Upstox Originals

Can India truly diversify its oil supply chain without increasing costs?

6 min read | Updated on February 09, 2026, 15:08 IST

SUMMARY

Tariffs may have eased, but they don’t capture the full complexity of the India–US trade discussions. A key underlying factor is energy sourcing and whether India can diversify its crude imports without raising costs or disrupting supply chains. The real constraint isn’t policy intent, but commercial feasibility; availability, pricing, and logistics ultimately shape what’s possible.

At its peak in 2019, India imported $7.2 billion worth of crude from Venezuela.

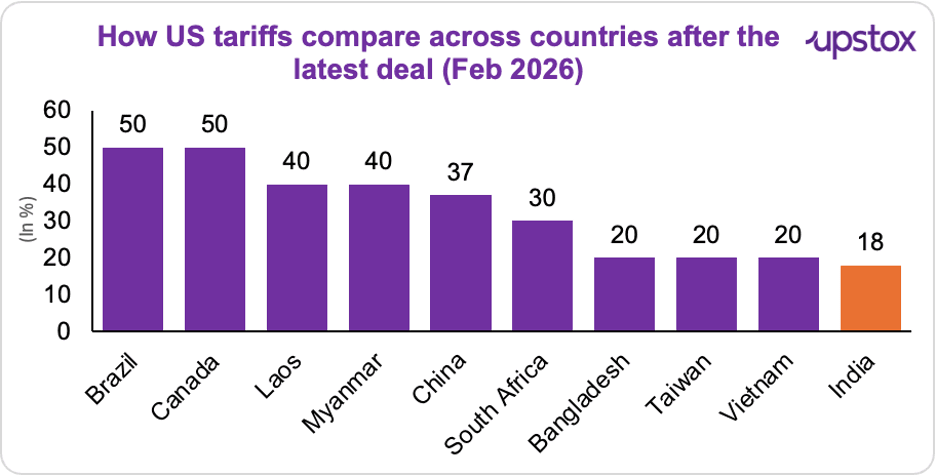

After months of back-and-forth and trade jitters, India and the US finally shook hands on a deal. Tariffs on Indian exports to the US have been chopped to 18%, down from a painful 25-50% earlier. That puts India among the lowest-tariffed Asian exporters to the US, even below Vietnam, one of Washington’s go-to trade partners.

Source: SBI Research

But… this deal isn’t really about tariffs alone. There’s oil quietly flowing beneath the headlines.

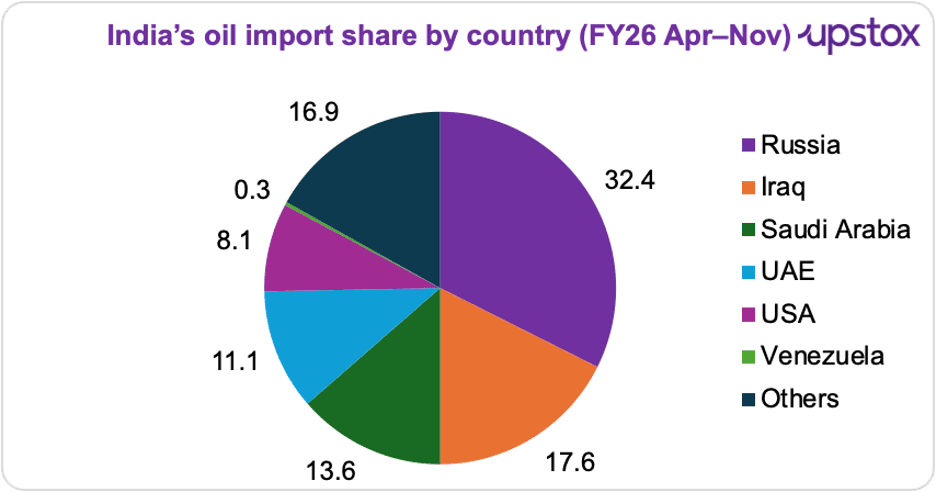

And here’s why that matters. Currently, India purchases a major chunk of oil from Russia because it is available at a discounted price. The question that arises is - can India reshuffle priorities that soon?

Source: SBI Research

Before we dive in, we should note that India has not publicly confirmed any commitment to begin importing Venezuelan/US crude. India has however acknowledged that we would like to diversify our supply chain, which is in our own interest.

There’s also history here. At its peak in 2019, India imported $7.2 billion worth of crude from Venezuela. Then US sanctions hit. And those flows collapsed to almost nothing.

So when Venezuela resurfaces today, it demands attention.

What happens if India switches to Venezuelan oil?

