Market News

Week ahead: Crude oil volatility, Inflation data, Trump-Xi meet and FII activity among key market triggers to watch

.png)

5 min read | Updated on May 10, 2026, 11:36 IST

SUMMARY

In the week ahead, markets will track India’s April inflation data, US CPI, and crude oil prices amid US-Iran tensions. The Trump-Xi meeting, FII selling and key NIFTY50 levels near 24,570 on the upside and 23,780 on the downside will also remain in focus.

NIFTY Midcap 150 has gained 3.5% last week, breaking above its previous resistance zone near 22,500 on the weekly chart.

Indian markets ended higher for the week ended May 8, despite rising crude oil prices, Middle East tensions and continued selling by foreign institutional investors. The NIFTY50 gained 0.7% to close at 24,176, while the SENSEX advanced 0.5% to 77,328.

The market tone remained supported by strong domestic institutional buying, outperformance from broader markets, better-than-expected corporate earnings and a recovery in the rupee. However, the move was not completely smooth as global risk factors kept volatility elevated.

Broader markets continued to outperform. The NIFTY Smallcap 250 index gained 4%,, while the NIFTY Midcap 150 rose 3.5% and hit a fresh all-time high. This clearly shows that stock-specific action remained strong even as the benchmark indices moved in a narrower range.

The rupee was also in focus. It touched a fresh all-time low of 95.43 during the week but recovered sharply to close at 94.48 against the U.S. dollar.

A weekly close above this level signals renewed strength in the midcap space. Going ahead, 22,500–22,000 will act as the immediate support zone. As long as the index sustains above this breakout area, the broader trend may remain positive. Against this backdrop, constituents like Godrej Industries, Yes Bank, BHEL, Laurus Labs and Dabur India surged in the range of 27% to 12% last week.

The April print will be more important because crude oil prices have risen sharply due to the Middle East conflict. Experts believe India’s April CPI may rise to 3.8%, partly due to higher fuel costs.

In the US, the highlight will be the consumer price index, also due on Tuesday. The CPI rose 3.3% YoY in March, compared with 2.4% in February. Core CPI, which excludes food and energy, rose 2.6% YoY, compared with 2.5% in February. The April data will be watched closely for cues on the Fed’s rate path, especially as energy prices remain elevated.

Apart from data, geopolitics will remain in focus as US President Donald Trump is scheduled to meet Chinese President Xi Jinping in China. Markets will track any progress on trade talks and any discussion around the war with Iran.

Brent finally settled at $100 per barrel, down 8%, while WTI closed at $95, down 8% for the week. This shows that the market is still swinging between two narratives, fear of supply disruption in the Gulf and hopes of a possible agreement to de-escalate the conflict.

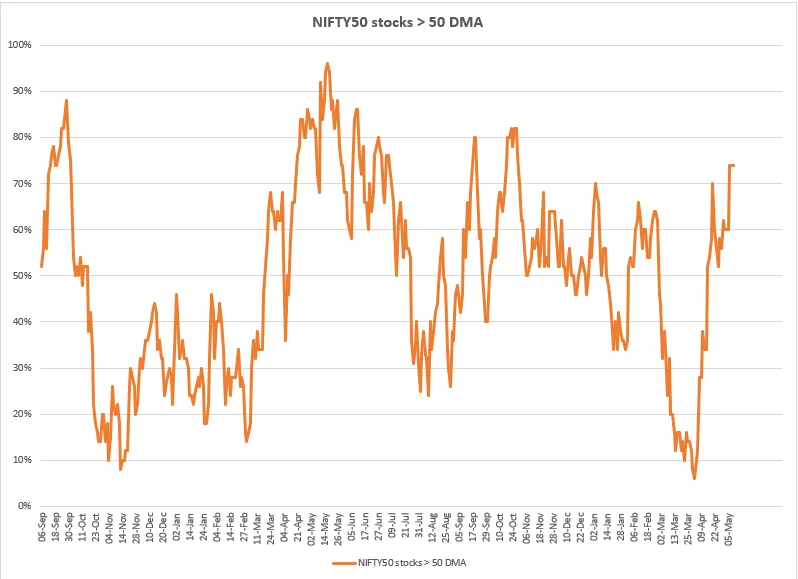

Market breadth

Market breadth improved sharply this week, showing that the recovery was not limited to a few heavyweight stocks. The percentage of NIFTY50 stocks trading above their 50-DMA rose to nearly 74%, its highest level in several weeks. This is a positive signal as it indicates broader participation across index constituents. However, after such a sharp rebound from March lows, the market may need some consolidation before the next leg higher.

