Market News

Week ahead: India-US trade deal, Q3 earnings, and FIIs activity among key market triggers to watch

.png)

4 min read | Updated on February 09, 2026, 08:37 IST

SUMMARY

NIFTY50 index extended its recovery for a second straight week, rebounding from Budget day lows after the India-US trade deal improved sentiment. Meanwhile, market breadth and FII positioning showed signs of stabilisation, with easing selling pressure and gradual short covering. In the week ahead, the market’s direction will hinge on US inflation data, key Q3 earnings and global cues, while the NIFTY structure stays positive as long as crucial support levels hold.

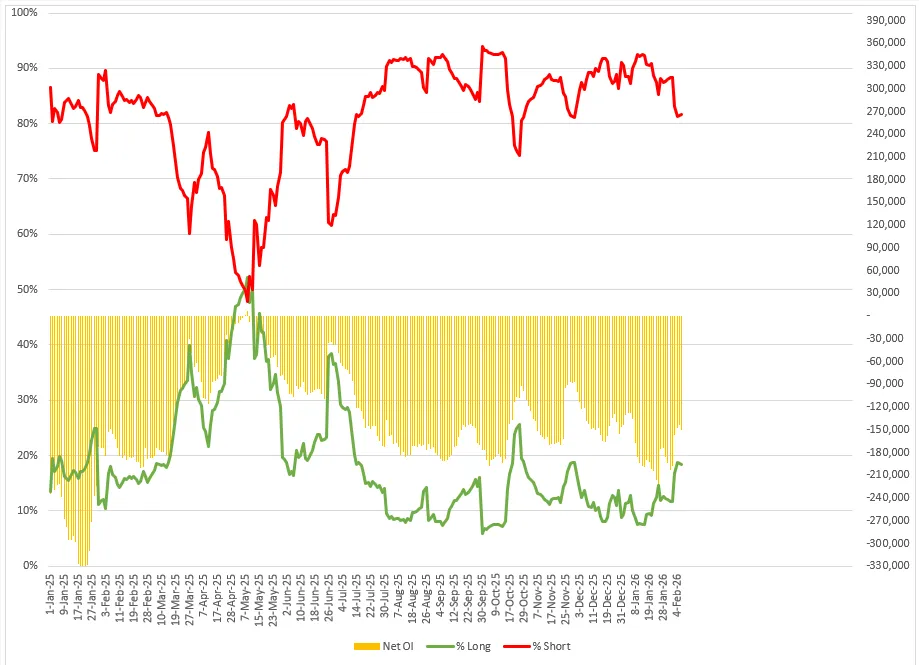

FIIs continued to reduce their short futures contracts, signalling a gradual decrease in bearish bets. | Image: Shutterstock

Indian markets extended the winning momentum for the second week in a row, with benchmark indices recovering from Budget day low after announcement of India-US trade deal. Benchmark indices witnessed above average volatility and dipped nearly 2% on the announcement of the Union Budget. However, the sentiment changed in favour of bulls as the United States slashed tariffs on India from 50% to 18%, waiving off secondary tariffs of 25% linked to Russian Oil.

For the week, the NIFTY50 index traded in a range of over 6% and settled at 25,693, up 1.4%. Meanwhile, SENSEX closed the week at 83,580, up 1.5%. The broader markets also recovered from weekly lows and ended the week on a positive note. The NIFTY Midcap 150 index rose 2% to 21,926, while Smallcap 250 index rose 15,864, up 0.6%.

Additionally, the RBI’s Monetary Policy Committee kept the interest rates unchanged at 2.52%, aligning with the expectation of the market. Sectorally, barring IT (-6.9%) and Defence (-0.1%), all the major sectors ended the week in green. Real-Estate(+7.7%), Energy (+7.0%) and Oil & Gas (+6.4%) advanced the most.

Meanwhile, in the United States earnings season continues, on Tuesday, Coca-Cola, CVS Health, and Ford Motor will announce their results, followed by Cisco Systems, McDonald’s on Wednesday.

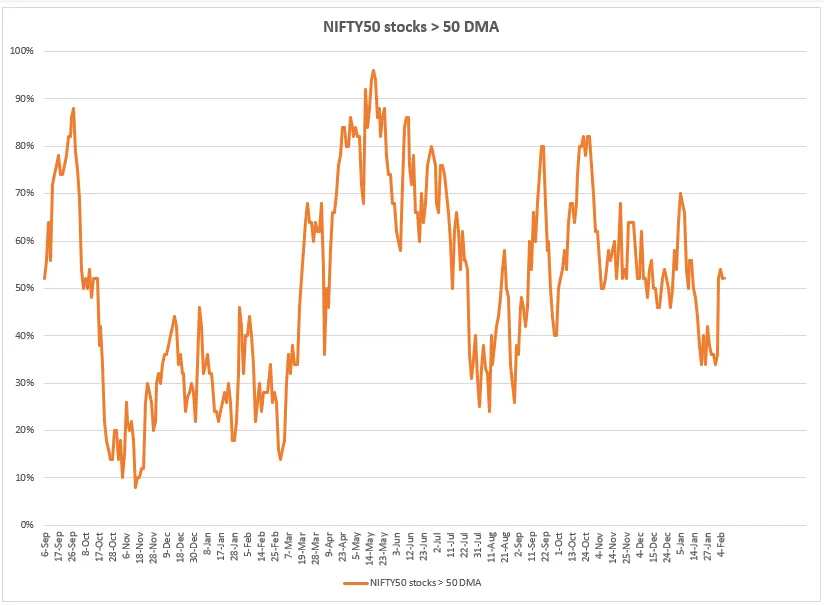

Market breadth

Market breadth has shown signs of recovery this week, with the percentage of NIFTY50 stocks trading above their 50-day moving average (DMA) rising from recent lows. Having slipped into the low 30s earlier, breadth moved back towards the 50% mark, signalling short-term relief following sustained selling pressure. Overall, the improvement in breadth suggests that selling pressure is easing.

FIIs cash market and derivatives

Foreign Institutional Investors (FIIs) continued to reduce their short futures contracts, signalling a gradual decrease in bearish bets. The long–short ratio improved significantly, with long positions rising from 12% to 18–19%, while short positions fell from 88% to around 81–82%. This suggests a steady phase of short covering rather than aggressive new selling. However, the FIIs' overall positioning remains bearish. Until the short contracts are fully covered, rallies are likely to be tactical, with FIIs preparing for renewed volatility rather than a trend reversal.

Meanwhile, in the cash market they have remained net buyers in February so far, purchasing shares worth ₹694 crore, marking a break from the relentless selling seen over the past seven months. On the other hand, Domestic Institutional Investors (DIIs) remain muted, with net purchase of ₹2,892 crore during the same period.

NIFTY50 outlook

The NIFTY50 index showed resilience, signaling a positive structure after a strong gap-up start following the announcement of the India-U.S. trade deal. The index is consolidating its gains around its 21-day and 50-day exponential moving averages (EMAs). Both the short-term and long-term technical structure of the index remains positive unless the slips below the 25,500 zone on a closing basis.

Disclaimer:

Derivatives trading must be done only by traders who fully understand the risks associated with them and strictly apply risk mechanisms like stop-losses. The information is only for consumption by the client, and such material should not be redistributed. We do not recommend any particular stock, securities, or trading strategies. The securities quoted are exemplary and not recommendatory. The stock names mentioned in this article are purely to show how to do analysis. Make your own decision before investing.

About The Author

Next Story