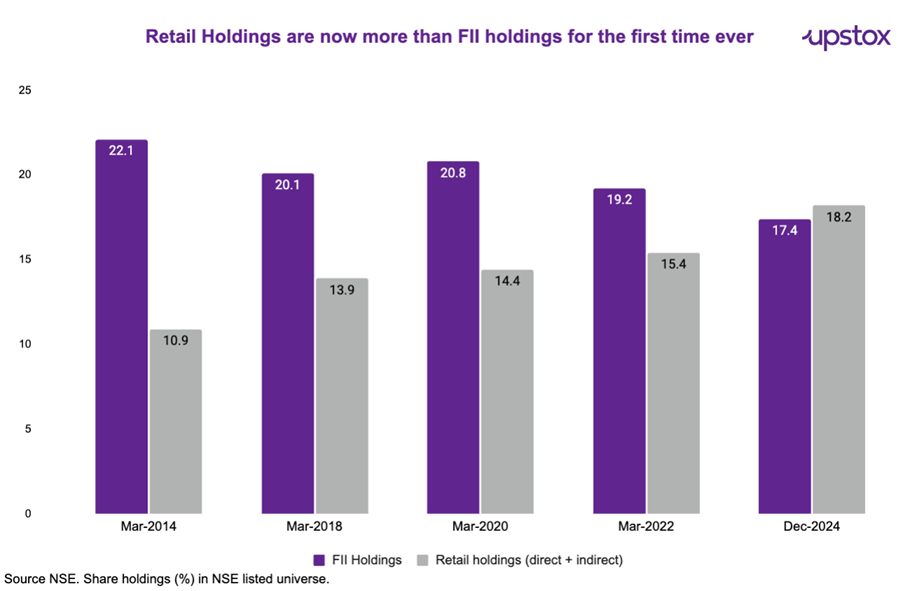

For the first time since 2006, individual investors hold a larger share in equity markets than foreign portfolio investors

Even among DIIs, individual investors stood out for their continued conviction in the equity markets. After all the volatility of 2024, it is encouraging to note that their faith in equity markets still remains resilient.

Why do we say that?

For the first time since 2006, individual investors now hold a larger share (18.2%) in Indian equity markets—both directly and through mutual funds—than foreign portfolio investors (17.4%) as of December 2024. This shift is a clear indication of the growing influence of individual investors in India’s equity markets.

How did we reach here?

Consistent inflows

Since 2021, Indian stock markets have found strong and steady support from domestic institutional investors (DIIs) and retail investors. They stood firm even when Foreign Institutional Investors (FIIs) pulled out in 2022 and again in 2025. With consistent investments—both directly and through mutual funds—individual investors now hold more of the market than FIIs for the first time ever.

| Net inflows (in ₹ cr) | FIIs | DIIs | Retail |

|---|---|---|---|

| 2019 | 1,01,111 | 42,257 | -25,280 |

| 2020 | 1,70,260 | -35,663 | 52,897 |

| 2021 | 24,004 | 94,846 | 1,42,755 |

| 2022 | -1,21,439 | 2,75,726 | 88,376 |

| 2023 | 1,71,107 | 1,81,482 | 5,243 |

| 2024 | 427 | 5,27,438 | 1,65,810 |

| 2025* | -1,12,601 | 1,51,445 | 27,265 |

Source: NSE. *Data for 2025 as of 28th Feb-25.

