Upstox Originals

Are Indian REITs having their moment in the sun?

6 min read | Updated on February 27, 2026, 19:28 IST

SUMMARY

Indian REITs had a winning year, not because markets turned friendly, but because offices stayed full, rents moved up, and cash flows held steady. Policy tailwinds - from rate cuts to regulatory tweaks- only strengthened the math. And with India’s REIT market still small, office-heavy, and under-penetrated, this looks less like the end of a rally and more like the early innings of a longer story.

Stock list

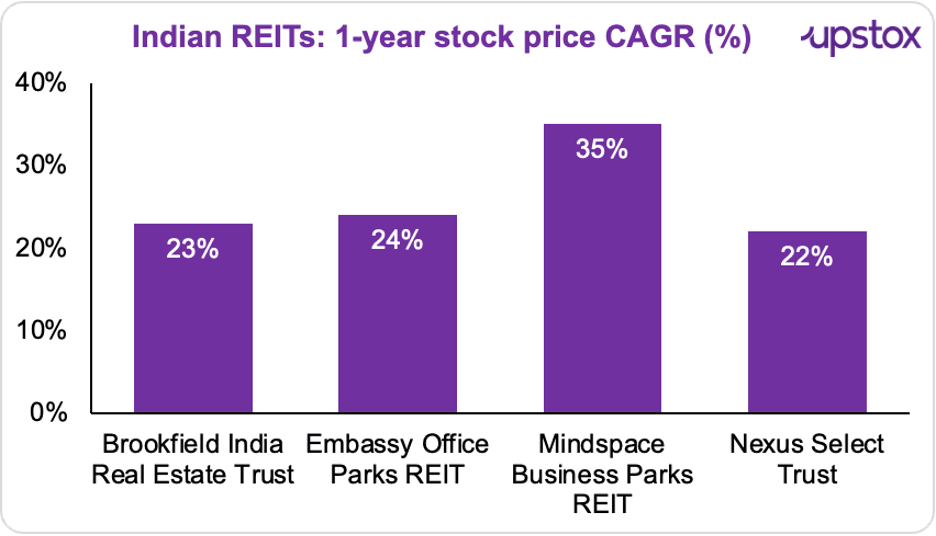

Over the past year, listed REITs posted one-year gains in the 20–30% range.

The last year had it all - volatility in markets, weak metals, and no clear winners. And yet, away from the noise, Indian REITs quietly did the heavy lifting.

Over the past year, when broader markets struggled to find direction, listed REITs delivered unexpectedly strong returns. Names like Embassy Office Parks REIT, Mindspace Business Parks REIT, and Brookfield India Real Estate Trust posted one-year gains in the 20–30% range.

Source: Investing.com, *Note: Knowledge Realty Trust, listed in August 2025, is excluded due to insufficient one-year trading history. One-year returns as on February 18, 2026

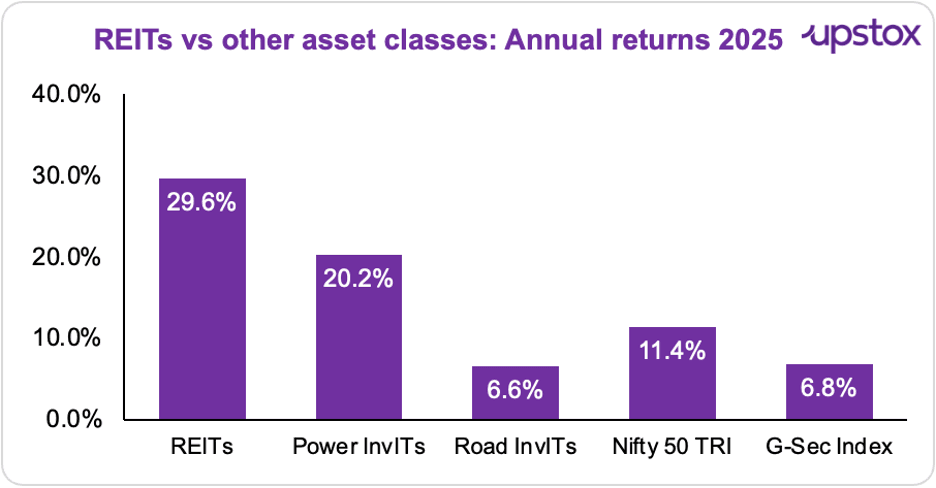

And the outperformance wasn’t marginal. According to ICRA Analytics, REIT returns comfortably beat the Nifty50 TRI’s 11.4% and the G-Sec Index’s 6.8% over the same period. Data from InfRE360 shows listed REITs emerging as one of the most resilient asset classes of the year.

