Market News

Week ahead: Crude oil, US Fed meeting, Q4 earnings, and US-Iran talks likely to impact NIFTY50 and SENSEX

.png)

5 min read | Updated on April 26, 2026, 11:34 IST

SUMMARY

Markets head into the week on a cautious note after snapping their recent winning streak, with global and domestic triggers lined up. Crude oil prices remain a key overhang amid Middle East tensions, while the Fed’s policy decision and commentary will be closely tracked for cues on inflation and rate outlook. At the same time, a heavy earnings calendar led by the Mag Seven could drive global sentiment.

FIIs have remained net seller so far in April 2026, with total outflows of ₹56,363 crore.

Indian markets snapped their two-week winning streak and ended the week on a weaker note. Rising geopolitical tensions weighed on sentiment and the benchmark NIFTY50 index slipped 1.8% to 23,897 and SENSEX dropped 2.3% to 76,664. The fall in indices was driven by a spike in crude oil prices, weakness in the Rupee and continuous selling by Foreign investors in the equity market.

However, the pressure was not uniform across the market. While frontline indices saw profit booking, broader markets continued to outperform, indicating underlying risk appetite. The NIFTY Midcap 150 index and Smallcap 250 indices slipped 0.7% and 0.1% respectively.

Sectorally, IT stocks surrendered gains from the last five weeks and slipped over 10%. Automobiles and Consumer Durables stocks also came under selling pressure as the indices dropped 2.9% and 2.4% respectively. On the other hand, Energy and FMCG stocks did the heavy lifting for the week and jumped 2.5% and 2.3% respectively.

However, even though the sector is benefiting from earnings-led momentum, cost pressures are beginning to re-emerge, putting companies in a difficult position as they try to balance price hikes with demand recovery in a price-sensitive market.

Attention will then turn to the PCE price index, due to be released on Thursday (1 May). This is the Fed’s preferred measure of inflation, and it is expected to remain elevated, broadly in line with recent trends. This signals that price pressures continue to exceed the comfort zone.

On the domestic front, markets will track political developments as assembly elections progress across key states. The second phase of polling in West Bengal is scheduled for April 29, while exit poll trends are likely to start shaping sentiment as the voting cycle progresses. Other states including Tamil Nadu, Assam, Kerala, and Puducherry have already completed polling. Vote counting for all five states is scheduled on May 4.

Meanwhile, the following companies in India will announce their fourth quarter earnings of FY25-26: AU Bank, Coal India, Ultratech Cement, Varun Beverages, Eternal, Maruti Suzuki, Bajaj Finance, Federal Bank, Vedanta, Adani Ports, Hindustan Unilever, Bajaj Finserv and National Aluminium.

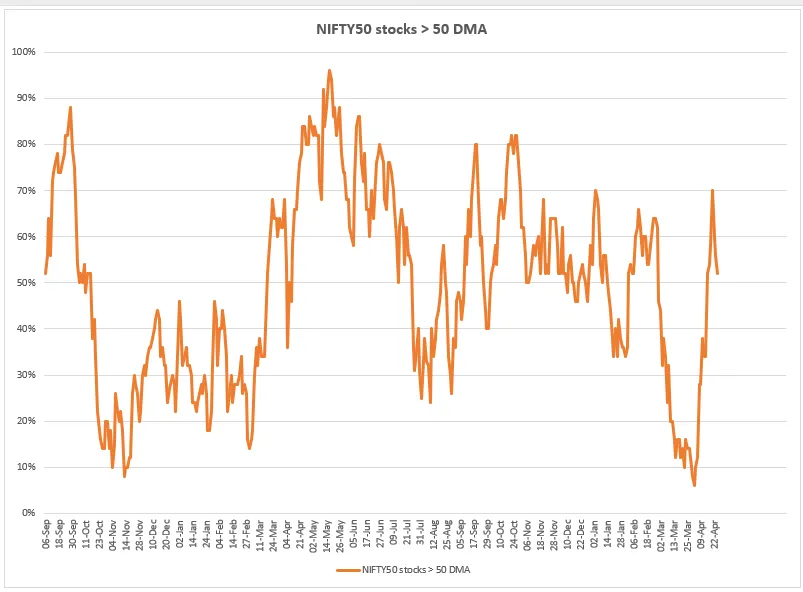

Market breadth

Market breadth has seen a sharp recovery in recent sessions. The percentage of NIFTY50 stocks trading above their 50 DMA bounced back from deeply oversold levels near 10–15% to around the 50–55% zone. This indicates that the recent pullback attracted buying interest and helped improve participation across the index. However, the current reading still sits in a neutral zone, suggesting that the recovery lacks strong conviction.

Foreign investors positioning

Foreign investors remained on the selling side through April, with total outflows of ₹56,363 crore. The selling intensity picked up sharply in recent sessions, coinciding with the decline in NIFTY. On the other hand, Domestic Institutional Investors (DIIs) continued to absorb the selling pressure, providing stability to the markets. They have bought shares worth ₹39,478 crore in April so far.

NIFTY50 outlook

NIFTY50 continues to trade in a volatile range, with price action failing to sustain above key resistance levels. The index recently attempted to move higher but faced rejection near the 24,600 zone due to a lack of strong follow-through buying.

On the downside, the 23,700–23,550 zone remains a crucial support band. This zone aligns with key moving averages and prior demand areas, making it important for bulls to defend. A decisive close below this range could open the door for a deeper correction, with selling pressure likely to intensify. On the upside, 24,300 remains the immediate resistance, and only a decisive close above this level would signal strength.

Disclaimer:

Derivatives trading must be done only by traders who fully understand the risks associated with them and strictly apply risk mechanisms like stop-losses. We do not recommend any particular stock, securities, or trading strategies. The securities quoted are exemplary and not recommendatory. The stock names mentioned in this article are purely to show how to do analysis.

About The Author

Next Story