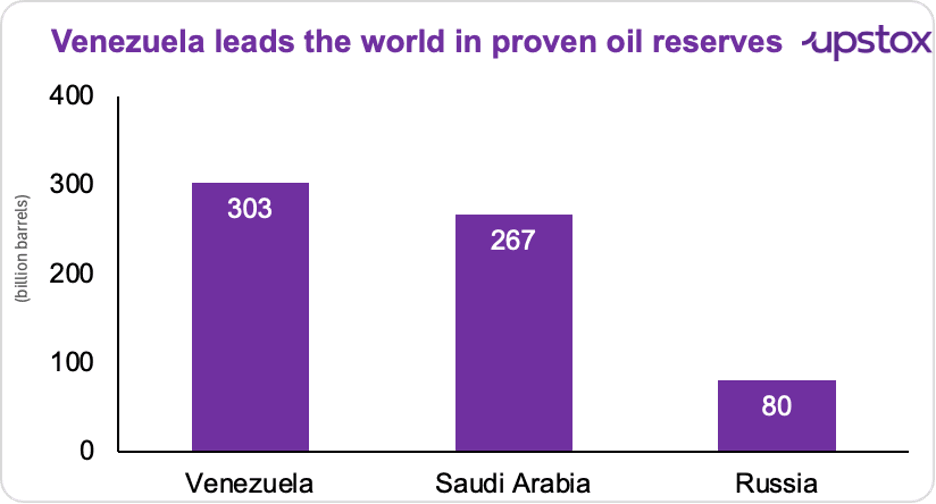

Yes, Venezuela sits on the world’s largest oil reserves. But reserves don’t power refineries; production does.

Source: CNBC

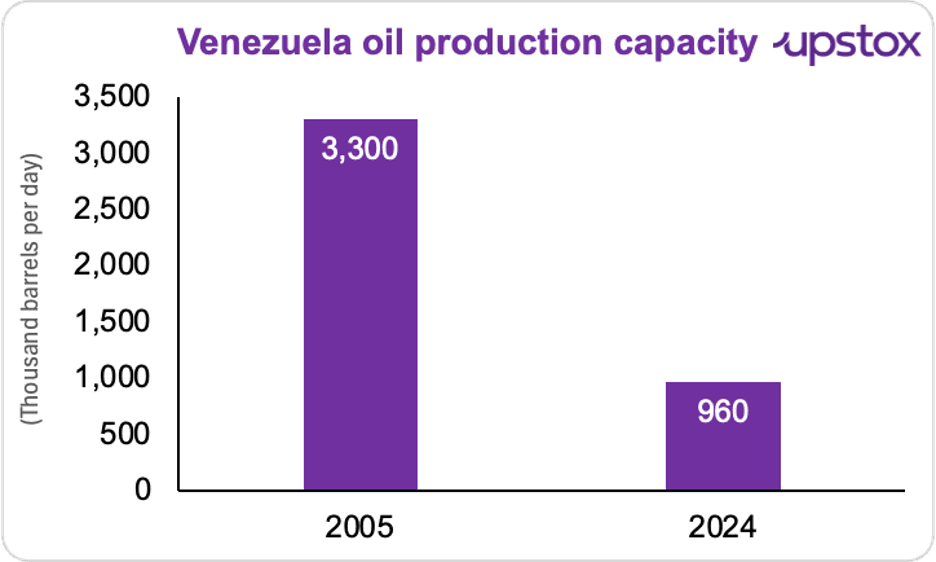

But today, Venezuela produces only about 800,000 barrels a day. Even when pushed to its limit, output barely touches 1 million barrels per day. That’s nowhere close to replacing the Russian oil India currently buys.

Source: CNBC

It wasn’t always this way.

Back in the 1990s, Venezuela pumped 3.5 million barrels per day. But production slid sharply after the 2007 expropriation of foreign oil assets, fell further during the 2014–16 oil price crash, and took another hit during the pandemic in 2020. And despite oil prices recovering later, Venezuelan output never really bounced back.

So here’s the reality check. As energy analyst Oxley told CNBC, “Getting oil production back up to 3+ million barrels in Venezuela would require a vast amount of investment — probably around $180 billion over the next 15 years.” That’s not a quick fix. That’s a decade-plus rebuild.

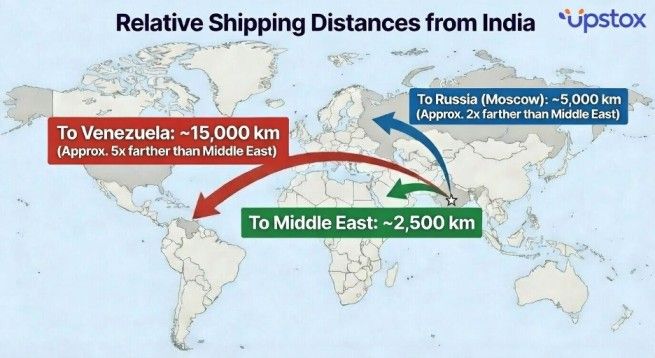

There’s another snag: Distance.

As SBI Research points out, Venezuela is five times farther from India than the Middle East, and roughly twice as far as Russia. And distance matters in oil.

A longer journey means higher freight costs, longer transit times, and steeper insurance bills. All of that pushes up the landed price of crude by the time it reaches Indian refineries.