In fact, REITs topped the pack with a 29.6% return, driven by steady leasing activity and stable yields. REIT returns nearly doubled; rising from 16.8% in 2024 to 29.7% in 2025; underscoring how consistent cash flows and improving occupancy quietly powered the rally.

Source: News articles

So why did REITs hold up?

Leasing didn’t collapse

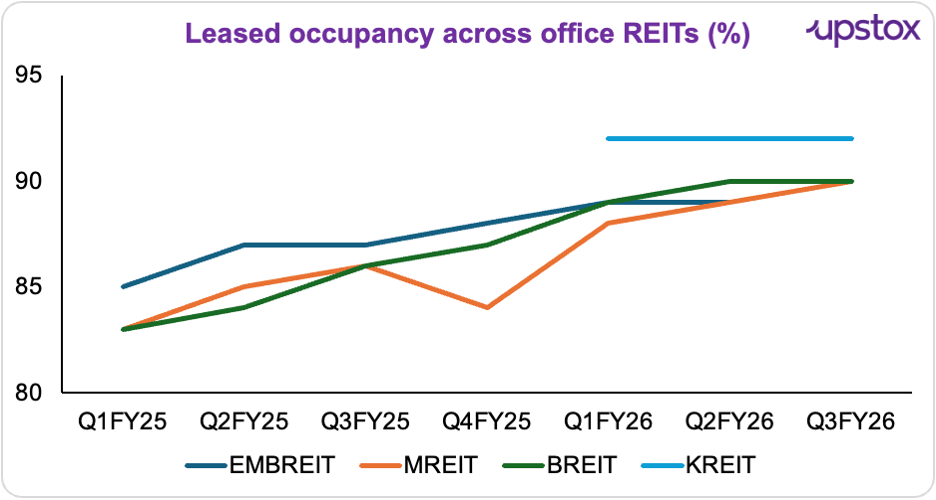

By FY25, most office REIT portfolios crossed 90% occupancy.. a key inflection point. Above this level, rentals become predictable and downside risk drops sharply. And that fed straight into Net Operating Income (NOI) and Distributions Per Unit (DPU).

Source: Company reports, Nuvama

Leasing momentum stayed strong through FY25–FY26, led by GCCs and supported by domestic demand from BFSI, IT, and flex spaces. In fact, GCCs alone accounted for ~30–45% of new leasing across major REITs.

Rents started moving up

And landlords finally had pricing power.

It wasn’t just about offices being full. Rents started rising too. Across office REITs, in-place rents grew 4–6% year-on-year.

The bigger boost came during re-leasing. During Q2 FY26, listed Indian REITs reported strong re-leasing spreads, largely ranging between 27%-36%, as per Anarock Research. That showed clear pricing power, landlords could charge more, and tenants were willing to pay.

These mark-to-market (MTM) gains meant expiry-led renewals kept pushing rents higher, even without aggressive new leasing. And that supported steady rental escalation across portfolios.

Oh, and regulatory nudges!

Rates came down. So did costs.

In 2025, the RBI cut the repo rate by 125 bps. That made borrowing cheaper for REITs, left more cash on the table, and helped keep distributions strong. REITs started looking like equities.

From January 2026, SEBI started treating REITs as equity-related instruments. Earlier, they sat in the non-equity bucket, which limited mutual fund participation. This change opens the door to more domestic money, better liquidity, and possible index inclusion. SEZ offices got a second life.

A policy change in December 2023 allowed REITs to remove SEZ status from certain office buildings. That meant they could lease space to any company, not just SEZ-eligible firms. The result? Many of these offices quickly reached 84–96% occupancy, lifting overall portfolio performance.