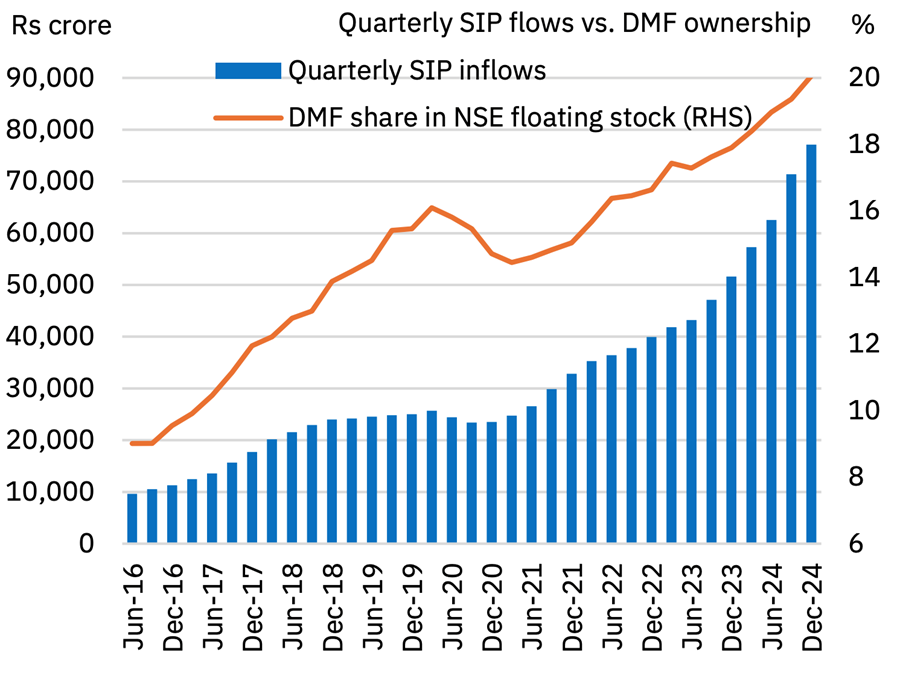

Domestic MF buying driven by SIPS:

Average monthly inflows were ₹23,743 crore for the first 10 months of FY25 (April-January), reflecting a nearly 43% increase compared to inflows of ₹16,602 crore in FY24. Additionally, SIP inflows have consistently risen quarter on quarter for the past 17 consecutive quarters, driving total net inflows from individuals to record highs. The inflows align with a consistent rise in DMF holdings from 8.8% in June-16 to 20.1% in Dec-24.

Source: AMFI, NSE

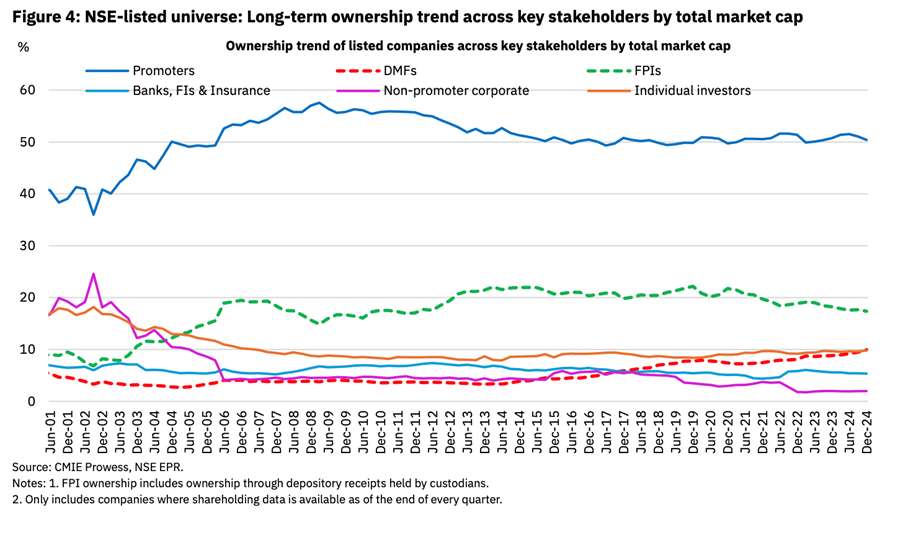

Other key stakeholders are selling

The decline in promoter and FII holdings paved the way for increased buying by DIIs and retail investors. SEBI's 2010 decision to raise the free float requirement forced promoters to reduce their stake, while government disinvestment in PSUs and rising valuations led to further selling. Additionally, geopolitical concerns, rupee depreciation, and market valuations prompted aggressive selling by FIIs.

Now, a new and important shift is underway:

Deepening market participation

Until recently, most investors preferred blue-chip companies, with their portfolios heavily skewed toward Nifty 50 stocks, which represent India’s largest and most stable firms. But this trend is starting to change.

Today, investors—both institutional and individual—are broadening their exposure beyond the top 50. There’s a visible movement towards mid-cap and small-cap companies, signalling a more diversified approach and growing confidence in the broader economy.

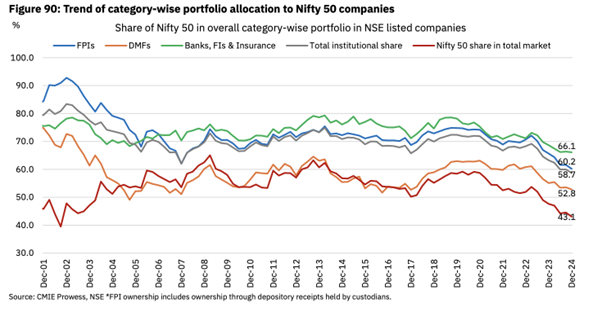

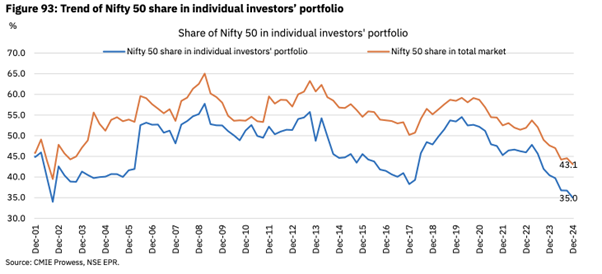

The share of Nifty 50 companies in overall institutional investments fell to 58.7%, the lowest in 24 years.