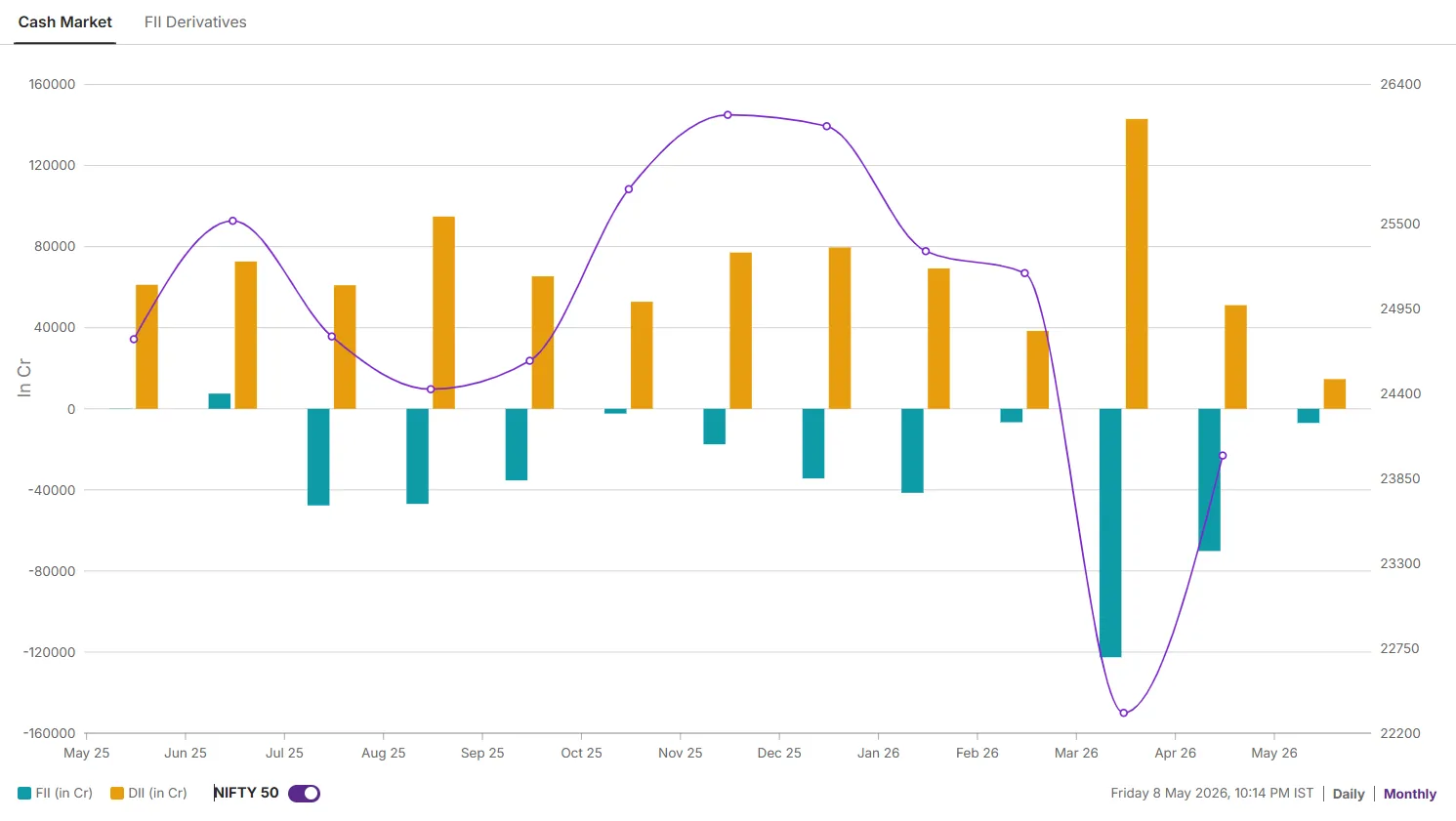

Foreign investors positioning

Foreign investors continued to maintain a cautious stance on Indian equities in May, offloading shares worth ₹11,072 crore so far in the cash market. For 2026, their net selling in the cash market stands at ₹2.5 lakh crore. This follows heavy outflows in the previous two years, with FIIs selling shares worth ₹3.06 lakh crore in 2025 and ₹3.02 lakh crore in 2024, respectively.

However, domestic investors continued to provide strong support to Indian equities. In 2026, DIIs have remained net buyers to the tune of ₹3.2 lakh crore so far. This follows strong buying in the previous two years, with domestic investors investing ₹7.8 lakh crore in 2025 and ₹5.26 lakh crore in 2024, respectively.

NIFTY50 outlook

On the daily chart, the NIFTY50 index is still trading above its 20-day (exponential moving average ) EMA, but remains close to the 50-day EMA, which suggests that the short-term structure is positive but not fully decisive.

For the coming week, 24,570 will act as the immediate resistance. A decisive close above this level can bring the weekly resistance zone of 24,990 to 25,140 back into focus. Until then, upside may remain capped and the index may continue to trade with a sideways-to-positive bias.

On the downside, 23,780 will be the first important support. A break below this level can weaken the short-term setup and push the index towards the next support near 23,490.

Disclaimer:

Derivatives trading must be done only by traders who fully understand the risks associated with them and strictly apply risk mechanisms like stop-losses. We do not recommend any particular stock, securities, or trading strategies. The securities quoted are exemplary and not recommendatory. The stock names mentioned in this article are purely to show how to do analysis.

About The Author

Next Story