Upstox Originals

Breaking down RBI’s financial stability report

.png)

6 min read | Updated on January 10, 2025, 19:05 IST

SUMMARY

RBI’s Financial Stability Report hints at some rising challenges in India’s financial system. Whether it is slowing lending growth in banks, falling asset quality in NBFCs, or rising delinquencies in microfinance. In this article, we deep dive into some of the key takeaways from that report and simplify these for you. Finally, we answer the pressing question - how dire is the situation?

RBI's Financial Stability Report has highlighted concerns about India's financial institutions

As per RBI’s Financial Stability Report, after years, the Financials sector in India (Banks + NBFC + Microfinance) has started to show some signs of concern.

Is the situation dire? Not yet. But as we show in this article, a stitch in time will save nine. Corrective steps, if taken immediately, will make this just a small passing phase, else, this has the potential to snowball.

In this article, we take a look at each of these sectors and break down the report for you.

Let’s start with the big one - Banking

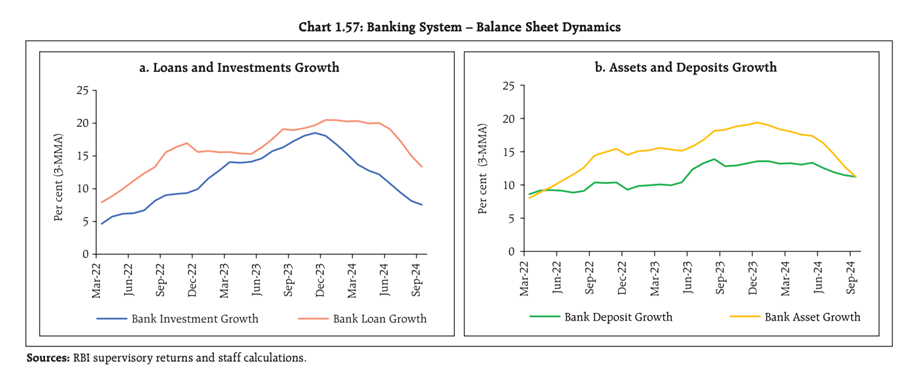

Growth tapering off

The banking sector is facing the problem of tapering growth. Loan growth is moderating as most corporates (which form a major portion of the banking sector’s loan book) are focusing on debt reduction. Equity funding has become easier as evidenced by the fundraising seen in 2024 (highest ever equity raise).

Similarly, on the deposit side, growth is moderating because various stakeholders are moving towards high-yielding instruments like mutual funds, equity, debt.

