Market News

Week ahead: RBI policy, crude oil prices, FIIs activity among key market triggers to watch

.png)

5 min read | Updated on May 31, 2026, 11:46 IST

SUMMARY

The focus in the week ahead will remain on FII flows, crude oil prices, rupee movement, global cues and the RBI policy outcome. Technically, NIFTY50 needs to reclaim the 23,800 to 24,000 zone to regain strength, while 23,200 remains the key support to watch.

RBI will announce its policy outcome on June 5.

Indian markets enter the new week on a cautious note after a weak close in the previous holiday-shortened week. The NIFTY50 slipped 0.7% to end at 23,547, while the SENSEX fell 0.8% to 74,775. Indices were weighed down by persistent FII selling, MSCI rebalancing-led outflows, profit booking in heavyweights and uncertainty around U.S.-Iran negotiations.

However, the broader market continued outperformance relative to benchmark peers.The NIFTY Midcap 150 (+0.3%) and Smallcap 250 (+1.2%) indices extended gains for the second straight week. The rupee also remained in focus after extending gains for the second consecutive week. It appreciated by 70 paise to settle at 95 per U.S. dollar, supported by easing crude oil prices.

Sectorally, the market trend was mixed during the week. PSU Banks, Energy and Metal were the top gainers, gaining around 1% each.On the other hand, Oil & Gas, FMCG and Pharma declined 1–1.5%

Globally, the focus will be on U.S. jobs data. The week will see key releases such as weekly jobless claims and non-farm payrolls. These numbers will shape expectations around the U.S. Federal Reserve’s rate path and may influence bond yields, dollar index and FII flows.

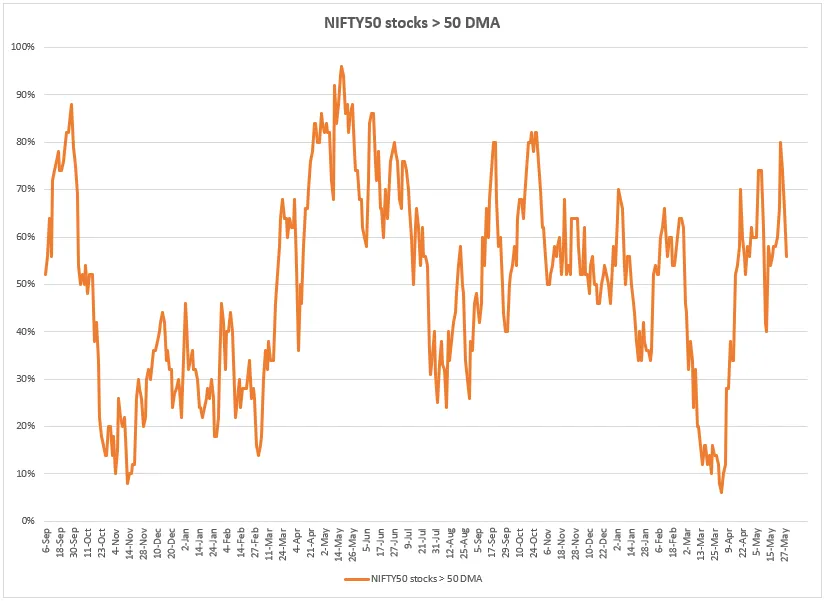

Market breadth

Market breadth cooled during the week after a sharp recovery seen through April and May. The share of NIFTY50 stocks trading above their 50-DMA slipped from the recent high of nearly 80% to around 55–60%. This shows that participation has moderated after the recent rally. However, breadth still remains above the neutral 50% mark, suggesting that the market has not turned weak internally yet.

