Market News

Week ahead: Oil prices, Strait of Hormuz, Reliance earnings and FII flows to drive markets

4 min read | Updated on April 19, 2026, 14:58 IST

SUMMARY

Indian markets enter the week with multiple key triggers in focus. Crude oil volatility and developments around the Strait of Hormuz will remain critical for global sentiment. On the earnings front, Reliance Industries could influence index direction. At the same time, FII flows will be closely tracked as the index approaches key resistance zones.

Foreign investors have remained consistent sellers in the cash market through April, although the intensity of outflows has eased. | Image: Shutterstock

Indian markets extended their gains for the second straight week, supported by easing geopolitical concerns and sustained buying in key sectors. Benchmark indices like the NIFTY50 rose 1.2% to 24,353, while the SENSEX advanced 1.2% for the week. The overall tone remained positive, although markets did witness some intraday volatility near resistance levels.

A key driver behind the sustained positive movement was easing global risk factors, particularly around crude oil prices. This helped improve investor sentiment, while resilience in global equities, especially the U.S. markets aided sentiment.

However, the upside was not entirely smooth. Foreign investors remained cautious, with selling pressure easing but not fully reversing. As a result, while the broader trend stayed positive, markets appear to be entering a phase where follow-through strength will be crucial for sustaining the up-move.

Sectorally, the trend remained positive with the majority of the sectors closing in the green. The only exception was Automobiles which slipped 0.7%. On the other hand, Defence stocks led the rally with a sharp 6.2% gain. Metals and Consumer Durables also performed well, rising 4.2% each.

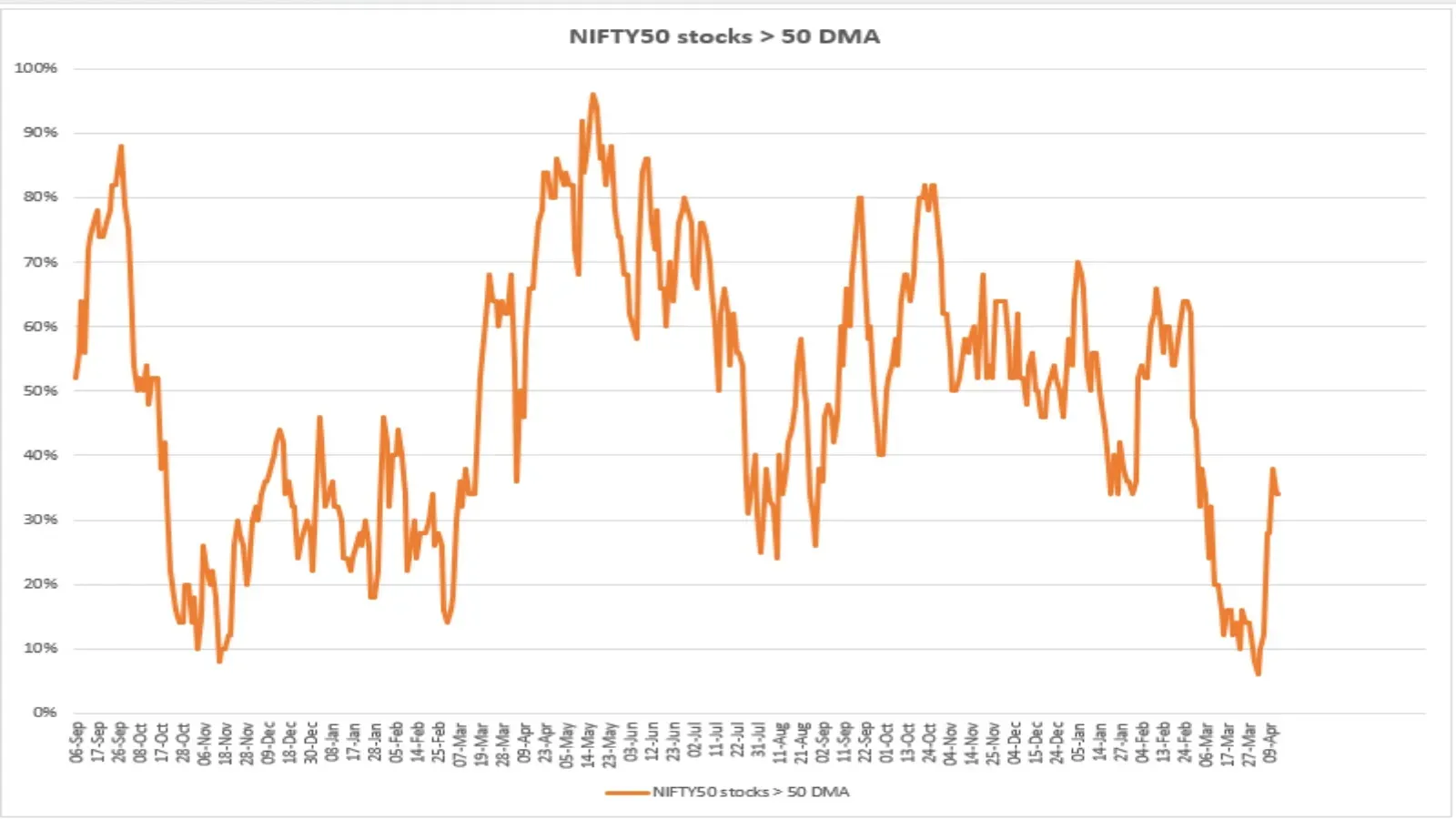

Market breadth

Market breadth showed signs of improvement, it remains far from strong. The percentage of NIFTY50 stocks trading above their 50-day moving average increased from a low of around 10% to the mid-30s this week. This suggests that although the index has recovered, participation remains limited and is not widespread.