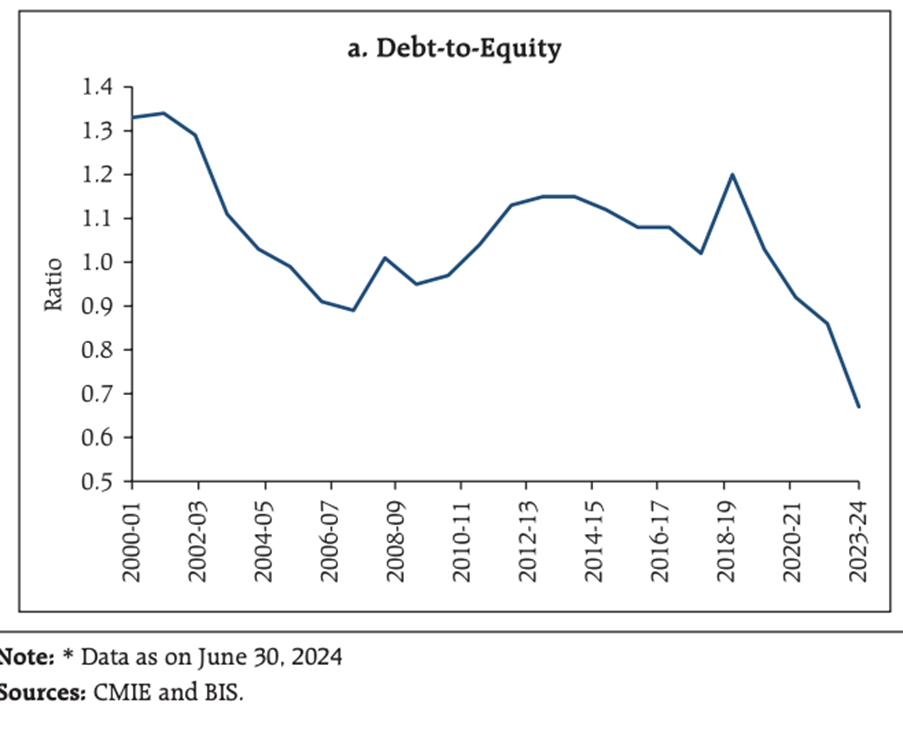

This is further confirmed by the reduced debt-to-equity ratio for non-financial companies. Presently the ratio is at an all-time low. While this may bolster confidence in non-financial companies, it is not exactly good news for banks, whose primary business is lending.

Profitability pressure

As a result, banks’ NIM and profitability face pressure from stiffer competition for funds. NIM stands for Net Interest Margin. Simply put, it is the difference between the rate at which a bank lends less the rate at which it borrows money (think interest rate on deposits).

As fewer corporates are out to borrow, banks are having to offer increasingly attractive interest rates to lure customers, which is hurting its profitability.

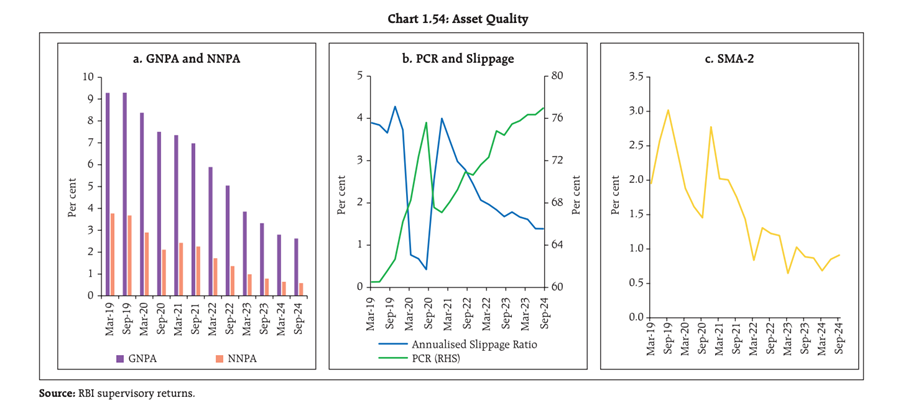

Asset quality concerns rising

We have good and bad news here.

Without getting into too much technicality, think about Scheduled Commercial Banks (SCBs) as private, public, and foreign banks in India. If you can think of a bank’s name, most likely it will be an SCB.

Bad news first

SCBs are seeing a rise in Gross Non-Performing Assets (GNPAs) for retail advances. What this means is that retail borrowing is seeing some stress and people are either unable to payback their interest or principal, or are delaying payments. This is causing problems for banks. Just for context, retail advances account for 32.9% of the total non food credit lending.

On a more optimistic note

Overall GNPAs are still well under control. While FMCG as a sector has seen some rise, the rest of the sectors continue to remain resilient.

Source: RBI Financial Stability Report

Overall, asset quality remains intact for banking

Despite some rise in GNPA, overall Non-Performing Assets remain well under control and at a 5-year low. The Provision Coverage Ratio (PCR) which measures how much funds banks have to cover losses due to bad debts remains healthy, which is a further sign of comfort.

However, SMA-2 (loans over-due for more than 60 days but less than 90 days) are the lead indicator of NPAs have started picking up again showing signs of emerging stress.

What does this mean for banking?

As we see it, the problem can be summed up in one word - growth. We are of course simplifying this to a considerable extent, but here is our summation - if deposit and lending growth picks up once again - banks will be able to overcome these short-term hurdles.

Similarly, growth in overall economic activity will also reduce the burden on the various sectors and once again help keep any potential distress under check. So, management commentary and performance in the upcoming Q3FY25 (quarter ending December 2024) result season will be keenly monitored.