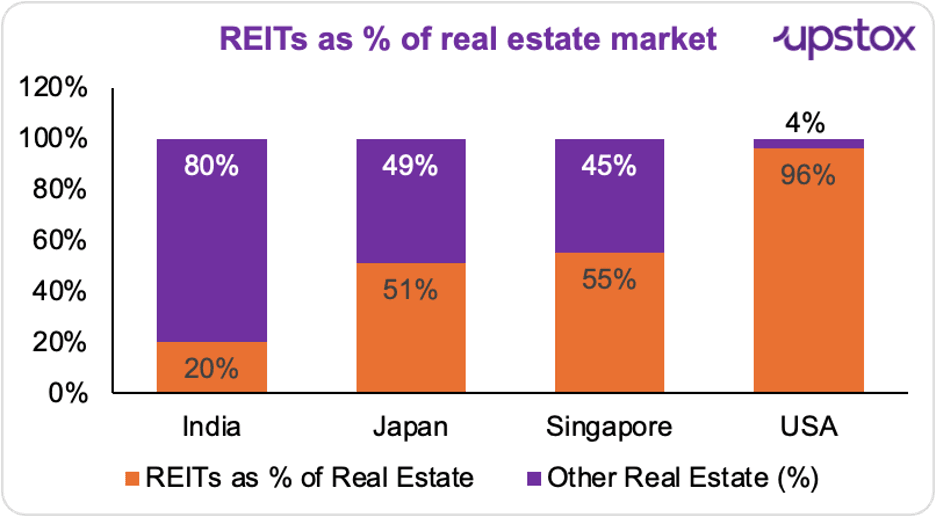

India’s REIT market is small, and that’s the opportunity

In India, REITs account for only ~20% of institutionally owned commercial real estate. In contrast, REITs dominate institutional property ownership in more mature markets - ~96% in the US, 55% in Singapore, and 51% in Japan.

This gap doesn’t reflect weaker real estate fundamentals in India. Instead, it reflects market maturity. India’s REIT framework is less than a decade old and currently concentrated largely in Grade A office assets. As the market deepens - with more assets, sectors, and listings - REIT penetration has significant room to grow.

Source: Anarock Research

Of India’s five listed REITs, only Nexus Select Trust has a retail-focused portfolio; the other four are concentrated in office assets.

A quick comparison with the global peers:

| Country | No. of Publicly Traded REITs | Market Cap ($ Bn) | % of Global REIT Index | Share of Top 3 REITs | Avg Dividend Yield of Top 3 REITs |

|---|---|---|---|---|---|

| USA | 196 | 1425 | 72.0% | 16% | 2.50% |

| Australia | 32 | 126 | 6.5% | 58% | 4.20% |

| Malaysia | 18 | 12 | 0.1% | 61% | 5.50% |

| Japan | 57 | 104 | 5.5% | 13% | 5.00% |

| Singapore | 39 | 73 | 3.0% | 37% | 6.00% |

| UK | 45 | 80 | 4.5% | 36% | 4.60% |

| India | 5 | 18 | 0.5% | 72% | 5.70% |

Source: Anarock Research

India’s REIT market still has plenty of headroom. Penetration is low, portfolios are office-heavy, and that’s exactly where the next leg of growth could come from. Globally, REIT markets scale by expanding into data centres, logistics, industrial parks, and warehousing; asset classes that are both yield-generating and institution-friendly. India is beginning to move in that direction.

Residential REITs, however, remain a tougher sell. Rental yields hover around 2–3%, ownership is fragmented, tenant churn is high, and large institutional rental portfolios are still rare. Add to that the absence of a unified rental housing policy, and the economics start to look strained.

Looking ahead

India's REIT story is shifting from scale to capital efficiency and cash-flow stability. The Reserve Bank of India has proposed allowing banks to lend to listed REITs, with exposure capped at 49% of asset value and eligibility limited to seasoned, well-regulated trusts. REITs could soon access cheaper, more stable funding, similar to InvITs.

The proposal applies to India’s five listed REITs and comes with guardrails: no land acquisition financing, no balloon repayments, and strict monitoring of fund use. Importantly, it arrives as fundamentals improve.

Residential REITs, meanwhile, remain a longer-term story. Low rental yields, fragmented ownership, high churn, and the lack of a unified rental housing policy continue to hold them back, even as formats like co-living and student housing show early promise.

Better occupancy and easier access to capital are quietly setting up the next phase of India’s REIT market.

About The Author

Next Story