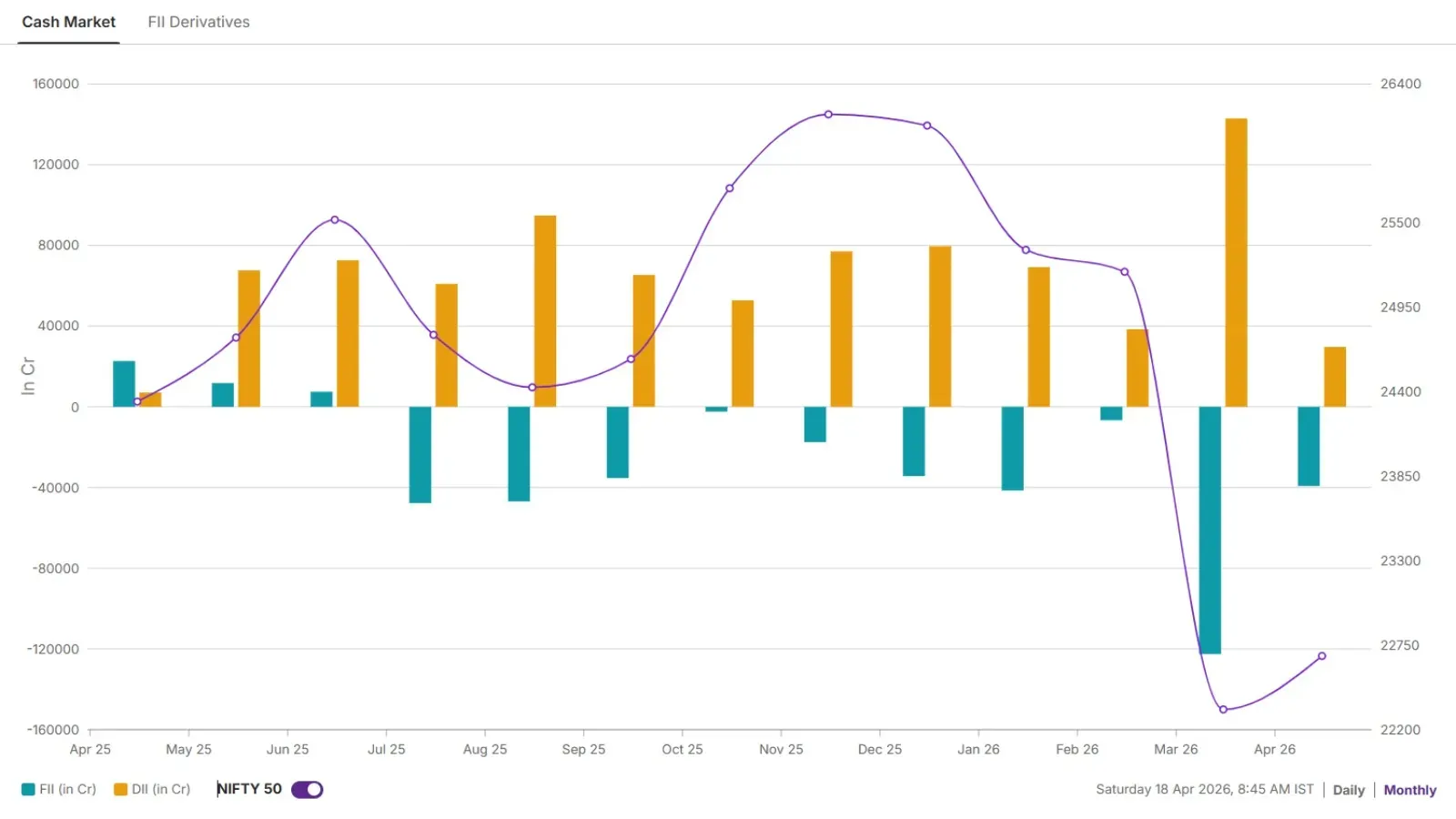

Foreign investors positioning

Foreign investors have remained consistent sellers in the cash market through April, although the intensity of outflows has eased. They are yet to turn meaningful buyers. For the month so far, net selling stands at ₹39,224 crore, while for the week, FIIs were marginal net sellers to the tune of ₹251 crore.

NIFTY50 outlook

The NIFTY50 continues to encounter resistance at around 24,300–24,500, with the recent rebound losing momentum at these levels. On the downside, the 23,700–23,500 zone remains crucial support and has acted as the recent swing base.

Technically, the index is range-bound, with higher levels witnessing profit-booking. A sustained move above 24,300 could pave the way to the 24,800 zone, whereas a break below 23,500 could shift the trend towards sideways or bearish movement.

About The Author

Next Story