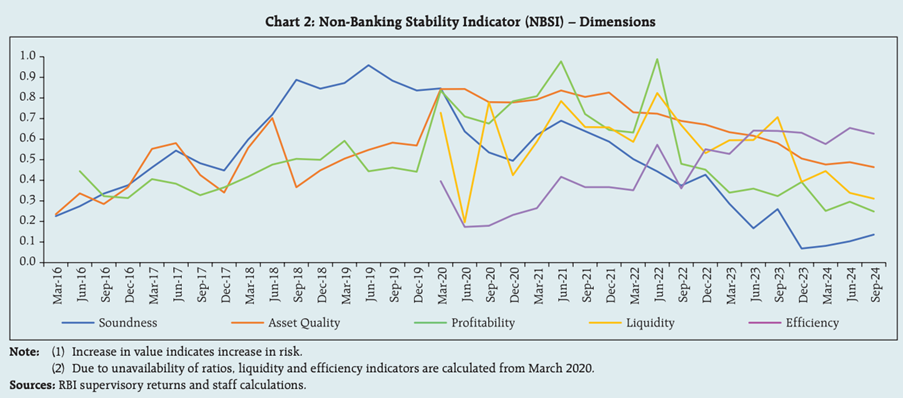

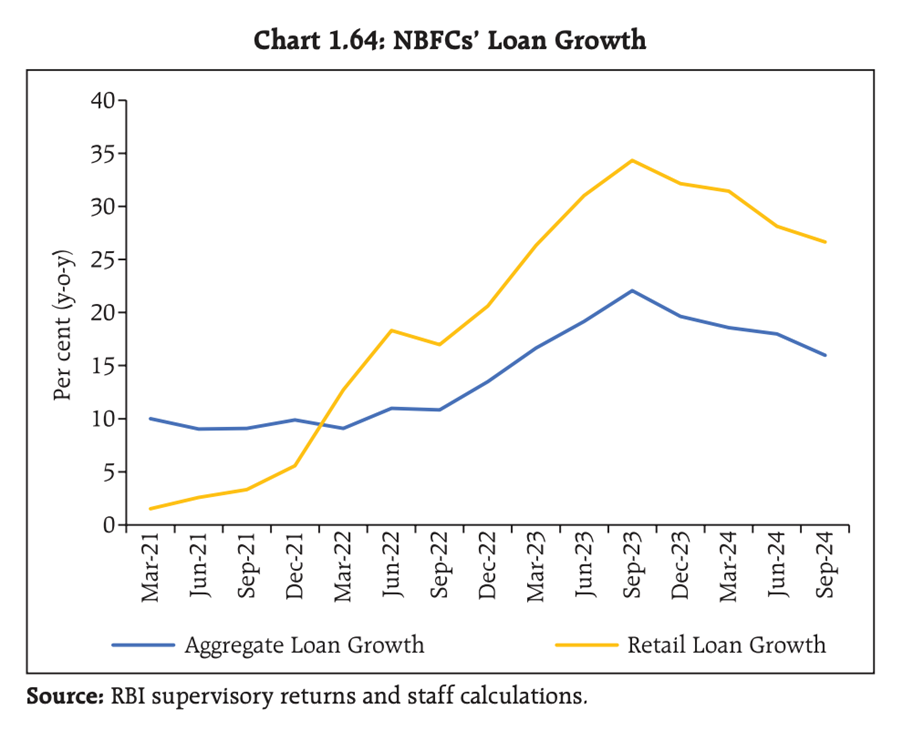

NBFCs

The NBFC sector is facing slowdown as evident from falling soundness, asset quality, profitability, liquidity and overall efficiency. This is mainly due to multiple initiatives by RBI for tightening credit (like increasing risk weightage of personal loans), increasing interest cost, aggressive branch expansion (impacts efficiency) and emerging credit risk especially in personal finance.

What does it mean for NBFCs?

Unlike banks, it seems NBFCs seem to be facing twin issues of growth and asset quality. As highlighted by RBI, loan growth for NBFCs has slowed down to about 6.5% as of H12024-25. A pickup in growth is therefore vital to revive NBFCs. With regards to asset quality, NBFCs may need to tighten their underwriting standards (specially for personal loans) and bolster their collection efficiency to ensure that stress on books is limited.

Finally, microfinance

For those not aware - microfinance institutions provide banking services for low-income individuals who otherwise do not have access to traditional banking services.

The sector shows signs of stress, with rising delinquencies across all lenders and ticket sizes.

During H12024-25, the share of stressed assets increased. The share of those who were 31-180 days past due (dpd) has almost doubled from 2.2% in March 2024 to 4.3% in September 2024.