Source: Author’s creation

And then there’s the price problem.

Russian oil is cheap.

As energy analyst George Voloshin points out, Russian Urals crude has been trading at a $10–20 per barrel discount to Brent. Venezuelan Merey crude? That discount is much smaller, around $5–8 per barrel.

That gap matters. The smaller discount isn’t the only problem; logistics quietly make it worse. Scale that up, and it gets serious.

According to Kpler, a complete pivot away from Russian oil could raise India’s import bill by $9–11 billion a year. So when does Venezuelan oil actually work?

Only if it’s deeply discounted.

Right now, Venezuelan oil is trading near $51 per barrel, according to SBI. At a $10–12 discount, the economics can hold. Without it, they don’t.

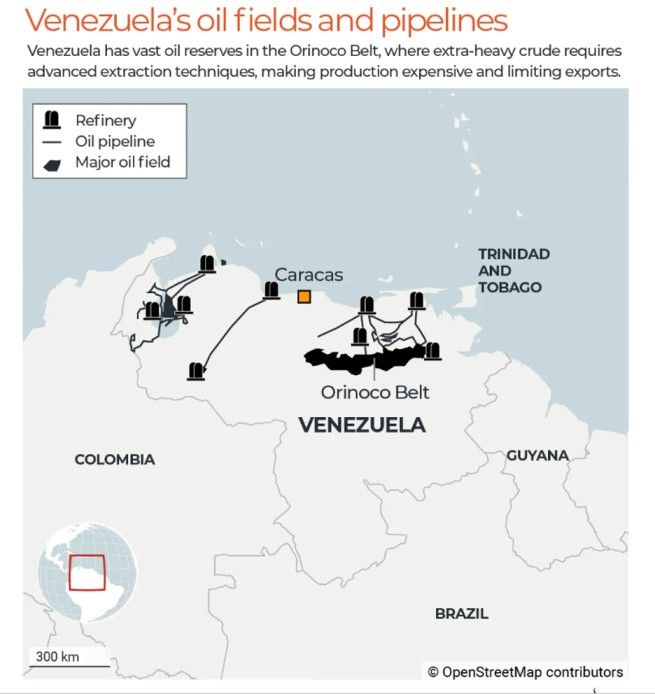

There’s another structural issue: Who runs Venezuela’s oil sector.

Most of the country’s oil production is controlled by PDVSA, the state-owned oil giant that dominates operations in the Orinoco Belt; where most of Venezuela’s oil sits.

Source: Al-Jazeera

And PDVSA hasn’t had an easy run.

Over the years, it’s struggled with ageing infrastructure, chronic underinvestment, mismanagement, and the heavy weight of international sanctions. All of that has steadily weakened its ability to produce and export oil at scale.

So while Venezuela has plenty of oil underground, the company responsible for extracting it has been operating well below potential.

The problem isn’t just how much oil Venezuela has. It’s whether its oil industry is strong enough to deliver it reliably.

So can India just buy US oil in the meantime?

To a degree, it already is. Between April and November 2025, the US share of India’s crude imports nearly doubled; from 4.6% to 8.1%. But that’s diversification at the margins, not a replacement. Like Venezuela, US crude faces similar commercial frictions (freight, distance, pricing), which means scaling it up quickly could push costs higher. That’s why any shift away from Russian oil shows up as a slow rebalance; not a sudden switch.

Why is switching suppliers harder than it looks?

Now, here comes the question.. Can Indian oil companies switch suppliers easily?

In theory? Yes. In practice? It will take time.

India’s oil imports are handled mostly by public sector OMCs like Indian Oil, BPCL, and HPCL. And they don’t buy oil based on geopolitics; they buy based on price, refinery fit, and delivery reliability.

Indian refineries are complex and flexible, so technically they can process crude from many countries. But here’s the catch.

Refineries are tuned for specific crude blends. Long-term contracts are carefully optimised. And sudden switches mess with costs, efficiency, and margins. So yes, OMCs can change suppliers, but.. slowly. Doing it quickly and at scale is expensive and inefficient.

That’s why India’s oil basket usually shifts gradually, driven by economics, not overnight decisions.

Looking ahead

So what happens next?

If India is expected to gradually reduce its dependence on Russian oil, how does that actually play out on the ground?

Oh yes, and what about Nayara Energy; one of India’s two private refiners, running a large Gujarat refinery that processes about 4 lakh barrels of oil a day, and nearly half-owned by Russia’s Rosneft?

In January alone, Nayara imported roughly 4.7 lakh barrels per day, making up close to 40% of India’s Russian oil imports.

If Russian oil flows do change, what happens to refineries like this; and how long does that adjustment take?

Credit rating agency Moody’s echoes some caution. A full phase-out of Russian crude could reshape global energy flows, and not without pain.

So while the trade deal puts oil back in the spotlight, what follows isn’t a single decision or deadline.

It’s a moving picture.. one that will evolve with markets, geopolitics, and time.

And for now, that story is still being written.

About The Author

Next Story