Just like institutional investors, individual investors have also reduced their investments in Nifty 50 companies. Shares of Nifty 50 stocks in their total portfolio fell to a 22-year low of 35%.

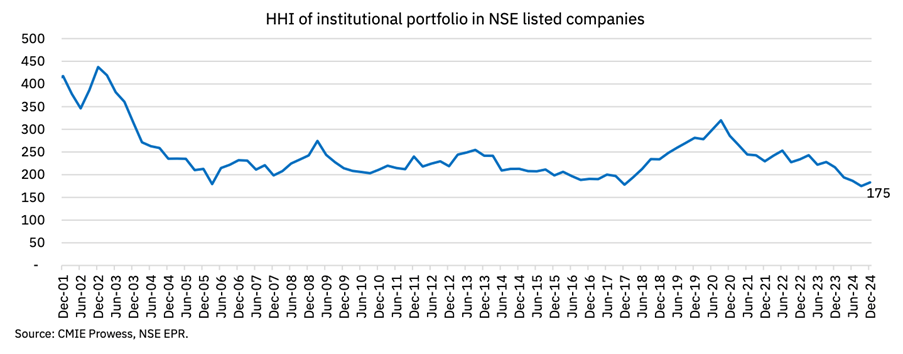

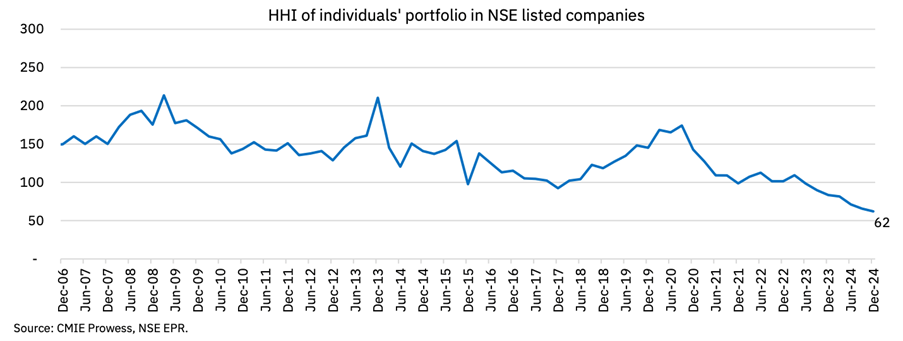

Portfolio diversification

The HHI is a measure of market concentration and diversification. Simply put lower HHI means lower concentration with a higher number of stocks in the portfolio. For institutional investors, the overall HHI stood at 183 in Dec 2024—near its lowest since 2001. FPIs’ HHI dropped significantly from the post-COVID high of 411 to 236, indicating a shift toward mid- and small-cap stocks.

Individuals are even more diversified. Their HHI dropped to a record low of 62 in Dec 2024—marking seven consecutive quarters of decline—driven by increased allocation to smaller companies.

This shift isn’t just about chasing returns. It reflects

-

Increased risk appetite

-

Greater access to research and insights

-

Wider and new investment opportunities across sectors and geographies

-

The outperformance of mid and small-cap segments in recent years:

| XIRR Returns % | 1-year | 3-year | 5-year |

|---|---|---|---|

| Nifty 50 | 1.6 | 10.2 | 21.5 |

| Nifty Midcap 150 | 0.4 | 17.3 | 32.1 |

| Nifty Smallcap 250 | -3.3 | 14.9 | 35.0 |

Source: NSE. Data as of 15th April-25. Returns mentioned above are shown in XIRR percentage terms.

The Indian market is no longer just deepening in participation—it is maturing in its allocation patterns too.

In summary

What we’re witnessing is not just an increase in participation. It is a maturing of investor behaviour—a willingness to think long-term, take calculated risks, and look beyond headline stocks.

From SIPs and disinvestments to midcap momentum and FII retreat—the forces shaping this new era of Indian equities are here to stay.

And at the heart of it, for the first time in nearly two decades, is the Indian investor—not just participating, but leading the charge.

About The Author

Next Story