Source: RBI Financial Stability Report

Besides this, the report notes that among borrowers who availed loans from multiple lenders, impairment remained high. The report points out that the share of borrowers availing loans from 4 or more lenders has increased from 3.6% to 5.8% during the last 3 years (September 2021 to September 2024).

While 5.8% may look like an optically lower number, here is why this matters. Those who have taken loans from various lenders will have higher debt and are unable to pay. If this further escalates, failure to repay loans will simultaneously impact more than one institution and impact its financial strength.

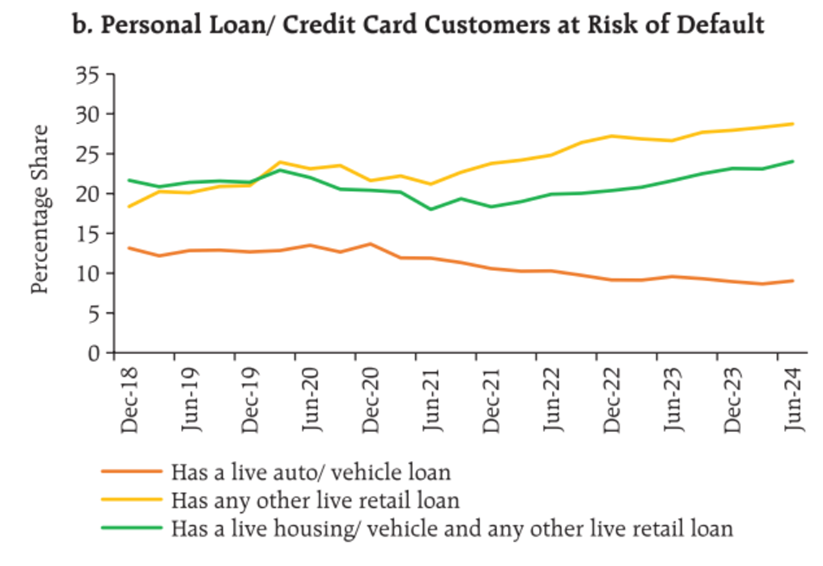

Existing borrowers borrowing more

Nearly half of the borrowers (yellow + green line) availing credit card and personal loans have another live retail loan outstanding, which are often high-ticket loans (i.e., housing and/or vehicle loan).

Given that a default in any loan category results in other loans of the same borrower being treated as non-performing, these larger and secured loans are at risk of slippages in relatively smaller personal loans.

Source: RBI Financial Stability Report

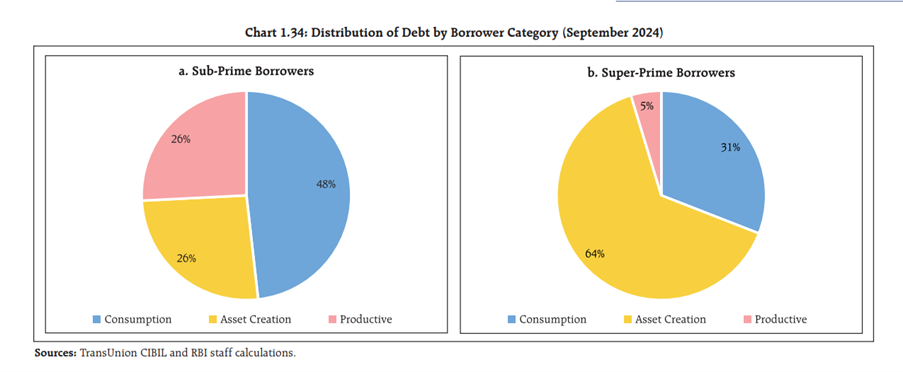

Subprime borrowers—those with lower credit scores - spend 48% of their loans on consumption, compared to super-prime borrowers - those with excellent credit - who only use 31% of their debt that way.

Source: RBI

What does this mean for microfinance?

Microfinance is relatively more riskier than the other two segments. That said, it is possible that the situation is not as bleak. And one potential reason could be the resilience of the rural economy. As guided by most industries from fields to fortunes, rural demand remains robust, driven by increasing rural income. And while the increase in indebtedness is definitely something to be stayed on top of, so far, there are no imminent signs of the sky falling down.

About The Author

Next Story