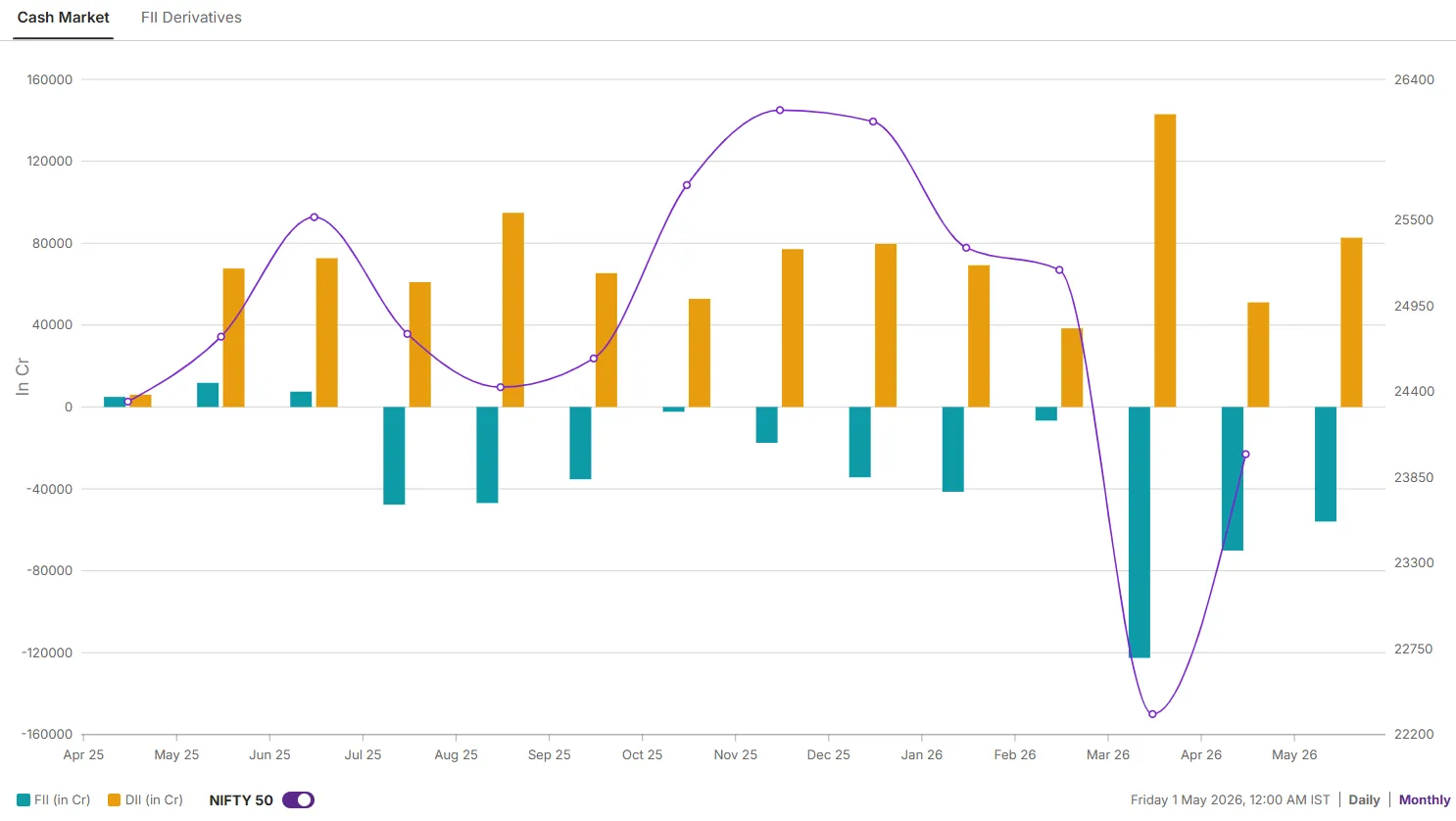

Foreign investors positioning

Foreign investors remained net sellers, offloading equities worth ₹23,782 crore during the week. The selling was partly driven by MSCI rebalancing-led outflows. In the derivatives market, FIIs continue to remain heavily positioned on the short side. Their index futures long-to-short ratio remains weak, indicating that foreign investors are still not taking aggressive bullish bets on Indian equities.

NIFTY50 outlook

The NIFTY50 index ended the week on a weak note and slipped below the 23,800 zone, which had acted as an important short-term level in the previous sessions. The index also closed below its 20-DMA and 50-day EMA, showing that momentum has weakened again.

For the week ahead, the 23,800–23,850 zone will act as the immediate resistance. A close above this range will be the first sign of strength. Until then, recovery attempts may face selling pressure at higher levels.On the downside, 23,100 is the immediate support to watch. A break below this level could extend weakness.

Disclaimer:

Derivatives trading must be done only by traders who fully understand the risks associated with them and strictly apply risk mechanisms like stop-losses. We do not recommend any particular stock, securities, or trading strategies. The securities quoted are exemplary and not recommendatory. The stock names mentioned in this article are purely to show how to do analysis.

About The Author

Next Story